(Bloomberg) via (TradersMagazine) MarketsMuse Fintech team notes that Deutsche Bank AG’s Stephen McGoldrick, who was leading a consortium of banks and asset managers in developing a new European dark pool for stocks, has decided to leave the project.

McGoldrick will return to his role as director of market structure at Deutsche Bank, according to a spokeswoman.Plato Partnership, the not-for-profit dark pool specializing in block trades, is being developed by eight banks and seven fund managers. The consortium has said it will redirect the profit it makes to academic research intended to improve Europe’s financial markets.

Stephen McGoldrick

“Stephen has done an exceptional job supporting Plato Partnership through the early stages of its development,” said Joanna Crawford, spokeswoman for Plato. “The Steering Committee would like to thank him for all his hard work.”

Turquoise, a market majority-owned by London Stock Exchange Group Plc, was selected in July to build the venue. The LSE subsidiary counts Deutsche Bank and Goldman Sachs Group Inc. among its minority shareholders, and they are also among the banks backing Plato.

Dan Mathews, a senior vice-president at Citigroup Inc., and James Hayward, who works in strategic investments at Goldman, were among Plato’s original architects, along with McGoldrick, the spokeswoman said. Mathews and Hayward will remain with the project.

The battle between business news pontificaters across the 4th estate is in full season, as evidenced by a smart article yesterday by Bloomberg LP’s Eric Balchunas and suggests that MarketsMuse curators are apparently not the only topic experts who noticed and took aim at a recent WSJ article that proclaimed savvy hedge fund types are increasingly exploiting exchange-traded funds by arbitraging price anomalies between the underlying constituents and the ETF cash product that occur in volatile moments.

That original WSJ article, “Traders Seek Ways to benefit from ETF woes …At the Expense of Investors” was misleading, and as noted by MarketsMuse Sept 30 op-ed reply to the WSJ piece, one long time ETF expert asserted that WSJ’s conclusions was “much ado about nothing.” Bloomberg’s Balchunas has since reached a similar conclusion; below are extracted observations from his Oct 12 column..

Hedge funds may need to get back to the drawing board if they’re planning to turn around their performance struggles by capitalizing on “shortcomings in the ETFs’ structure” via some unusual trade ideas, as highlighted in this recent Wall Street Journal article. Most funds do nothing of the sort.

Eric Balchunas Bloomberg LP

The vast majority of ETF usage by hedge funds is very boring. They love to short ETFs to get their hedge on and isolate some kind of risk. For example, they may short the Health Care Select Sector SPDR ETF (XLV) and then make a bet on one of the health-care stocks in the basket in order to quarantine a single security bet. Hedge funds have about $116 billion worth of ETF shares shorted, compared with only $34 billion in long positions, according to data compiled by Goldman Sachs last year.

The $34 billion in long positions is them using ETFs like everyone else — as a way to get quick and convenient exposure to a particular market. For example, the world’s largest hedge fund, Bridgewater Associates, has a $4 billion position in the Vanguard FTSE Emerging Markets ETF (VWO), which it has held for six years now. There’s also Paulson & Co.’s famous $1 billion position in SPDR Gold Trust (GLD), which it has been holding for almost seven years. Like anyone else, they like the cheap exposure and liquidity VWO and GLD serve up.

With that context in place, yes, there are a tiny minority of hedge funds that engage in some complex trades like the ones highlighted in the article. But each trade comes with at least one big problem.

Before anyone tries any of these at home, it’s important to deconstruct them.

Trade #1: Robbing Grandma

How it works: During a major selloff, try and scoop up shares at discounted prices put in by small investors using market orders.

The problem: It’s super rare. Aug. 24, which saw hundreds of ETFs trade at sharp discounts amid a major selloff, was basically an anomaly. At best, a day like that happens once every two years. Thus, to capitalize on discounts of the 20-30 percent variety is like standing on a beach waiting for a hurricane to hit. And you won’t be the only one, so you may wait two years only to find you can’t get your order filled on the day the big one hits. In addition, no large institutional investors are putting in market orders. So this low-hanging fruit is sell orders for tiny amounts put in by unknowing small investors. Essentially this is the white-collar equivalent of robbing Grandma for some loose change in her purse.

Moreover, Aug. 24 may never happen again, at least the way it unfolded. ETF issuers are working with the exchanges, the regulators, and the market makers — and even making significant recommendations — to make sure those kinds of small investors aren’t exposed again like that.

It should be noted, though, that arbitrage between the ETF price and the value of the holdings happens day in and day out with ETFs — that’s how ETFs work. They rely on a network of market makers and authorized participants to arbitrage away the discrepancy between the ETF’s underlyings and its net asset value (NAV).

Trade #2: The Double Short

To continue reading the straight scoop from Bloomberg columnist Eric Balchunas, click here

For followers of the global equity crowdfund movement and fintech aficionados who are fluent in ‘what’s next?’, this is a big news week from the crowdfund world. Yesterday, MarketsMuse curators spotlighted a just-launched trading exchange that brings billions of dollars worth of private shares into the wacky world of secondary market trading. While there are rumored to be various efforts to package equity-crowdfunded ‘equity stakes’ into exchange-traded fund structures, which is arguably the “next great idea, “the first ETF for Equity Crowdfunding” has yet to be formally announced.

Before that announcement actually happens, today’s announcement from the multi-billion crowdfunding space (see link below) might be the data foundation such an initiative. and could very well be the vision spearheaded by this new portal, RaiseMoney.com.

MarketsMuse editor note: fully-disclosed, one of our favorite staff members was cited in this news story with the following comment

“Noted Pete Hoegler, senior analyst for financial industry blog, MarketsMuse.com, “The RaiseMoney.com platform has three critical elements in its favor. Firstly, they have a really compelling domain name that inspires immediate brand recognition.” Added Hoegler, “Secondly, this group has the benefit of not having “first-mover disadvantage” and most important, RaiseMoney.com is providing a much-needed service for a still nascent industry that is capturing the attention of millions of people and billions of dollars.”

Click below for the formal announcement distributed by NASDAQ’s GlobeNewswire

MarketsMuse FinTech curators feigned no surprise when noticing today’s announcement from the City of London profiling a new initiative just launched today that will accommodate equity crowdfund investors–a real, live exchange to trade out of equity crowdfund investments.

To paraphrase the opening observation from global crowdfund directory and search platform RaiseMoney.com…

“…From the “What Will Those Finance Wonks Think of Next?! Dept,” City of London investors (and the thousands of bank trading desk folks plying their trades down near Canary Wharf) are now getting an exchange to trade crowdfunded investments, as the UK’s first crowdfunding marketplace launches today….

Not to be confused with the London Stock Exchange, or the ubiquitous NYSE, Crowdfunding platform Crowd2Fund is opening “The Exchange”, where investors will be able to sell off investments made in equity crowdfund deals and access their capital.

Crowd2Fund, which launched in late 2014, is an FCA-regulated platform specialising in revenue loans. But trading on the new marketplace won’t be limited to investments made on this platform – it’ll be opened up to exchanges of investments made on any crowdfunding campaign.

Peer-to-peer lending and crowdfunding is a booming part of London’s soaring FinTech sector. Crowdfunding campaigns grew a staggering 420 per cent in 2014, leaving the sector with growth of £1.74bn.

MarketsMuse extends a warm salute to the nation’s oldest and largest minority brokerdealer owned and operated by service-disabled military veterans in connection with the following news announcement..

Oct 5 2015–Stamford, CT and Newport Beach CA–Mischler Financial Group, Inc., the financial industry’s oldest and largest institutional brokerage and investment bank owned and operated by Service-Disabled Veterans is pleased to have served as a Silver Sponsor for the 2015 Army Ranger Lead The Way Fund Gala. Silver Sponsors contributed a minimum of $25,000; proceeds to

Mischler Rates Trader Glen Capelo (l), Duke University Coach K Krzyzewski (c) Mischler CEO Dean Chamberlain (r)

are dedicated to support service-disabled US Army Rangers and the families of Rangers who have died, have been injured or currently serving in harm’s way around the world.

This year’s annual gala took place September 30 at New York’s Chelsea Piers and NBC News Anchor Tom Brokaw served as Master of Ceremonies. The 2015 Lead The Way event paid tribute to 5-time NCAA champion and college basketball legend Mike “Coach K” Krzyzewski, a US Military Academy at West Point Graduate (USMA ’69) and a former classmate of Mischler’s Founder and Chairman Walt Mischler. Coach K served two tours of duty prior to his career as a world famous university basketball coach.

Mischler Financial’s VP of Capital Markets Robert MacLean (USMA ’02), who served seven years as a US Army Ranger and is a two-time recipient of the Bronze Star, served as a member of this year’s Lead The Way Fund Host Committee. MacLean shared that honor with a short list of military veterans who have since forged a path on Wall Street at firms that include among others, Goldman Sachs, JPMorgan, UBS, Credit Suisse, Barclays, and Fortress Investment Group.

“To put it bluntly, what headline writers or traders are selling you today is a load of bollocks.” Neil Azous, Rareview Macro LLC

When global macro guru Neil Azous of Rareview Macro appeared on CNBC midday yesterday, MarketsMuse curators had already absorbed and relayed his recent views about energy prices, as well as his relatively rare (and sober) view as to the mid-term outlook for equities. When he opined late last night, “You date equities, but you marry credit..” via his Twitter feed, MarketsMuse Fixed Income curators smirked; simply because our resident bond market experts have long held that rare view–one that today’s “young Turks” often fail to appreciate.

Whether Monday’s equities market action was merely a ‘dead cat bounce’ in a progressively deteriorating state of market metrics that some attribute to a cyclical ‘earnings recession’, or a firming up of the underlying financial market foundation that portends “higher for longer” stock prices, its good to have sight beyond sight…

Consensus is a Classic Counter-Trend Tuesday…You Date Equities but Marry Credit

To put it bluntly, what headline writers or traders are selling you today is a load of bollocks.

Emerging market equities have just recorded their largest five-day gain since the taper tantrum in June of 2013. While the historical precedent is not the same the absolute performance is of similar magnitude for developed market equities. The prevailing view is that this is on account of a weaker US dollar, and on the view that lower interest rate for longer will be supportive for global growth.

As a gesture of goodwill by the Bulls, after five days of impressive stock gains, and for no other real reason, the consensus view is that today is a classic counter-trend Tuesday.

We have to chuckle to ourselves over this, because just last week, a stronger US dollar and an imminent interest rate increase that would remove the Federal Reserve uncertainty were also viewed as positive for equities. There is not even an acknowledgement that the move off the lows in the S&P 500 is very similar to the market bounce seen at end of August, and we all know how that worked out.

We’ll leave the narrative spinning to everybody else and, as we do every day, just try and deliver you some sight beyond sight.

One would think that this large group of people, all of whom consider themselves students of the market, would include a few other basic factors in their headline writing or analysis, such as:

The BoJ meeting tonight;

The ECB and BOE meeting minutes on Thursday;

Dead-cat equity market bounces of this magnitude are thematic during bear markets;

Reluctant buyers ahead of earnings season, especially considering a mini-theme of negative pre-announcements beforehand has already begun.

We suppose the list of data points could go on and on, but for us the key driver for risk assets is whether financial conditions tighten or loosen. We are watching corporate-based measures closely for that insight, not just the traditional market-based measures the majority on the Street monitor.

Despite the bounce in equity markets, a minor step-change in sentiment around the energy sector, which is supportive for inflation expectations, and the minor relief that a weaker US dollar and lower interest rate profile provides, there really has been no loosening in financial conditions over the past five days.

The breakdown in correlation between equity and credit markets is too hard to ignore, especially if you are looking for the upturn in equities to show durability beyond the past five days.

Here are three examples from yesterday of what we mean by this disconnect between stocks and credit and how credit is struggling with the tight financial conditions. These are just some of the corporate-based, as opposed to market-based, measures we are referring to.

Ford Credit (F), a BBB rated issuer, came to market with a two-part 3-year fixed and floating rate note deal. Later in the day, the 3-year fixed notes were sold after combining its fixed and floating rate tranches. Additionally, it was forced to pay a 35 to 50 bps concession over its nearby 3-year fixed issue to print new paper. The key takeaway is that with a BBB rating, in this type of market, Ford would only issue if it “needed” to, not because it would do so opportunistically. Accordingly, the market is making them pay up for this new paper.

The Province of Ontario (a sovereign-type issuer that is rated A+) stood down from issuing a €2.5bn 10-year deal due to “market conditions”, even though the deal had already been pre-marketed (i.e. investors knew of and were prepared to buy the deal).

The lead managers released the statement below. This is extraordinary to say the least and illustrates how even the best credits are being very cautious… “Ontario always tries to right size its transactions and provide a liquid benchmark sized offering. The Province views the USD and EUR markets as core strategic markets and, as such, wants to maintain a well-defined liquid yield curve in each currency. Market conditions were today such that Ontario could not meet these objectives and, as a result, has decided to step back from the market at this stage and would like to thank investors for their interest.”

Five (5) other IG deals were known to have stood down from coming to market yesterday, following the decision by the Province of Ontario. (Source: Mischler Financial, Quigley’s Corner, Ron Quigley)

In our view, we do not expect financial conditions to confirm the recent equity bounce. In fact, we think tighter financial conditions will be a key determinant in why the fourth quarter positive seasonal call will struggle this year despite the stock trader’s almanac always saying otherwise.

Firstly, we have already made our views very clear on how one major financial condition – the corporate financing gap – has now swung into deficit. And we have pointed out the consequences of that: it will limit their ability for further credit issuance, M&A will cost more, and stock buybacks will slow, and that collectively has led to the Street being way too generous in its fourth quarter forecasts for all of these metrics.

In fact, we were pleased to see Deutsche Bank yesterday echo what we have already said and lower its forecast for stock buybacks in 2016 by 25% or more, relative to the total announced in Q3 ($600bn annualized). Moreover, the buyback announcements in Q3 were already significantly lower than the first half of the year.

Secondly, investors are beginning to recognize that a high yield bond should never have traded with a 4% yield in the first place, as that yield was artificially inflated by extreme monetary policy measures such as QE. So while spreads have widened a lot, a 5% or 6% yield should really still be the equivalent of 7% or 8% similar to other cycles. Additionally, the breadth of weakness, for the first time this year, has now spread outside of the energy and materials sectors as investors do their homework on the rest of the things they own. The point here is that high yield is not cheap if the measurement is multiple cycles, not just the cycle with extraordinary monetary measures.

Finally, the other anecdotal trend we are observing is that credit traders don’t have the same appetite as equity traders to buy weakness right now. The majority of credit trader’s performance over the last few years is easily traceable to buying a new issue, watching that credit tighten immediately thereafter due to the sensational appetite for yield, and then selling them out quickly. Put another way, you are insulting equity investors when you call them IPO flippers. Right now, this trade does not exist and anyone who does not have a genuine investment process is being shut out of the market. This is one reason why credit spreads are not tightening.

The bottom line is that corporate Treasurers or credit investors remain highly suspicious of the primary issue market. Yes, companies will always need to re-finance their credit stack as part of their normal operations, as could be seen with Ford Motor paying up for it yesterday. But anything opportunistic is on hold, especially if a company has to re-model their economic projections for an M&A deal in the pipeline, as that will now come at a higher price.

So until we see several – by which we mean 3 to 4 consecutive days – of firm market tone conveying that corporate Treasurers and credit investors are once again aligned it is pretty easy to chalk up the latest move in stocks to nothing more than a classic bear market bounce. If this does not materialize, then the mindset of selling into strength will prevail.

As a reminder, when push comes to shove, you date equities but marry credit, especially after a 5-6% bounce.

Neil Azous is Founder/Managing Member of global macro think tank Rareview Macro LLC and the publisher of global macro newsletter, Sight Beyond Sight, a daily publication subscribed to by leading hedge funds and investment managers. Neil’s real-time comments and trade ideas are often posted to Twitter

To continue reading the Oct 7 edition of Sight Beyond Sight, please click the following link. Subscription is required, a Free Trial is available (no credit card required). Click here to access...

Professional Investment Community Cries Out in Agony and They Don’t Yet Know Exactly Why

MarketsMuse Strike Price and Global Macro curators voted the Oct 5 edition of global macro advisory firm Rareview Macro’s Sight Beyond Sight the best read of the week. Yes, its only Monday, but those who follow this newsletter as we do (along with a discrete universe of savvy investment managers and hedge fund traders) have discovered that a certain degree of prescience can be contagious when trade ideas are presented with a pragmatic, transparent and easy to understand thesis.. Below are the lead-in topics and followed by selected excerpts…

A Great Disturbance in the Force – Oil, Materials, & Momentum Strategies

Portfolio Overlay – Two Inexpensive Ways to Add Downside Convexity

New Trade – Short 2-Year US Treasuries via Put Options

For those of you who still have to make up your mind on whether we can help you or not with your daily investment process, today’s edition of Sight Beyond Sight is a good example of what makes us different. The majority of the morning notes you have received today all center on the “bad news is now good news” meme or how lower interest rates for longer will be supportive for risk assets. Of course, none of them have highlighted that financial conditions have been tightening all year long so despite the call for lower interest rates for longer the real world is not buying that unless credit spreads tighten. Instead, we will give you a rareview into how risk takers are faring across various strategies. Additionally, we provide three new trade ideas.

Neil Azous, Rareview Macro

In the 1977 iconic movie Star Wars: Episode IV-A New Hope, following the scene where the Death Star destroys the planet Alderaan, the Jedi Knight, Obi-Wan Kenobi, said: “I felt a great disturbance in the Force, as if millions of voices suddenly cried out in terror and were suddenly silenced. I fear something terrible has happened.”

I have started with that quote because it seems the best way to describe the Start of the new week for the professional investment community. Take a look at the below observations and it will be easier to understand why risk takers are “crying out in terror” and for many of them “something terrible has happened”.

If you are a global macro fund, then liquidity is not going to be your friend today as you defend core strategies that are deeply entrenched. For those who have been living on a deserted island the remaining long US dollar positioning is mostly versus emerging market FX and G10 commodity currencies, rather than other reserve currencies such as the euro, Japanese yen, Pound sterling, and the Swiss franc.

If you are a long/short strategy, you already know what is happening because it started well over a week ago.

You just did not want to believe it. Not to worry, a further unwinding in the long Financial/healthcare versus short Material/Energy sector strategy will help you finally come to grips with reality. If you are a quantitative fund, up until really last Friday in both Europe and the US, you have had the benefit of being part of the number one factor input and best performing strategy this year –that is, MOMENTUM. Sadly for you, the reversal of that strategy is a lot more violent on the way out then chasing it on the way in. Perhaps you will take back your 15 minutes of old fame from the new guys-Risk Parity and Target Volatility funds?

The conclusion would be that the worst-of-the-worst–energy, materials and bottom 15% of single stock performers–is now in play from the long side for whatever reason –its “go time”, crude oil has bottomed, or gross exposure reduction is not near being completed.

The current price in S&P 500 futures is ~1950. The low on August 24th was 1831. The difference between the two is ~6%.Protecting against a 6% downside move, or 120 S&P 500 points, is an expensive exercise right now, and not one we are interested in. Instead, we are more worried about the second 6%, or the move down to 1720-1700 from 1831, especially the air pocket that is likely to develop once/if the August 24th intra-day low of 1831 is breached.

The problem is that we do not know the short-term direction of the S&P 500 index, including if it will first go to 2000 in the next 30-days but we are highly sensitive to an even larger move on the downside in the fourth quarter than what occurred in the third quarter. So working on these premises, what are the best strategies to deploy right now? We think having a two-tiered approach between the S&P 500 index and equity volatility, as measured by the CBOE VIX Index, is an optimal strategy.

We’ll look to dynamically manage both of these strategies side-by-side in the event that we see another leg lower in US equities. The two strategies we like are and the ones we deployed in the model portfolio late last week and posted via Twitter are…. Continue reading →

MarketsMuse Fixed Income Update “Corporate Bond Market- Balancing on a Knife Edge” is courtesy of extract from the 10.02.15 weekend edition of “Quigley’s Corner”, a daily synopsis of the investment grade corporate bond market and rates trading space authored by Ron Quigley, Managing Director of investment bank and institutional brokerage Mischler Financial Group, the financial industry’s oldest and largest minority brokerdealer owned and operated by service-disabled military veterans. Mischler Financial was selected in 2014 and again in 2015 for the Wall Street Letter Award “Best Research-Brokerdealer”

Ron Quigley, Mgn.Dir. Mischler Financial Group

Blackouts couldn’t be more optimally timed as we experience massive re-pricing in our IG primary credit market. The corporate black-outs are serving as an unplanned, well-timed inherently built-in “kick-the-can” that is necessary in helping us to all buy time as we navigate thru what is perhaps the most unpredictable, treacherous, volatile and uncertain time that our primary markets have experienced since 2008. As one very senior syndicate source told me “the credit markets are sitting on a knife’s edge.” IG spreads are on the whole 44 bps wider at the end of the third quarter according to Morgan Stanley.

Today’s notoriously and unexpected poor employment data was the last thing credit markets needed and it has instigated a massive Treasury rally. Perhaps this is a bit of good news because when both are combined, is a potential high velocity tailwind to credit products from big government bond funds. However, that’s “if” funds want to own credit product and hold it for an extended period of time and potentially wear a negative mark-to-market.

Having said that, the guy-in-the-corner suggests that at some point this weekend, you should put on your favorite song and sing along to it after many shots of tequila. When you get to the point of feeling bad, look at yourself in a mirror and realize that you can begin to feel better with coffee, food, sleep and time but come Monday morning the business model you are used to is about to change. Not adapt; not get better; rather change. The trends in the credit markets that we have seen over the last two quarters are showing no signs of abating, and in some degrees, worsening.

Now please let me introduce the moment you’ve been waiting for..

Syndicate Forecasts and Sound Bites from “The Best and the Brightest!”

I am happy to report that once again the “QC” received unanimous participation from all 23 syndicate desks surveyed in today’s Best & Brightest polling. That includes all of the top 22 ranked syndicate desks according to Bloomberg’s U.S. IG U.S. Investment Grade Corporate Bond underwriting league table that can be found on your terminals at “LEAG” + [GO] after which you select #201 (US Investment Grade Corporates). Their cumulative underwriting percentage is 94.00% of YTD IG dollar debt underwriting which simply means they’re the ones with visibility. But it’s not only about their volume forecasts, rather it’s also about their comments! This core syndicate group does it best; they know best; so they’re the ones you WANT and NEED to hear from.

*Please note that these are Investment Grade Corporates only. They do not include SSA issuance unless otherwise noted.

The question posed to the “Best and the Brightest” early this morning was:

“Good morning! So, this week the massive repricing in primary markets saw average NICs bust out to 54.23 bps; bid-to-covers shrank to an average 2.02x; today’s numbers were BAD; Obamanomics is quite the engine of growth and job creation, China’s slowdown is showing up in our data (ISM Milwaukee posted its worst manufacturing number since the dot com bubble). Spreads are wider on today’s data to start. Lower-for-longer might just be lower forever! The two-part question for today is what are your volume forecasts for IG Corporate supply for BOTH next week AND October? It’s going to be challenging to nail that down but it’s an important survey at this critical juncture. Many thanks, Ron”

MarketsMuse ETF Curators debated on the title to this story, and first suggested the headline “Has BATS Gone Bats?!” While market structure experts continue to debate the topic of pay-to-play, i.e. payment for order flow schemes, BATS Global Markets, the youngest and arguably, now one of the largest electronic exchanges in the global marketplace based on trade volume across equities, ETFs and options is proving again Donald Trump’s moto: “Controversy Sells!”

According to the firm’s announcement last night, BATS is upending the traditional fee model for companies to list on an exchange-one that had Issuers paying the Exchange for the privilege of listing the company’s securities in consideration for the respective exchange’s brand integrity and financial ecosystem integrity. Instead, BATS, in effort to capture a lead role in the Exchange-Traded Fund space is now offering to reverse the business model and will pay ETF Issuers to list their products on the BATS exchange platform.

The way in which ETF products trade has recently come under close scrutiny by market regulators and institutional investors in the wake of both disconnected NAV prices of the cash product v. the underlying constituents during volatile periods and in connection with leveraged ETF products performing in unanticipated ways v. the way in which respective marketing materials proclaim those products can be expected to perform.

As noted in today’s WSJ story by Bradley Hope and Leslie Josephs..

The Lenexa, Kan.-based exchange operator on Thursday plans to launch what it calls the BATS ETF Marketplace, which will pay ETF providers as much as $400,000 a year to list on BATS. Payments will vary depending on average daily volume.

Traditionally, ETF providers have paid between $5,000 and $55,000 a year to list on a stock exchange. BATS previously offered firms the option to list on its exchange for free. Besides the monetary incentive, the marketplace is also changing the way it rewards market makers for continuously offering to buy or sell ETFs, a move it said will help reduce volatility.

“We are redefining the relationship between ETF sponsors, investors and market makers,” CEO Chris Concannon said in an interview.

ETFs have come under greater scrutiny after they faced trading issues on Aug. 24, including prices of ETFs being far out of whack compared with the prices of the underlying holdings. Exchanges, market makers and ETF sponsor firms are in discussions about how to make wider changes to rules to help prevent similar problems from happening.

“August 24 obviously makes us go back and say: ‘Are our decisions the right ones?’ ” said William Belden, managing director of ETF strategies at Guggenheim Investments LLC.

While equities markets have zig-zagged since late summer with lots of volatility, leading to pretty much no change in major indices since late August, news media outlets have put their cross hairs on the ETF industry, which has been battered with criticism consequent to out-0f-context pricing that has riddled opening bell markets during recent spikes in volatility. CNBC pundits have invited an assortment of geniuses to explain, defend or attack ETFs for days, including 30 minutes dedicated to the topic mid-day yesterday. The industry print publications have been repurposing each other’s copy with similar themes for days, and the SEC and other alphabet agencies are purportedly ‘investigating’ the ETF industry as a consequence of the recent disruptions.

For equities market experts who are fluent in exchange-traded funds, which are nothing more placeholders for bespoke basket trading strategies–you know that the notion of disruptions in pricing of the cash product aka the ETF could easily happen whenever there is a dislocation in the underlying constituents. Its a caveat emptor type of product. But, somehow, this simple concept has been lost on everyone, except of course by ‘savvy hedge fund managers’..and what a surprise, one HF name now being mentioned for exploiting ETF products is none other than Steve Cohen.

Here’s an excerpt from today’s WSJ “Traders Seek Ways to Benefit From ETFs’ Woes…In some cases, gains come at expense of individual investors”….–which is arguably best suited for college freshman taking elementary classes. According to one trader interviewed by the MarketsMuse Curator, “If there is any SEC-certified RIA or any institutional investor who doesn’t understand this product and the related nuances [and believes the WSJ article was informative], your license should be stripped.”

Here’s an excerpt from today’s WSJ story by Rob Copeland and Bradley Hope Continue reading →

Many fixed income folks are lamenting about liquidity in the corporate bond market. LiquidNet, the institutional trading platform is determined to make corporate bond trading more liquid..for the buyside.

Just when you thought e-bond trading for corporate bonds was a never ending pipe dream…

Liquidnet Launches Fixed Income Dark Pool to Centralize Institutional Trading of Corporate Bonds

More than 120 asset managers across the US and Europe on-board for launch

Enrolled asset managers comprise two-thirds of top 50 holders of US corporate bond assets under management

September 29, 2015 08:00 AM Eastern Daylight Time

NEW YORK–(BUSINESS WIRE)–Liquidnet, the global institutional trading network, today announced the launch of their Fixed Income dark pool that facilitates direct, peer-to-peer trading of corporate bonds among asset managers in the US, Canada and Europe, creating a much-needed hub of institutional liquidity. Liquidnet has enrolled more than 120 asset managers, representing a critical mass of liquidity and a sizeable portion of assets under management for high yield and investment grade bonds in the US. At launch, the platform will enable trading for US and European corporate bonds (high yield and investment grade), emerging market corporate bonds, and European convertible bonds.

“Greenwich Associates research found that 80% of investors find it extremely difficult to execute large block trades; as such, a platform that can help ease that burden while not causing a shift in the trader’s workflow is a necessary part of the path forward.”

The Fixed Income dark pool has been designed to provide a seamless solution for corporate bond traders, providing them a protected venue in which to trade natural liquidity safely and efficiently. The platform has been built with input from Liquidnet’s network of leading asset managers and bolstered by the firm’s experience operating the leading dark pool for the institutional trading of equities. Similar to Liquidnet’s equities solution, the Fixed Income dark pool will provide the option for those corporate bond traders utilizing an order management system (OMS) to easily have their orders swept into the pool with minimal changes to existing workflow.

“The fixed income market has been woefully underserved by technology and, as concerns about a liquidity crunch continue to rise, it needs a transformation,” said Seth Merrin, founder and CEO of Liquidnet. “With close to 15 years of experience connecting asset managers around the world to solve the unique challenges of institutional equities trading, Liquidnet is uniquely positioned to provide a more efficient trading solution and experience that delivers a critical mass of natural liquidity that minimizes information leakage and maximizes best execution.”

Liquidnet has leveraged its relationships with partners and existing buy-side Member firms to ensure the platform’s success at launch. In June, the firm announced successful integrations with seven OMS operators that support direct connectivity, and a partnership with Interactive Data for continuous evaluated pricing to aid in pre-trade transparency and more efficient best execution analysis. In addition to new features, Liquidnet has also expanded its Fixed Income team and expertise with the recent high-profile appointment of Chris Dennis, formerly of BlackRock, as head of US Fixed Income Sales.

“The corporate bond market is desperate for innovation and improved efficiencies, and we’re starting to see several new trading platforms emerge,” said Kevin McPartland, Head of Research for Market Structure and Technology at Greenwich Associates. “Greenwich Associates research found that 80% of investors find it extremely difficult to execute large block trades; as such, a platform that can help ease that burden while not causing a shift in the trader’s workflow is a necessary part of the path forward.”

“Liquidnet Fixed Income was designed with significant input from the buy side to create the first true dark pool for corporate bonds,” said Constantinos Antoniades, Liquidnet’s Head of Fixed Income. “By facilitating a high-quality critical mass of participants, including two-thirds of the top 50 holders of US corporate bonds, Liquidnet will provide the most convenient, secure trading venue for institutional fixed income trading going forward.”

A recent survey of buy-side firms—comprising $12.15 trillion in assets under management—conducted by fixed income magazine, The Desk, stated that 58 percent of buy-side respondents indicated that they were planning to move to Liquidnet for their fixed income trading.1

The FinTech aka financial technology revolution continues to advance across the financial industry landscape, as dozens of startups from block chain to bond trading initiatives work towards securing a presence within the institutional financial services ecosystem. And, as profiled in a brilliant column this week from Institutional Investor spotlighted by MarketsMuse tech talk curators, the City of London is quickly carving out a leading role for being Europe’s epicenter for incubating the next greatest applications. The question now is, “How soon will London’s Silicon Roundabout squeeze out Silicon Alley and Silicon Valley?”

The excerpt from II’s Charles Wallace latest report, “FinTech Startups Flock to London’s Silicon Roundabout” is below. A link to the entire article follows accordingly.

Raja-Palaniappan

Raja Palaniappan worked at Credit Suisse in London as a bond trader for a number of years before deciding to go out on his own and launch an online marketplace called Origin Markets, which seeks to revolutionize private placement bond issuance by eliminating intermediaries like Goldman Sachs Group. Although American by nationality, Palaniappan decided to open his platform in London because he felt the city offered greater opportunity than New York or Silicon Valley for a new financial technology, or fintech, company (see “ Former Trader Raja Palaniappan Sees Fintech Opportunity in Bonds”).

“London does have a competitive advantage in fintech because you’ve got technology in Old Street and finance on Liverpool Street and they’re about three quarters of a mile apart,” Palaniappan says, referring to two areas of the City of London financial district. “In the U.S. technology lives on the Left Coast and finance on the Right Coast, and there’s little consolidation between the two.”

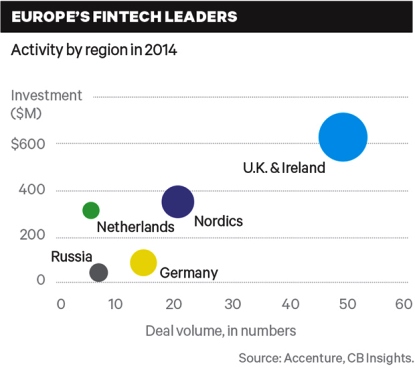

According to consulting firm Accenture, Europe is the world’s fastest-growing area for fintech funding, with spending rising 215 percent last year, to $1.48 billion. London had the largest share of that investment, some £342 million ($530 million), according to London & Partners, a government-funded agency supporting the London economy. Although the U.S. continues to lead overall fintech funding, with $2 billion in 2014, much of that was Silicon Valley–based investment in business-to-consumer start-ups like LendingTree, an online exchange that connects consumers with lenders; in London much of the activity is targeted at institutional financial services such as banking, insurance, trading and asset management.

“Since the Industrial Revolution, London has been the center for international commerce, and the melting pot that you have in terms of people and talent is pretty unique in the world,” says Sean Park, a Canadian who runs Anthemis Group, a firm that advises and invests in fintech start-ups from offices near Oxford Circus in Soho.

London’s growth as a fintech hub is not exactly surprising. The city is the world’s leading center for international wholesale financial services. It boasts more banks than Hong Kong or New York, leads the world in foreign exchange trading, has vibrant asset management and insurance sectors, and is home to the Eurobond market. In addition, fintech enjoys strong support from the British government, which sees the financial services sector as essential to the health of U.K. Plc and technology as critical to maintaining London’s competitive edge. Financial services employ some 2 million people, or about 7 percent of the country’s workforce, and generate 10 percent of the U.K.’s gross domestic product. Continue reading →

MarketsMuse news curators have spotted dozens of commentaries from leading equities and debt market pundits opining about global mining giant Glencore. There is only one comment that offered a truly rare view that struck a chord, and it is courtesy of this morning’s edition of global macro newsletter “Sight Beyond Sight”, which is published by global macro think tank Rareview Macro LLC. The title of today’s edition:

Tentacles from Glencore Extend Well Beyond the Naked Eye…Quarter-End Flight to Quality

Neil Azous, Rareview Macro

Today’s edition of Sight Beyond Sight is going to sound aggressively Bearish to some people. At the same time, the tone is insensitive to the countries, companies, and employees involved. If that bothers you, that is too bad. This is a financial services newsletter, not the United Nations or the Red Cross. We are not trying to disparage anyone or call someone out. Our goal is to try and help you make or save money.

When I traded credit derivatives at Goldman Sachs back in the late 1990’s, the way we separated our bond business between investment grade, high yield and distressed was very simple. If an issuer’s bond price was trading above 80 cents on the dollar you were investment grade. Conversely, if an issuer’s bond price was trading below 80 cents on the dollar you were high yield. Anything below 50 cents on the dollar, you were distressed. Below 20 cents…don’t ask.

Glencore EU1.25b notes due March 2021, one of the most recently issued and liquid tranches of their debt outstanding, dropped six cents to~76 cents on the euro today, effectively crossing over into high yield territory even though it still maintains its BBB credit rating. Headline writers argue that most of the weakness today in Glencore’s stock and bond price is the result of comments made by Investec Plc, where it warned that there would be little value for shareholders should low commodity prices persist. This echoes a key research note last week from Goldman Sachs that said: “If commodity prices were to fall 5% from current levels–which we do not consider to be a far-fetched assumption given the downside risk to commodity consumption in China–we believe that concerns about its IG credit rating would quickly resurface.

Under this scenario, we estimate that most of Glencore’s credit rating metrics would fall well outside the required ranges to maintain its IG rating, and that could happen as early as the next reporting period (FY15).”

From here, this is where those who throw bombs for a living believe is what is coming up next:

Commodity prices drop another 5%;

Rating agencies downgrade Glencore to high yield

(by Friday);

Glencore’s trading desk receives margin/collateral call immediately as commodities are T+0 settlement for margin (i.e. remember Duke&Duke in Trading Places);

Like AIG, the re-insurer of the credit markets, a significant amount of derivative contracts tied to commodities become an unknown.

MarketsMuse Global Macro merges with Strike Price seers with sage excerpt from 18 Sept edition of “Sight Beyond Sight”, the daily newsletter published by global macro think tank Rareview Macro and authored by Managing Member Neil Azous and rising star Michael Sedacca…For fans of the film Draft Day, this excerpt will resonate in a resounding way..For those who option traders who understand what VIX really is, and respect ideas that make sense, the following is a solid read.. The entire SBS edition can be found via link below..

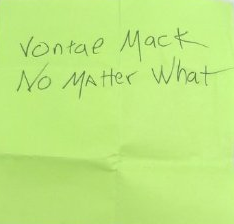

Volcano Trade Cont. – No Matter What, Vontae Mack

Neil Azous, Rareview Macro

Today, we are going to use a metaphor from a football movie to get our point across. Please note we expect to receive significant push back in this view, given we are going against the grain here. We are prepared for whatever you want to throw at us.

The movie, Draft Day, starring Kevin Costner, was an interesting (supposed) peek into the shrewd world of power plays among National Football League (NFL) general managers as they jockey to make the best deals on the yearly NFL Draft Day.

What grabbed the attention of viewers was the final, big reveal on a visual tease that ran through the whole movie involving a Post-It note. Kevin Costner’s character, Sonny Weaver, Jr, in only his second year as the General Manager for the Cleveland Browns, is feeling Herculean pressures from all sides – the arrogant owner, the difficult coach, and the even more difficult fans – to elevate the pitiful Browns into a team of national contenders. He has to make big, smart plays, which means we glimpse the political maneuverings at work, the salary cap issue, the various strengths and weaknesses of the key players his staff has been researching, as well as the poker game he must play with other GM’s in the NFL who are playing poker right back at him.

But all along, we see Sonny continually referring to the same little Post-It note he started with earlier that morning before he even left his house. He wrote the note himself, stuck it in his pocket, and then keeps referring to it as the day wears on and the stress level rises.

The draft begins. By making a painful trade that puts the entire future of his franchise on the line, Sonny secures the enviable #1 pick of the first round. Perfect, now he can get the obvious choice, the much-hyped #1 quarterback candidate. Instead, to the astonishment of all he unilaterally chooses the strong, but less regarded linebacker, Vontae Mack.

And this is what touched most viewers. At the end, after weathering the draft day storm, regardless that we all knew Costner would come out on top, it turns out what matters is that Post-It note. When he lays it on the table for the viewer, to finally read, it simply said:

No. Matter. What. He carried it with him all day. He clutched it in his fist when the heat was hottest and the fog was thickest. He fumbled it, strayed from it, even doubted it, but in the end, that simple determination governed him, guided him, through the storm. When no one supported him or even thought he was sane, the fictional Sonny Weaver, Jr, had one thing, his No Matter What.

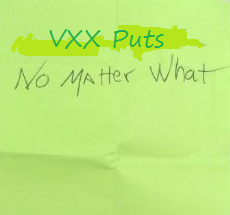

This is how I feel about the VXX put options we hold in the model portfolio.

You can insert CNBC in place of the Cleveland fans, my inner circle of trusted advisors in place of the coach, and our paid subscribers as the arrogant owner. But at the end of the day, we want to see how these moves lower in volatility plays out into next week. While we know we can book an additional 30-60 bps of PnL in the model portfolio in short order, we are looking to make a significantly larger amount if volatility continues to come in at the pace that has been witnessed over the last few days. The key point being, if VXX closes at 18 next Friday the below Volcano Trade would contribute an additional +4% to the NAV, on top of the 60 bps already realized. That is an opportunity we can’t ignore and we want to be a pig about it.

Yesterday before the Federal Reserve monetary policy statement we adjusted our short US equity volatility position for a second time.

Below is the sequence of trading events since the inception of this strategy but as a reminder the definition of the “Volcano Trade” is as follows: After an asset has had a large move in your favor and the option you own approaches a ~70 delta, you are able to roll the position to an out-of-the-money strike in two or three times the size, and capture an increasingly larger amount of profit if the move continues.

September 1st: Bought 10,000 VXX 9/18/15 $25 put options for $0.95 (VXX spot reference ~$30.50)

September 15th:Volcano Trade

Sold 10,000 VXX 9/18/15 $25 put options at $1.61 (vs. 0.95 cost basis)

Bought 20,000 9/18/15 $23.50 put options for $0.78 (VXX spot reference ~$24.20)

Net Credit: $0.03 or $30,000

September 17th a.m.:Super-Volcano Trade

Sold 20,000 VXX 9/18/15 $23.5 put options at $1.76 (vs. $0.78 cost basis)

3,520,000 premium taken in

Bought 30,000 VXX 9/25/15 $20.50 put options for $0.57 (VXX spot reference ~$22.00 at 9:57 a.m.)

Net Credit: $1.81 or $1,810,000

*Locked in 60 bps of PnL to the model portfolio

**The roll and the remaining options are FREE.

September 17th p.m.:Super-Volcano Trade Cont.

Bought 10,000 VXX 9/25/15 $20.5 put options for $0.36 (VXX spot reference $22.80 at 4:10 p.m.)

Current position: 40,000 VXX 9/25/15 $20.5 put options for $0.5175.

*Playing with House Money: Current premium $2,070,000 or 69 bps to the NAV.

Time Stamp: All updates were sent in real-time via Twitter.

Here are the following reasons for taking these actions:

The FOMC rate decision and approaching expiration date (i.e. today) had caused this week’s options to carry an implied volatility about double that of next week’s expiration.

The notional of the put options reached 150 bps of the model portfolio NAV, which considering they were less than 48 hours from expiration breached our rules-based discipline.

As a result we were able to accomplish three things.

We were able lock in profit whilst keeping a comparable amount of short delta. At the time of the sale we were synthetically short 1.5mm shares of VXX. By rolling the options our new synthetic short position was the equivalent of 835,000 shares.

We increased our gamma exposure to a further decline in US equity volatility by rolling down and out into larger size (i.e. 40,000 put options versus 20,000 put options).

We significantly reduced our vega risk by shifting into options with half of the implied volatility.

So far, this is nothing more than us sticking to our rules-based discipline. In fact, this was “text-book” trading and a classic example of adjusting a position on numerous occasions at the most opportune time. Following the FOMC release yesterday, the VXX even broke below our new strike and traded at $20.04.

Our view remains the same as it did on Wednesday when we introduced the “volcano trade” to you – that is, we expect US equity volatility to continue to decline into the end of the quarter. Additionally, the VIX curve continued to shift towards contango, with it trading inverted for a portion of yesterday’s session.

While headline writers want to suggest that uncertainty around the path of Fed policy is negative for risk assets the fact remains that investors believe lower-for-longer interest rates trumps that view and, as a result, they are not long enough market beta if the bounce back in risk into the end of the quarter continues. After all, that would be the biggest Bronx cheer (i.e. middle finger) of all right now.

We are mindful that hanging around this long may be overstaying our welcome, but hopefully the “volcano” will continue to explode through this new lower-lower strike with four versus two times the leverage since inception and dispense burning lava all over the nearby villages filled with dogmatic perma-bears who are looking for high volatility once again because they did not get unshackled from the Fed handcuffs.

Feel free to turn the CNBC volume to full blast, call our office, or send us angry emails to change my mind. But remember where I am coming from today and what our Post-It note says.

Neil Azous is the founder and managing member of Rareview Macro LLC, a global macro advisory firm to some of the world’s most influential investors and the publisher of the daily newsletter Sight Beyond Sight.

MarketsMuse editors were relieved yesterday after the Fed announcement for two reasons; the first being we were reminded that at least half of Wall Street’s Fed-watching pundits who get paid big bucks to predict events can be replaced by anyone who can flip a coin, as half of the pundits were wrong and arguably, at least half of those who were right, were probably right for the wrong reasons. One would need to have a transcript of the entire meeting to know what those Fed governors were thinking and saying.

The second relief comes from having watched a post-announcement color commentary on CNBC “Fed Winners and Losers”..which had sober and well-thought out thoughts from Rareview Macro’s Neil Azous and SocGen’s Larry McDonald

MarketsMuse Global Macro curators always look for substantive and objective observations from outlets that are truly substantial within the context of presenting thoughts and comments from experts followed by the most discerning investors. With that in mind, we salute the folks at UK-based Substantive Research for this morning’s note, which includes the following kudos to a global macro pundit who MarketsMuse takes credit for spotlighting early on….

Giving up on the European recovery theme?

Neil Azous from Rareview Macro published a great note that encapsulates a couple of big themes; Inflation targeting by central banks, and the impact of QE on equity markets, and in particular, European equities. There’s a big question about the relevancy of inflation targeting in today’s central bank user manual and Rearview has neatly put together a collection of quotes and academic work from central banks on this. with their own take on what this might mean for policy making in the future. How does this relate to European equities? If inflation targeting is no longer an effective policy tool it certainly limits policy options for the ECB. Azous also notes that European equities haven’t had the same tail winds that the US and Japan markets have had whether that is the direct result of QE policy, or corporate actions. This ”underperformance” shouldn’t signal less faith in the European recovery story, and he produces a laundry list of reasons to back the view for being long european equities here.

In the wake of recent weeks’ volatility and pricing dislocations across the exchanged-traded product space, news media and Mutual Fund marketers are having a field day putting the feet to the fire–and those toes being torched are connected to the universe of juiced-up and levered ETF and ETN products, as well as hedge funds that specialise in so-called “risk-parity funds” that employ lots of leverage. Is it fair to bash these ‘alternative’ strategies, or should the SEC require that the prospectuses (or is it “prospecti”?) for these protein-enhanced products have a coverage page that displays Caveat Emptor in caps? For those not fluent in Latin, the phrase means: Buyer Beware.

NYT Dealbook columnist Landon Thomas Jr. poses that issue in his a.m. piece: “Investment Strategies Meant as Buffers to Volatility May Have Deepened It”–and before pointing MarketsMuse readers to that article, MarketsMuse editors remind our readers that ETF red flags are nothing new. Levered products, often in the form of ETNs (exchange-traded notes) that seek to either mitigate risk or enhance returns via the use of futures products are notorious for being fit for trading market professionals only; not retail investors and not even for so-called sophisticated institutional investment managers.

Corporate bond ETFs have also been put on ‘watch lists’ in recent months, even though they are all the rage for many of the right reasons, including offering exposure and ‘greater liquidity’ for those needing to allocate investment funds to corporate debt issues across various industry sectors and ratings categories. That said, Apocalypse Watchers warn that when interest rates spike, corporate bond investors will all run for the exits together (to avoid mark-downs in their holdings) and the market-makers who specialize in ETF products connected to this asset class will be overwhelmed with nowhere to go–and no [reasonable] bid to offer to those sellers–simply because the glass-is-half-empty crowd contends those market-makers will be unable to find buyers for the underlying constituents as a means to hedge their purchase of the cash ETF product. That particular thesis has not yet been fully tested, but it does offer an agenda for spirited debate.

The Dealbook column does put context into the discussion with the following:

Defenders of risk-parity investing say that these investment styles are not set in stone and that portfolios can be recalibrated on fairly short notice to make them less vulnerable.

As for E.T.F.s, practitioners say that the funds to date have held their own despite some concerns over how portfolios were being valued during the very sharp market sell-off late last month.

Some of the more exotic E.T.F.s that rely on leverage to juice investment returns could in some instances be the “tail that wags the dog,” said Steven Schoenfeld, an early pioneer in E.T.F. investing and founder of BlueStar Global Investors.

“But the fundamental advantage of E.T.F.s — transparency, liquidity and variety — that remains,” he said.

What remains unclear, however, is how an investing community that has become accustomed to churning out safe and steady returns in a low interest rate, low volatility environment adapts to the new reality of wild market swings.

Such sharp ups and downs in the market are expected to become more frequent as the time approaches for the Federal Reserve to push interest rates higher.

People might as well get used to them, says Nicolas Just, a portfolio manager at Natixis Asset Management, a French fund company that oversees $904 billion in assets.

“These types of sudden market swings will become more and more frequent,” he said. “So you have to be prepared for them at any time.”

For RIAs who want to be smarter (and at the same time, earn CFP and CE credits, MarketsMuse points you to the Sept 17, Forbes Advisor Playbook iConference. Why? Well for one, Shark Tank shark extraordinaire Kevin O’Reilly a newbie ETF Issuer of exchanged-traded funds firm “O’Shares” (whose first product is OUSA) will be a guest speaker, along with a list of other industry luminaries that include Schorders’ Head of US Multi-Sector Fixed Income Andy Chorlton, Tim Palmer, Head of Global Interest Rates for Nuveen, Luciano Siracusano, Chief Investment Strategist for WisdomTree.

What does the day long session include? 6 timely topics ranging from Capital Markets and Game Theory to debating Optimal Active vs. Passive Portfolio Construction. MarketsMuse knows this will be a must-attend simply because the program is being coordinated by Julie Cooling of RIAchannel and our favorite ETF journalist, Todd Shriber aka ETF Godfather will be one of the program’s moderators.

What’s In It For You? 6 CFP and 6 CIMA CE Credits!