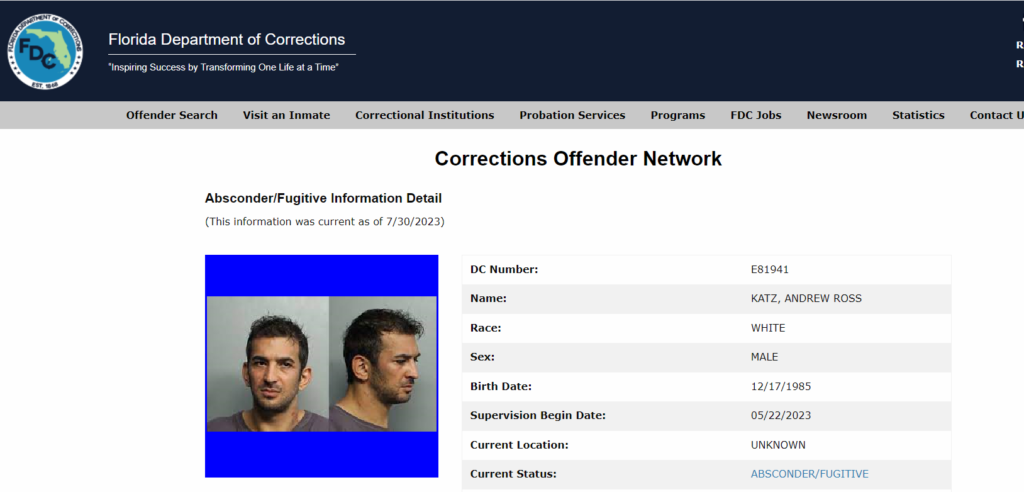

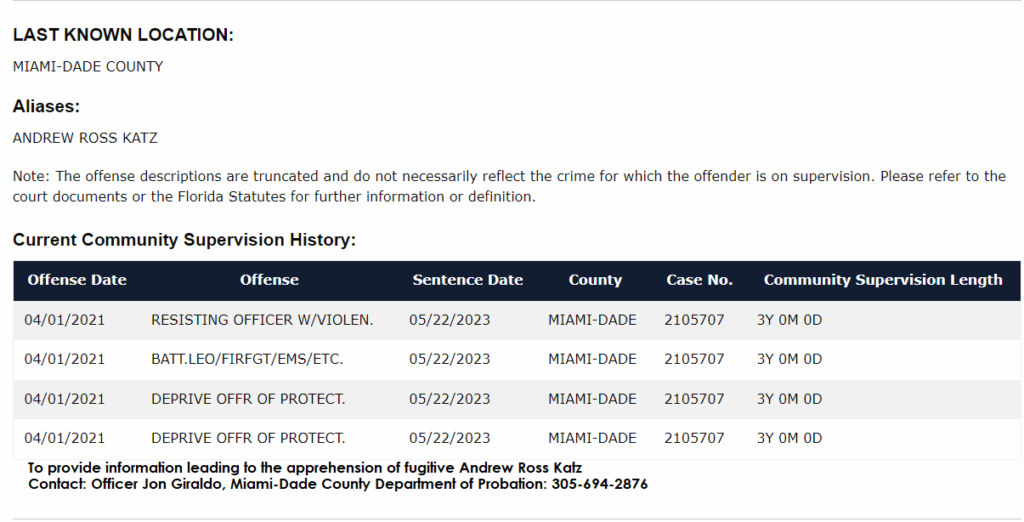

Andrew Katz, aka Ross Katz aka Drew Katz aka Stark Katz, a serial criminal who, at various times over the past seven years has claimed to be a “crypto entrepreneur” (operating through an entity known as “Seaquake”), and more recently, profiles himself on LinkedIn * as a “Fintech and “AI entrepreneur”, has fled Florida after being convicted on 4 charges of felony assault against law enforcement officers.

Fugitive Andrew Katz, aka Drew Katz, aka Ross Katz

*Note: In addition to using multiple aliases, Katz has recently taken to creating at least two LinkedIn accounts in an effort to obfuscate. In addition to the above LinkedIn profile, he is apparently using this LinkedIn profile, while he remains a fugitive from Miami-Dade County law enforcement.

Katz has been profiled via this outlet multiple times for his role in advancing securities fraud schemes, including defrauding crypto industry pioneer Brock Pierce, and for arrests on charges of assault, harassment, and stalking in Los Angeles and New York City. After being convicted in New York, in February 2022, Katz had already fled Manhattan for Miami, and a fugitive warrant was issued by New York authorities.

The latest event, which had Katz assaulting three police officers while they were attempting to arrest him on a domestic violence charge, led to his being convicted on four felony charges.

Katz is now being sought by Florida state law enforcement agencies. Those who have information as to Katz’s latest whereabouts are requested to contact the Miami-Dade County Department of Probation via 305-694-2876. DO NOT ATTEMPT TO APPREHEND THIS INDIVIDUAL; HE IS CONSIDERED TO BE ARMED AND DANGEROUS.

Bonds and Billions 3.0…Tradeweb Markets, one of the original electronic bond trading pioneers, which first introduced its dealer consortium platform in 1996, proved that patience is a virtue when it comes to monetizing enterprise value. The company raised $1.1billion via its Nasdaq-listed IPO yesterday (NASDAQ:NW). Illustrating investor attraction to owning a piece of the fintech company focused on fixed income trading, the company increased the number of shares they first planned to offer from 27.3 million to 40 million shares and upped the ante for the IPO price from a $24-$26 range to slightly north of $27. The IPO puts a $6bil valuation on the company–whose original investors include a consortium of broker-dealers.

Tradeweb CEO Lee Olesky photo courtesy of BRENDAN MCDERMID/REUTERS

Per snippet from Bloomberg News, Tradeweb intends to use proceeds to buy shares held by eight of the 11 large banks that own stakes in the company, including Bank of America Corp., Goldman Sachs Group Inc., Morgan Stanley and UBS Group AG, according to its registration statement filed with the Securities and Exchange Commission.

Tradeweb’s IPO is also the biggest for a financial services company in the U.S. since online lender GreenSky Inc. raised $874 million in May.

The offering follows benefits administrator Alight Inc.’s decision in March to postpone plans to raise up to $800 million in an IPO. Alight and Tradeweb are both owned by private equity firm Blackstone Group LP, which led the $17 billion acquisition last year of Tradeweb parent Refinitiv from Thomson Reuters Corp. Tradeweb, founded in 1996, builds and runs electronics markets for trading government bonds, derivatives, exchange-traded funds and other financial instruments over the counter. It handled an average of $549 billion in daily trades in 2018, according to its IPO prospectus.

Tradeweb posted net income of $160 million on $684 million in revenue last year.

As noted by Liz Hoffman of the WSJ, online venues are gaining ground in bond trading, digitizing orders that were once placed over the phone. At MarketAxess HoldingsInc., Tradeweb’s closest listed peer, trading volumes have more than doubled since 2014.

At $27, Tradeweb’s stock will list at about 30 times the company’s annual earnings. MarketAxess trades at nearly 50 times its earnings, while exchanges such as NYSE ownerIntercontinental ExchangeInc. fetch about 25 times their earnings.

JPMorgan Chase & Co., Citigroup Inc., Goldman Sachs and Morgan Stanley led the offering. Tradeweb will start trading Thursday under the symbol TW on the Nasdaq Global Select Market, according to the statement

Affiliates of Refinitiv will continue to hold about 54 percent of Tradeweb’s outstanding common stock, according to filings.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editorvia cmo@marketsmuse.com

NYSE DMM Citadel Securities started as a HFT prop trading firm

Something funny happened on the way to the floor of the New York Stock Exchange last week; Citadel Securities and Virtu Financial, two of the three biggest NYSE “Designated Market-Makers” aka “DMM”) –also domain experts in leveraging high-frequency trading technology—and now control trading in nearly 40% of NYSE listed stocks, announced they formed a consortium and raised $70 million to create an electronic stock exchange called Members Exchange, aka” MEMX” that aims to compete directly with NYSE as well as NASDAQ to list and trade shares of public companies. The news release likely didn’t sit well with NYSE Chairman Jeff Sprecher, as the announcement reads like a script that could be titled “Mutiny on the Bourse.”

A familiar scene..but not from the NYSE..yet.

Citadel Securities and Virtu Financial are not merely NYSE designated market-makers, an exclusive role granted by the exchange where the quid pro includes the DMM’s commitment to put their capital at risk while they maintain fair and orderly markets in the stocks they are assigned. Not your father’s NYSE specialists, Citadel and Virtu are also financial industry behemoths. Citadel is a global ‘alternative investment firm’ with $25b AUM and a high-frequency trading (“HFT”) domain expert. One of the original flash boys, the firm’s proprietary trading arm mints money using HFT tactics and strategies and is overseen by hedge fund billionaire Ken Griffin, whose net worth is estimated at $9.8bil.

Virtu Financial is also a $multi-billion platform. Firm co-founder Vinnie Viola is a former NYMEX Chairman, who became a high-frequency trading czar in the early 2000’s. Where Citadel’s Ken Griffith is a Harvard graduate, Virtu’s Viola hails from the US Military Academy at West Point. Now the owner of Florida’s professional ice hockey league franchise, Viola was on a Trump short-list to be nominated for US SecDef. Viola’s net worth of nearly $3bil might pale in comparison to Griffith’s pocketbook, but, what’s a billion here and billion there? Unlike Citadel, Virtu is a publicly-traded company ($5bil market cap), albeit the company’s shares are inauspiciously listed on NASDAQ (ticker: VIRT). In addition to its ‘seats’ at the NYSE, Virtu has a membership presence on nearly 125 exchanges around the world.

So, both of those boys are billionaires, both of their firms are high-frequency trading Goliaths that have multi-asset, market-making presence across a spectrum of electronic trading centers, and both became NYSE top DMMs by gobbling up old-line specialist firms. Virtu secured its initial spot on the NYSE floor in 2011 and Citadel joined the party with its Pac-man strategy of NYSE specialist firm acquisitions shortly after Intercontinental Exchange “ICE” bought out the NYSE in 2014.

Follow MarketsMuse on Twitter

Follow MarketsMuse on Twitter

Specialist traders work at a Virtu Financial booth on the floor of the New York Stock Exchange April 16, 2015. Shares of electronic trading firm Virtu Financial Inc rose as much as 24.6 percent during their IPO, valuing the company at about $3.23 billion. REUTERS/Brendan McDermid – RTR4XMJS

According to the launch announcement put out by MEMX, the $70 million in first round funding came from among others, Morgan Stanley, UBS, Charles Schwab, E*Trade Financial and TD Ameritrade. A total of nine firms are included in the initial business. There is only minor speculation as to why NYSE DMM GTS Securities is not currently involved in the new initiative-or at very least- they were not mentioned in the news release. Perhaps the simple reason is that GTS, which is also counted within the ranks of of multi-asset electronic market-makers, are NYSE loyalists and as relative newcomers to the NYSE, they are leery of aligning themselves with their sharp-elbowed tenants Virtu and Citadel in a yet-to-be-proven initiative and one that will certainly provoke the ire of Jeff Sprecher, the Chairman of the NYSE, and more importantly, the Chairman & CEO of NYSE owner Intercontinental Exchange (“ICE”) (NYSE:ICE). If you missed the memo, ICE is the global icon in the universe of financial exchanges; they own 12 other venues.

Why yet another stock exchange?! Does the equities market really need even more fragmentation?! Well, it’s all about the money. Duh.

According to insiders familiar with the MEMX initiative, the owners of Citadel and Virtu -as well as their sell-side partners, have long lamented the escalating cost of fees, both market data fees and the ‘extra fees’ imposed on “market on close” or “MOC” orders-the latter of which now represent the largest bulk of NYSE daily trading volume. Its no secret that those accessing the NYSE have increasingly pointed the egregious pricing to the point where those fees impede the ICE-owned venue’s ability to attract more order flow and better compete with other electronic exchanges that also trade in NYSE-listed companies.

One personal familiar with the MEMX’s pitch deck suggested, “These guys are tired of ICE taking in big market data fees and transaction fee revenue that they believe they are entitled to because they’re the ones making markets and providing liquidity. Their view is if were they to own their own exchange and offer lower fees, they could pocket it all themselves.” More telling as to the motivation is the narrative published on MEMX’s website: “As the only member-owned equities trading platform, MEMX will represent the interests of its founders….. and their collective client base..[comprised of retail and institutional brokerages] on U.S. market structure issues.” Sounds like a line straight out of Gordon Gekko’s playbook.

Are you following former hedge fund trader Larry Benedict’s daily $SPX trading ideas? “Go Home Flat 201”

As cited in the WSJ coverage of the story, MEMX website suggests their model is to “be more simplistic.” They state: “We will include a limited number of order types to promote simple and transparent interactions,” as well as “no speed bumps” to potentially hold up the trading process.” That ‘no speed bump” feature might sound like a slap at the upstart IEX exchange, owned by IEX Group and the ‘anti-flash boys’ equities exchange venue whose shareholders include major buy-side institutional investors. The IEX value proposition is to be ‘fairer to institutional investors’ and it limits access by “exploitative HFT trading firms” whose trade strategies include predatory, nano-second order entry and order cancellation.

ICE Chairman Jeff Sprecher (r) Benedict Arnold(l)

Or, the MEMX marketing message could be “click bait” when considering that they have purportedly approached IEX with a proposal to ‘take-over’ the nascent-stage and still-struggling-for-market-share equities exchange venue. Even flash boy fintech billionaires know that when it comes to trading technology, it is often cheaper to buy than it is to build. And, despite MEMX claims they can “easily replicate the NYSE technology and infrastructure at a low price point”, they know the $70mil they’ve put together is merely a seed round when comparing to the 7 year old IEX. which has taken in nearly $200mil since its formation and has only achieved less than 3% market share and the only company listing it has secured is electronic brokerage Interactive Brokers (IEX:IBKR). If MEMX can do a ‘take-under; of IEX, they’d have a ready-made exchange that its founders could pitch to the biggest NYSE-listed corporations.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

The never ending battle to electronify the secondary market for corporate bonds has yet another new entrant that aims to disintermediate corporate debt dealers that ‘control’ the trading in what has morphed from a $2trillion market to a $9 trillion marketplace during the last decade alone. As profiled by CNBC last week, the platform is called Wave Labs and its led by former Nordea Asset Mgt head trader and “fintech quant wonk”. Miles Kumaresan. Wave Labs purportedly as a new sauce that distinguishes itself from the current generation’s e-bond trading platforms; its powered by AI and algorithms that select corporate bonds based on buyer’s criteria. How Wave Labs helps to address the needs of sellers –which is arguably a crucial feature for any electronic trading platform–wasn’t addressed in the CNBC story

As best said by MarketsMuse Senior Curator ,”At risk of infringing on any copyright that Yogi Berra might have, “It’s Deja Vu All Over Again.”

MarketAxxes, which started after BondNet, had the right approach-which explains how/why it grew to what is now a multi-billion market cap company, even if its niche is mostly matching small size trades (under $5mil notional). That typical trade size

metric is illustrative of the obstacles that face any electronic platform that hopes to secure a presence in the corporate bond market. As one industry veteran pointed out, “Stocks are bought and [corporate] bonds are sold (by a salesman); if there’s a new black box that can actually pick the precise bonds that an institutional buyer wants, without having to deal with a salesman, that’s the holy grail.”

During the last 3-4 years, newbie disruptors who have sought to be the new kids on the bond block seeking to displace the role of bank trading desks have included among others, Liquidnet (whose pedigree is more tied to equities trading),Trumid, Electronifie, OpenBondX, and EMBonds. Their respective value propositions are the same: since the crisis of 2008, when bank balance sheets were forced to scale down inventory holdings, bank trading desks have not been able to address the liquidity needs of the marketplace. Each of the new generations of bond trading platforms has cute features, the most common being peer-to-peer trading, “RFQ” (request-for-quote) and also, scheduled auctions, as opposed to continuous bid-offer actionable price streaming. Electronifie and Trumid -both represented by fintech merchant bank SenaHill Partners, combined within two years of their respective start-up phase, as both struggled to get past B Rounds for funding in the course of trying to get a foothold in the marketplace.

Per the CNBC coverage by Hugh Son (@hugh_son), “Leaning on his quirky charm and the bravado of a true believer, Kumaresan says he has gotten meetings with some of the world’s biggest asset managers. He mentions their names — giants in the industry — and then requests that they stay out of print. As he tells it, the demonstrations of his prototype usually end abruptly as executives gush over its potential.”

One could argue those conversations end abruptly because Wave Labs is just the latest wave. “Kumaresan might be better off tuning into Kevin O’Leary, the CNBC pundit and notorious Shark from ABC’s “Shark Tank”, and consider licensing his technology to MarketAxxes or TradeWeb–as they’ve already got the most important two elements: credibility and customers.”

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

For the full story about Wave Labs, “This quant says his tiny start-up is about to blow up Wall Street’s $8 trillion bond trading monopoly” click here

Extra! Extra! XLC is the new ETF that ties telecom and media constituents into one exchange-traded fund! For those with a view towards latest and greatest ETF products, eyes and ears are on the Communications Services Select SPDR Fund(NYSEARCA: XLC) — “it tracks the Communication Services Select Sector Index and “seeks to provide precise exposure to companies from the media, retailing, and software & services industries in the U.S.”

Wow. That’s a bucket full of precision when considering the constituents of XLC include among others, Facebook (NYSE:FB), Alphabet Inc (NASDAQ: GOOGL), Activision (NASDAQ: ATVI), Verizon (NYSE: VZ), Comcast (NASDAQ: CMCSA), Netflix (NASDAQ: NFLX) The good news is that ETF maestro Andrew McCormond, Managing Director ETF Solutions for WallachBeth Capital distills the appeal of XLC, the latest innovative exchange-traded fund and one that might be the FANG-style ETF for portfolio managers who have yet to find a one-stop product that meets their portfolio allocation needs.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.

If you’re on a path to raise capital for a new hedge fund, a fintech initiative or a blockchain-startup, the first step is packaging your pitch and presenting the opportunity within a properly-prepared Prospectus. The go-to firm to assist you? Prospectus.com LLC. Straightforward, Smart and Bespoke Services.

Securities Token Offering to Displace Initial Token Offering Fad; BOX in JV with digital broker-dealer tZero to Create Securities Token Exchange platform

(Redistributed with permission; story from Traders Magazine)-Well, Matilda, the Boston Options Exchange (BOX) is plotting to create the first regulated exchange to list and traffic in securities tokens as a means to legitimatize crypto-centric assets via a just-announced joint venture with Patrick Byrne’s digital-themed broker-dealer tZero. For those who haven’t gotten the memo, Securities Token Offerings aka STOs are the next generation approach to the now de-fangled initial coin offering (ICO) construct–which have been lambasted by securities regulators in nearly every corner of the globe.

Now that crypto cool kids are finally getting the memo: “These are Securities!” , the proposed first fully regulated Securities Token Exchange is coming to the US-via the Boston Options Exchange.

tZERO, the digital-themed broker-dealer created by Patrick Byrne and BOX Digital Markets LLC (BOX Digital)-a subsidiary of Boston Options Exchange, announced it has formed a joint venture to launch the industry’s first regulated security token exchange.

Lisa Fall, Box Digital

On May 18, 2018, the two companies entered into a letter of intent to form an exchange to list and publicly trade security tokens for companies that issue, or convert existing stock to, security tokens. The proposed joint venture would be equally owned by tZERO and BOX Digital, with each having equal representation on the Board of Directors, together with one mutually agreed upon independent director. Lisa Fall, who currently serves as CEO of BOX Digital and as president of BOX Options Exchange LLC, would be the CEO of the joint venture.

“tZERO has proven to be a pioneer in the development and practical use of blockchain technologies for capital markets for a number of years,” said Ms. Fall. “tZERO’s track record and accomplishments in this innovative area, coupled with BOX’s expertise in operating a highly efficient and transparent equity options marketplace, made partnering together an easy decision and we look forward to building a world-class platform for listing and trading security tokens.”

tZERO plans to contribute cash and license tZERO’s blockchain technology for operation of the security token market. BOX Digital will contribute expertise and personnel toward obtaining regulatory approval and operation of the security token market. Approval of the U.S. Securities and Exchange Commission will be sought following execution of definitive documentation. Creation of the joint venture is subject to definitive documentation and customary conditions.

“Our partnership with BOX Digital Markets is a significant milestone that will create the first SEC-regulated exchange designed to efficiently trade crypto securities. Lisa Fall’s leadership, reputation and deep experience in the regulated securities exchange industry will be a major asset in achieving this objective,” said Saum Noursalehi, newly appointed CEO of tZERO. “Together, we will continue to work with the SEC as we develop a first-of-its-kind platform that will integrate blockchain capital markets into the current U.S. National Market System.”

“Now that pragmatic securities industry thought-leaders have figured out how to package crypto assets within the construct of a security so as to conform to the US regulatory regime, nobody can dispute the fact the genie is out of the bottle . “Securities Token Offerings (“STOs”) is a much more palatable approach, making way for a new mantra, “ICOs are dead, long live STOs”, until of course, another shoe drops.”

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.

For the full story from John D’Antona Jr. of Traders Magazine, click here

What’s Next? CryptoCurrency Bank License; Crypto Cool Kids New Goal: Stay Inside Regulatory Goal Posts

Coinbase Inc. and another cryptocurrency firm talked to U.S. regulators about the possibility of obtaining banking licenses, a move that would allow the startups to broaden the types of products they offer.

Coinbase, which operates the largest U.S. cryptocurrency exchange, met with officials at the U.S. Office of the Comptroller of the Currency in early 2018, according to a person familiar with the matter. Meanwhile, ivyKoin, a payments startup, in recent weeks sat down with officials at the Federal Deposit Insurance Corp., this person said. IvyKoin President Gary Fan confirmed the meeting.

The discussions included other topics, such as the firm’s business models, this person said. The companies might not seek a bank charter, which would significantly ramp up regulatory scrutiny. Whether they do so will depend on whether they decide the benefits of becoming a bank outweigh the costs.

A federal banking charter would let the firms swap a hodgepodge of state regulators for one primary federal one. The companies would also gain the option of directly offering customers federally insured bank accounts and other services, rather than partnering with existing banks.

A Coinbase spokeswoman declined to comment on the meeting. She said the firm is “committed to working closely with state and federal regulators to ensure we are properly licensed for the products and services we offer.” An OCC spokesman declined to comment.

IvyKoin pitches itself as a payments platform for government-issued currencies and cryptocurrencies that uses “know your customer” technology to detect money laundering. In the near term, ivyKoin is working with banks rather than trying to become one, but it asked regulators about a banking license to understand what might be necessary if it decided to apply, Mr. Fan said.

At the meeting, they “talked about our business model, what we hope to accomplish, next steps for us, key risks and how we can help banks manage that,” he said. “Our experience was really positive and [regulators] actually encouraged the discussion.”

Evan Fisher, Prospectus.com

“The past 18 months has seen an explosion of interest in ICOs, too many of which are unconstrained and outside the goal posts of what makes sense,” said Prospectus.com’s Evan Fisher, a former sell side investment banking veteran now consulting fintech firms on ICO best practices. “And, having the proper documentation in place for both investors and regulators is the most important part of any successful fund raise.”

Fisher is experienced in helping startups frame their value proposition properly and stresses founders need to ensure that when regulators do start to take a closer look at ICOs and cryptocurrencies, that all the necessary documentation is on file and easily obtainable.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.

Goldman Sachs, the venerable investment bank and trading house, has been called lots of things, including “Squid.” But nobody on Wall Street can dispute the fact that $GS is uniquely innovative and perhaps, a firm that can smell the trail of money better than its peers and explains why Goldman is opening a bitcoin trade desk. While JPMorgan CEO Jamie Dimon has repeatedly said bitcoin and other cryptocurrencies are at worst, the foundation to a Ponzi scheme, and at best, a passing fad, Goldman’s CEO Lloyd Blankfein has a different, more open-minded view. As evidenced by last week’s announcement, Goldman is opening a digital asset trade desk to accommodate a growing spectrum of hedge funds, endowments and foundations that already own digital assets or intend to deploy funds to the alt currency asset class. The new digital asset desk will be led by a fellow named Justin Schmidt, an MIT quant jock who previously worked at several quantitative investment management firms, including a hedge fund connected to The Schoenfeld Group.

Jason Schmidt, Goldman Sachs Crypto Trader

As reported by NYT reporter Nathan Popper, “…While Goldman will not initially be buying and selling actual Bitcoins, a team at the bank is looking at going in that direction if it can get regulatory approval and figure out how to deal with the additional risks associated with holding the virtual currency….Rana Yared, one of the Goldman executives overseeing the creation of the trading operation, said the bank was clear-eyed about what it was getting itself into…”

Ms. Yared said the bank had received inquiries from hedge funds, as well as endowments and foundations that received virtual currency donations from newly minted Bitcoin millionaires and didn’t know how to handle them. The ultimate decision to begin trading Bitcoin contracts went through Goldman’s board of directors.

Whether your company is a fintech startup planning a private placement offering, a crypto concern with a custom token offering that is seeking to raise capital from qualified or accredited investors via an Initial Coin Offering (ICO), a Securities Token Offering (STO)or if you are fast growth firm setting the stage for an initial public offering (IPO), a properly prepared offering prospectus or offering memorandum is required by your investors and industry regulators that govern securities offerings. Issuers seeking expert, yet affordable investor document solutions rely on experts at Prospectus.com.

Goldman has already been doing more than most banks in the area, clearing trades for customers who want to buy and sell Bitcoin futures on the Chicago Mercantile Exchange and the Chicago Board Options Exchange.

In the next few weeks — the exact start date has not been set — Goldman will begin using its own money to trade Bitcoin futures contracts on behalf of clients. It will also create its own, more flexible version of a future, known as a non-deliverable forward, which it will offer to clients.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.

Asset Management Industry is Notorious for Waste: Its About Blockchain, You Blockheads. NOT Bitcoin,

Blockchain Dapps Can Mitigate Risk of “Death By Drop Copy”

Any asset manager in today’s world who has more than $500 of AUM does not need to be fluent in the language of fintech, blocktech or be able to explain ‘the internet of things’ to understand the benefits of embracing blockchain dapps and the power of distributed ledger technologies. Any asset management firm that claims to be operating in the world of institutional fund management does need to get on the blockchain bus–or risk getting run over by it.

(courtesy of Prospectus.com LLC) As part of ongoing series “Its About Blockchain, Blockhead, Not Bitcoin!”, FT reporter Attracta Mooney hit the yellow zone of the target in a recent column profiling the how, where and why investment industry asset managers in UK, Ireland, Luxembourg, Hong Kong, Singapore, Taiwan and Australia could enjoy nearly $3billion in annual savings were they to embrace blockchain’s distributed ledger powered processes. After all, the new ‘internet of things’ blockchain value proposition for securities industry purposes is specifically designed to deliver at very least, greater efficiency in work flow, greater trust in the information being shared, enhanced transparency among trade processing constituents and more effective use of human capital resources.

Where? Let’s focus on the back office, the central place where administration of transaction reporting, accounting, trade processing and related legacy “drop copy” tasks take place. How? Distributed Ledger dapps leveraging the blockchain ecosystem are intended to mitigate duplicitous human interactions within the context of transaction affirmation, transaction processing, transaction reporting and transaction documentation.

If the above is confusing to you, or if you have not yet interrogated any of the thousands of simple-to-understand primers and tutorials on this topic (including the growing assortment of content pieces published in the news section of Prospectus.com) then you should

schedule a call with a fellow named George Chrisafis, who oversees fintech merchant bank SenaHill Partners’ Emerging Tech and Infrastructure Advisor Group. George is an IT industry grey beard with 30 years of domain expertise and his CV includes senior roles at the world’s biggest banks. When it comes to distributed ledger—as well as AI applications being developed for the securities industry, George is a reliable source of insight.

bring a high school or college-aged family member to your office and have them deliver a 5 minute dissertation on the topic of blockchain and distributed ledger, and to limit the cryptocurrency explanation to 1 minute. For some, the topic is confusing, but this is confusing, there is no shortage of simple primers and tutorials that frame the value proposition of distributed ledger.

Why Asset Managers Should Embrace Blockchain applications Barring above steps to independently confirm the thesis put forward in the FT article (excerpt and link below), let’s jump straight to the topic that best defines the purpose of asset managers: MONEY. Now let’s delve into the real cost and real expenses associated with their role(s) from both a human capital perspective and IT angle. [The information cost (research) and marketing expense components can be addressed in a different opinion piece}.

From a human capital expense perspective, transaction reporting tasks are notorious for their duplicative and redundant steps spread across various internal departments; many back-office professionals lament the high risk of Death by Drop Copy, simply because much of their time is spent drop-copying one file from one software application into an unconnected software application that performs a different task. From an IT perspective, let’s opine that most investment management firms are spending considerable sums each year on software licenses, software maintenance, and software administration. Succinctly, blockchain applications can save tens, if not hundreds of thousands of dollars to an established asset management firm—in turn enabling a firm to deploy those cost savings to revenue producing initiatives and recalibrating how internal human capital resources are better utilized.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor or email: cmo@marketsmuse.com.

(MarketsMuse fintech and blocktech curators extend our thanks to Prospectus.com LLC for the following contribution)-Bloomberg Intelligence reporter Jonathan Tyce wins the Valentine’s Day Award for Very Good Framing courtesy of his latest piece “Blockchain is Coming Everywhere, Ready or Not” –one of a series of articles by Tyce that puts the blockchain value proposition into proper perspective. Without suggesting there is any IP underlying the thesis advanced by Tyce, the opening sentence speaks volumes to those who are crypto challenged and have the misinformed view that blockchain = bitcoin=all kinds of bad things, including but not limited to ‘investment bubble”, Ponzi scheme, “pump and dump” ICOs where the Issuer is now hiding in the ‘dark web’ or sun-tanning in Belize, and lastly, ‘one of the things that lets people create crazy currency that isn’t even fungible’. Bid repeats: Its all about the blockchain, blockhead. Not bitcoin. Welcome to BlockTech.

Without intending to invite the BloombergLP copyright cops to castigate this blog for infringement violations, this blog has posted a series of original articles themed with the same title of this post. With that disclaimer, we’ve responsibly stayed within the goal posts and merely excerpted select portions of Tyce’s piece to advance smart thinking and give credit where due…

The applications of blockchain technology will spread in 2018 far beyond bitcoin and, perhaps more surprisingly, way beyond financial services. Significant disruption and new business opportunities are on the menu. Four of the most-critical benefits from distributed-ledger technology can be encapsulated within trust, transparency, cost and speed. Where will the disruption occur?

Blockchain is now a familiar term to many, though in most cases, its meaning will be inextricably linked to bitcoin after a 10-fold price surge in 2017 valued the cryptocurrency at more than $180 billion.

This is only one strand of the story for Europe and globally. The applications of blockchain technology will spread in 2018 far beyond bitcoin and, perhaps more surprisingly, way beyond financial services.

For starters, huge improvements in efficiency and transaction speeds, cost savings and enhanced security are on the menu, with significant disruption and new business opportunities likely to follow.

Distributed-ledger technology

Putting the semantics to bed early, blockchain is the name designated to a string or chain of transaction records (blocks), cryptographically signed with “hashes,” or digital signatures. Though undoubtedly the most high-profile application of blockchain, the bitcoin network is just one example of how cryptocurrencies and other transactions can use this technology.

Blockchain is effectively the means to create tamper-proof records of data and transactions — whether that is a money transfer, vote cast, medical record or change of property ownership. It is just one of a variety of decentralized database technologies that exist across multiple locations. These are known as distributed ledgers, and it is within these so-called DLT technologies that great opportunity exists.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor or email: cmo@marketsmuse.com.

Corporate Bond Market Transparency 4.0 MarketsMuse fixed income fintech curators, who have been on the beat for better than 8 years, were keen to cover this week’s inaugrual meeting of FIMSAC. e-Bond trading system founders, fixed income fund managers and fintech aficionados who have long lamented the limited degree of US corporate bond market transparency and less-than-likeable liquidity when trading corporate bonds in the secondary market and who ‘get the joke’ insofar as the benefits of embracing electronic trading platforms for corporate bonds might have a new advocate: SEC Chair Jay Clayton. At least that’s the way it appears based on comments Clayton made on Thursday while speaking to members of the Fixed Income Market Structure Advisory Committee (FIMSAC) during the group’s first meeting in Washington DC.

Whether Clayton does a typical White House walk-back after financial industry lobbyists turn up the heat in effort to preserve their legacy role controlling order flow and pricing remains to be seen. Because Clayton’s axe is less focused on institutional participants versus retail investors when stating “Main Street investors want liquidity; it is a sign of stability and resiliency..” he may not understand how the corporate bond works or the process by which individual investors become holders of corporate debt within their portfolios. If that’s the case, he’s perhaps perfectly suited to be a member of the present White House administration.

The importance of fixed income markets is “difficult to overstate,” Clayton said, noting the value of outstanding corporate bonds rose 76 percent between 2006 and 2016, compared to equity market cap growth of 40 percent.

“Individual investors are key participants in these markets, both directly and indirectly through pension funds and other pooled vehicles,” Clayton said, adding that he intends for the commission to continue focusing on these investors.

Courtesy of Law360 coverage: “Concerns regarding liquidity, or the ease with which buyers and sellers can match up in a given market, have been raised by bond market investors in recent years as big banks that serve as bond dealers and market makers, acting on new regulations imposed in the wake of the 2009 financial crisis, have reduced their balance sheets to cut costs and rein in risk.

The banks have shrunk their balance sheets by scaling back on the large bond positions they once held and used for creating markets for bond investors.

Some bond market participants have said the smaller balance sheets have led to reduced liquidity because it’s now harder to match buyers and sellers. That’s raised concerns that investors could lose lots of money should they need to quickly sell a large block of bonds into a market with few buyers.

Companies seeking to raise capital via private placement of debt instruments and in need of offering prospectus document preparation services turn to investor document specialists at global consultancy Prospectus.com

The wider concern is that if liquidity is already fragile it could essentially freeze during a time of financial stress when lots of investors choose to sell their bonds. When that happens, as it did in 2007, a domino effect kicks in which, given the size and reach of global bond markets, poses a threat to the world’s economy.

Committee member Gilbert Garcia, managing partner of Houston-based bond manager Garcia Hamilton & Associates, said he trades daily and has firsthand knowledge of a lack of liquidity during normal trading conditions, especially for large blocks of bonds.

“What we need to do is be ready for the next crisis,” Garcia told other members of the committee.

Scott Krohn, Verizon Communications Inc.’s treasurer and also a committee member, raised a concern that yields on Verizon’s highly liquid bonds could be vulnerable to extreme volatility during periods of financial stress as investors flee riskier securities in favor of safer ones, such as Verizon’s corporate debt.

When it comes to corporate monikers, MarketsMuse fintech curators are big fans of catchy names and have made it a New Year’s resolution to compile and share a weekly list of firms that earn special recognition within the burgeoning world of blockchain, bitcoin and crypto handles. And, the winner for the first week of 2018 is”BnkToTheFuture.” No, its not a futuristic bank run by Doc Brown and no, Marty McFly is not the crypto credit lending officer. Its a current generation “cool kids only investment bank” that appears to be based in Hong Kong and staffed by the now ubiquitous-to-the-industry line-up of slick looking folks from UK, HK and of course, Eastern Europe. Arguably, the management team can be considered blockchain industry pioneers given this firm was formed way back in 2011.

Our thanks for guidance to this “Global FinTech, Bitcoin and blockchain online investment platform” goes to TradersMag Senior Editor John D’Antona who pushed this release to us, which is chock full of mentions of ‘crypto industry celebrities’ who recently joined the firm’s advisory board. Our compliance desk loved the “About BnkToTheFuture” section of their press release; it conforms beautifully with global financial industry best practice protocols: “The platform is in line with international financial regulations and over $200m has been invested in deals listed on its platform.” Below is an excerpt of the news story:

Simon Dixon, CEO BankToTheFuture

BnkToTheFuture today announced its token sale advisory board, with executives from Civic, Smith + Crown, Abra, BitAngels, and more signing on to help BnkToTheFuture launch a tokenized secondary market and due diligence platform for equity tokens. BnkToTheFuture’s online investment platform already brings vetted deals to qualifying investors and has invested in many of the most valuable companies in the sector, and will now incorporate its BFT cryptocurrency token to reward due diligence, deal flow analysis and investor relations on prospective and current deals.

“Investors in today’s burgeoning ICO landscape are seeking more professionalism, accountability, and compliance, while equity investors are seeking greater liquidity and trading,” said Civic CEO and BnkToTheFuture Identity/KYC Advisor Vinny Lingham. “BnkToTheFuture provides this gap in service, and I’m excited to see this project grow through its next phase.” The company’s press release includes: “The platform is in line with international financial regulations and over $200m has been invested in deals listed on its platform including BitFinex, BitStamp, Kraken, ShapeShift and over 100 others.”

Joining BnkToTheFuture’s advisory board alongside Lingham are Jonathan Smith, Civic Co-Founder and CTO; Bill Barhydt, CEO of Abra; Diego Gutierrez Zaldivar, CEO and Co-Founder of Rootstock (RSK), Michael Terpin, CEO of Transform Group, Founder of CoinAgenda, and Co-Founder of BitAngels; Sunny Ray, President of Unocoin; David Johnston, Chairman of Factom and Co-Founder of BitAngels; Li Huo, Director at Huobi; Adam Vaziri, Blockchain lawyer and Director at Diacol; Brian Lio, CEO at Smith + Crown; Matt Chwierut, Researcher at Smith + Crown; Tony Simonovsky, CEO of InsightCryp.to; and David Drake, Chairman at LDJ Capital. BnkToTheFuture will continue to list new advisors here.

Whether your company is a fintech startup that is planning a private placement offering, a crypto concern with a custom token offering that is seeking to raise capital from qualified or accredited investors via a Initial Coin Offering (ICO), or if you are fast growth firm setting the stage for an initial public offering (IPO), a properly prepared offering prospectus or offering memorandum is required by your investors and industry regulators that govern securities offerings. Issuers seeking affordable investor document solutions rely on experts at Prospectus.com.

“While building BnkToTheFuture’s advisory board for our upcoming token launch, we sought leaders in the blockchain industry and those who have been consistently involved advocating for Bitcoin from very early on to help guide our efforts to further develop a transparent platform compliant with regulatory requirements,” said Simon Dixon, CEO of BnkToTheFuture. “We’re confident that our advisory team of experts will be instrumental in this process.”

Already popular as an online investment platform with 45,000 qualifying investors and over $200 million invested in rounds listed on its platform including companies like Kraken, BitFinex, BitStamp, ShapeShift and others, BnkToTheFuture will incorporate blockchain technology to allow for the trading of equity tokens and will issue its own token, BFT, to support deal flow analysis, due diligence and investor relations on the platform. BFT will be available in a public token sale in February 2018.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.

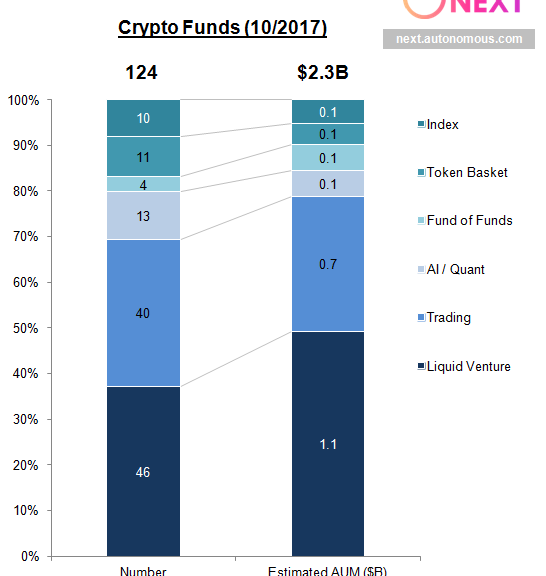

Crypto Hedge Funds Get Their Greenwich On. If the MarketsMuse curators have avoided bidding on and publishing tick-by-tick coverage of “crypto mania” and bitcoin bubblelicious bytes akin to our media industry brethren, its only because we were arguably a pioneer when, starting in 2014, we first started framing the bitcoin and distributed ledger evolution under the label fintech. OK, one of our editors was conflicted–having purchased a few bitcoins back when paying $100 for the cryptocurrency caused laughter from peers with CT license plates on their Teslas. What a difference a day makes (ok, lets call it a few hundred days).

Every famous hedge fund wonk, from Steven Schonfeld to “Stevie” Cohen, and tens of dozens of others have either carved out a crypto trading strategy or are planning to do so. After all, volatility is every trader’s elixir and now that CME, CBOE, NASDAQ and as of Dec 20 announcement, NYSE ARCA have all blessed bitcoin, the opportunity to trade crypto derivatives on a regulated exchange is impossible to resist for the ‘hedgies.” Even Thomas Peterffy, the hard-charging Republican and multi-billionaire founder of Interactive Brokers, has walked back on his earlier position in which he said he would not allow IB customers to trade bitcoin products; now they can when they post the required margin. Hey, Thomas’s membership fees at Mar-a-Lago are going up and if bitcoin trading can create a new commission silo for the “Professional’s Gateway to the World’s Markets”, it makes sense to get in on the action. (Breaking News: NYSE ARCA TO LIST 2 BITCOIN ETFS).

As reported by WSJ’s Dec 20 column, “Big Hedge Funds Want In On Bitcoin”-— Already, there are around 20 funds, managing a total of roughly $2 billion in assets, that solely or predominantly trade cryptocurrencies, as tracked by an index compiled by Chicago-based data group HFR. The asset total highlights how it has largely been smaller funds that have traded bitcoin, though HFR President Kenneth Heinz says the number of funds could double in size in the first quarter of 2018.

OK $2b is “Peanutsville” when it comes to the trillion dollar hedge fund industry which deploys capital across multiple asset classes and strategies. But, according to the WSJ story, as well as off-line conversations with HF titans, lots of folks who might have been allergic to peanuts are now looking to put on spreads with LEAP style maturity dates.

Lest one forget, a whole bunch of smarty pants types in VC land dismissed two twins by the name of Winklevoss for claiming to have been the brains behind Facebook. Even their lawyers laughed at them when they insisted on taking then private shares in FB instead of $50m in cash when Mark Zuckerberg offered to settle the ‘misunderstanding.’ The shares soon became worth $300m and the twins then parlayed some of that into buying up 1% of the bitcoin market. The Winklevoss boys were laughed at again when they were the first to file for a bitcoin-based exchange-traded fund (ETF). As their initial $10m stake in bitcoin blossomed into $1 Billion (on paper), those twins also created what is viewed as the most robust electronic exchange in the bitcoin ecosystem and is arguably worth as much as $1b also–just because someone would likely pay that much to take over the system.

Evan Fisher of Prospectus LLC, a global consulting firm that provides hedge fund set up guidance, business plan writing services, preparation of investor offering documents and more recently, whitepaper writing and ICO offering documents, sums it up by saying, “The calculus for hedge fund players allocating risk to this new asset class is pretty simple, if their peers are diving in, they need to.”

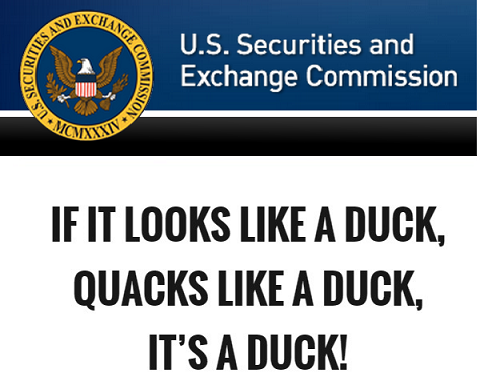

Initial Coin Offerings [Finally] Get SEC Attention; The Duck Test 3.0.

For those who believe the US SEC is slow to react when reining in and/or reigning over new-fangled investment products, the evidence indicates you are accurate. After all, recent history regarding sub-prime debt sold to unwary investors, Madoff-style investment management scams, payment-for-order schemes advanced by exchanges, and high-octane exchange-traded notes unsuitable for retail investors are just a few of the topics that made it out of the gate and far into the fields before investor advocates rang the alarm bells at the front door of the US Securities & Exchange Commission.

There have been more than 160 of these ICOs this year, which have collectively raised more than $3 billion, according to data from research firm Coindesk. Before this year, ICOs had raised a total of about $300 million going back to 2014.

SEC Chair Jay Clayton Photo: Andrew Harrer/Bloomberg News

In defense of the bureaucrats based in Washington, their job description is arguably less a function of evaluating investor-suitable products and Wall Street selling practices as opposed to their primary role of chasing the horse after its out of the barn. After all, the folks who offer SEC staff with new investment product insight and regulatory recommendations (and tickets to concerts and sports events) are highly-paid lobbyists who represent Wall Street investment banks that have an agenda–to make fees from selling investment products and to ensure there is as little as possible regulatory oversight on their activities. Thanks for reinforcing that view, Mr. Trump!

But, in the case of the latest innovative product known as initial coin offerings, where innovators are raising money for an assortment of business models through issuance of bitcoins vs traditional shares in a company, Wall Street banks are finding themselves short of having a controlling role in the underwriting, sale and secondary market trading of these ‘instruments.’ Whilst the likes of Goldman Sachs and other fintech-friendly firms are racing to find their sweet spots in the digital ledger, blockchain and bitcoin space, suffice to say those investment banks are not happy about losing out on what would have been tens of millions of dollars in underwriting fees that could have been generated from the more than 160 private placement offerings that raised nearly $3billion since the beginning of the year, as well as potentially hundreds of millions of dollars in potential underwriting fees based on the pipeline of ICO deals in the pipeline.

So, it should come as no surprise that despite the ongoing string of announcements about new ICO issuance, the SEC has seemed to be asleep at the wheel for months insofar as issuing any regulatory edicts, leading some cynics to suggest that lobbyists from Wall Street have more recently whispered into the ears of SEC Chair Jay Clayton and compelled him to assert the power of SEC over those conducting initial coin offerings.

MarketsMuse readers are directed to coverage by Prospectus.com, “SEC Invokes Duck Test for Initial Coin Offerings-ICO Alert” via this link

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.

Well Matilda, as if the universe of corporate bond electronic trading platforms isn’t crowded enough, despite clear signs of consolidation taking place for this still nascent stage industry (e.g. upstart Trumid’s recent acquisition of infant-stage Electronifie) , one more corporate bond e-trading platform has its cr0ss-hairs on the US market. The latest entrant is UK-based Neptune Networks, Ltd., a consortium controlled by sell-side investment banks that has inserted electronic trading veteran Grant Wilson as interim CEO. Neptune’s lead-in value proposition’ is perfecting the IOI approach to capturing liquidity, and also offers a tool kit of connectivity schemes that bridge buyside and sell-side players.

Grant Wilson, Interim CEO Neptune Networks

Promoting indication-of-interest orders ( pre-trade real-time AXE indications) as opposed to actionable bid-offer constructs that are ubiquitous to equity trading platforms, is a technique that other US-based corporate bond trading platforms are already advancing. Neptune is also not alone in their positioning an ‘all-to-all’ model as a means to inspire buy-side corporate credit PMs and traders to embrace electronic trading, a seemingly counter-culture technique that enables them to swim in the same pool as sell-side dealers aka market-makers. The distinction that Neptune brings to the table is girth and size, thanks to its sponsors Goldman Sachs, JP Morgan, Credit Suisse, Morgan Stanley, UBS, Citi and Deutsche Bank, each of which maintain board seats. Unlike the other players in the space that are focused on building a “round lot marketplace” (as opposed to retail size orders that MarketAxxess (NASDAQ: MKTX) specializes in, Neptune carries over 14,000 individual ISINs daily, claims that its average order size is 5mm, total daily gross notional in excess of $115bn, and according to Neptune’s marketing material, over 22,000 individual ISINs have been submitted to the platform since January 1st.

Lots of e-bond trading platforms, but none are incorporating bond ETFs, at least not yet.

As compelling as Neptune’s value proposition is, some corporate bond e-trading veterans are quietly wondering whether these initiatives are somehow missing the memos being circulated throughout the institutional investor community profiling the rapid adoption of corporate bond ETF products in lieu of their long-held focus on individual corporate credits.

According to one e-bond trading veteran, “Anyone who follows the trends [and follows the money] can’t help but appreciate that a broad assortment of Tier 1 investment managers, RIA’s and even public pensions’ use of bond ETFs is increasing in magnitude by the week, not the quarter. If you’re operating an electronic exchange platform for corporate bonds, and your users are rapidly increasing their use of fixed income exchange-traded funds, having a module for ETFs would seem to be a natural next step.”

Others in the industry have suggested to MarketsMuse reporters that enabling users to trade the underlying constituents against the respective corporate bond cash index along with a module for create/redeem schemes, or even a means by Issuers can distribute new debt directly seems to make “too much sense.” But then again, these same industry experts acknowledge the political landmines that would most assuredly be encountered by those trying to disrupt and innovate within corporate bond land are perhaps too much for those who need to prove their business models before aiming at new frontiers. Continue reading →

And The Winner Is….Institutional Investor Presents 2017 Top 40 Trading Tech Top Guns

Who says trading technology wonks are under-appreciated within the context of recognition by industry followers? Certainly not MarketsMuse fintech curators, and definitely not Institutional Investor Magazine, which brings us their annual ranking of the top trading technologists on the planet.

“The Trading Technology 40 were selected by Institutional Investor editors, taking into account nominations and input from industry experts. The leadership criteria include recent and career accomplishments and contributions to individual companies and to the industry at large; scope and complexity of executive responsibilities; and pure technological innovation.”

The 2017 ranking was compiled under the direction of II Senior Contributing Editor Jeffrey Kutler. Profiles were written by Kutler; Asia Bureau Chief Allen T. Cheng; Staff Writer Jess Delaney; and Senior Writers Frances Denmark, Imogen Rose-Smith, and Julie Segal.

Here’s an excerpt from the just published findings..

Modern financial markets could not function without automation. Traders, counterparties, and transaction-processing infrastructures depend on automation to cope with the avalanches of data that are both generated by the markets and essential to their reliability and integrity. Despite occasional glitches — which have become progressively less frequent and less severe since the disastrous flash crash of May 2010 — it all happens so smoothly that it is easy to take the technology for granted.

That’s a credit to the technologists of the trading world featured in this year’s Trading Technology 40. Whether they work in equities, fixed income, currencies, commodities, or derivatives, the executives listed here are pioneering solutions to countless problems presented by the size and complexity of markets.

Whether your fintech or trading technology company is planning a private placement offering available to a select universe of friends and family, qualified investors or an initial public offering (IPO) via an exchange listing, a prospectus or offering memorandum is required by your investors and industry regulators that govern securities offerings. The experts at Prospectus.com have prepared business plans, offering documents and more for a discrete universe of financial technology start-ups.

To view the winners and their biographies, go straight to II’s article via this link

Those of us who have worked in and/or around the world of electronic trading for more than 15 minutes readily know about REDI, the ubiquitous direct access execution platform for stocks and options that was introduced by Spear Leeds & Kellogg in 1987 to its professional clearing customers, a universe that grew to thousands of professional traders across the globe. For those not old enough to remember Spear Leeds aka SLK, it was one of the financial industry’s largest specialist firms with it biggest boots on the ground on the NYSE and Amex, and for decades, one of the largest clearing agents for stock and options exchange members and upstairs prop traders. SLK was also one of the industry’s most recognized upstairs market-makers until being acquired by Goldman Sachs in 2000 for a whopping $6.5bil. For those in the know, Goldman’s record-setting acquisition was attributed in part to a fellow by the name of Neil DeSena, “a boy from Bayonne” whose name was synonymous with REDI from the day it was first introduced in 1987, to the day the platform came under Goldman Sachs stewardship, to the day in 2016 when REDI was sold by GS for $1bil to Reuters Plc, and for every day in between, including now, when a trader somewhere in the world uses REDI to send a buy or sell order for stocks, options and/or futures into the now global OEMS platform.

History has already shown that the usually prescient Goldman Sachs wanted not only SLK’s prop-trading business and its clearing customers-which delivered hundreds of millions in high-profit revenue , GS also wanted to be at the forefront of electronic trading and SLK provided that. And, it was Neil DeSena who offered that entree. Until his untimely passing last week, barely three months after celebrating his 52nd birthday, Neil DeSena’s name and the brand name REDI remained forever intertwined, despite the fact that Neil had retired from his role as a Goldman Sachs MD several years ago. It was DeSena who was widely-credited for taking the REDI electronic platform from a closed stock and options order routing system for SLK clearing customers to a a billion-dollar, global OEMS platform synonymous for trading stocks and listed equity options. Upon Goldman’s acquisition, Neil became a GS managing director and under their banner, he built REDI into the industry leading global multi-asset trading system, expanding data centers and global networking through Europe and Asia with full interdependency/redundancy, creating a fully 24×7 global institutional trading platform. In 2015, Goldman sold REDI to Reuters for a cool $1bil.

Ironically, Neil DeSena was not an inventor, nor a prodigy software wonk, and not an MIT-educated computer geek or a Harvard MBA. Neil came to the financial industry as most did ‘back in the day’; he was a humble, but eager “boy from Bayonne” who came from a middle-class family and like so many others from the hamlets near the world’s trading centers, he aspired to work on Wall Street’s trading floors. As noted in his bio at SenaHill Partners, the fintech merchant bank Neil co-founded in 2013 with Justin Brownhill after retiring from Goldman, Neil’s first Wall Street job was typical to that of other 23 year olds; he scored an entry-level, back-office clerk (for retail broker Quick & Reilly). After rising through the ranks and learning how to leverage technology and lead people, Neil joined SLK in 1992, where he became the first employee of REDI. To the tens of hundreds that Neil since touched throughout his personal and professional life, ‘the rest is history’, but Neil’s history and the legacy he leaves behind cannot go without mention.

Neil DeSena was a classic innovator and entrepreneur who always maintained a prescient view when it came to the future of marrying technology and financial markets. He was less a student of technology than he was a student of human behavior and the inherent opportunities that technology-based solutions could provide to one of the world’s biggest industries. Better than most, including the legions of Wall Street technology and business development gurus, Neil had an innate and intimate understanding of the the mindset of those who navigated stock and options marts and what they would need to be more efficient and more effective, before those savvy-traders knew themselves. It was Neil’s thought-leadership, his uncanny ability to gain the trust and confidence of those around him, his foresight as to how/where/why technology could be leveraged, and perhaps most of his all, his endearing personality and sense of integrity that served as a benchmark for so many people he encountered.

Never one to rest on his laurels and certainly not like so many from the finance industry who aspire to build wealth for themselves and retire to a life of luxury, when Neil left Goldman Sachs, it took little time to decide “What’s Next?” Joining hands with Justin Brownill, one of the trading tech industry’s most successful entrepreneurs, the two formed SenaHill Partners in 2013 and framed the firm to be one of the very first fintech merchant banks focused on fostering upstart and industry disrupting financial technology firms. Since the firm’s creation barely four years later, more than two dozen finance industry tech pioneers have joined as network advisory board members; each contributing expertise, relationships and insight in their respective areas and helping to review nearly 2500 business plans submitted to SenaHill. The collective of professionals has gained the attention of finance industry and tech industry titans and has put wind behind the sails of dozens of disruptive startups focused on areas from bitcoin and distributed ledger to financial-flavored media platforms.

Irrespective of the degree of success enjoyed by enterprising start-ups that DeSena and Browhill have helped guide, Neil DeSena’s truest success is illustrated less by counting the literally hundreds of people who came to offer kindness and support this past weekend to Neil’s wife Carolyn and his three young children, Madeleine, Neil Anthony, and Jack, but more by the legacy he leaves; Neil always reminded those who were smart enough to listen that “material success is fleeting; honor and integrity are the most important virtues, as it those qualities that we should all be remembered for.”Continue reading →

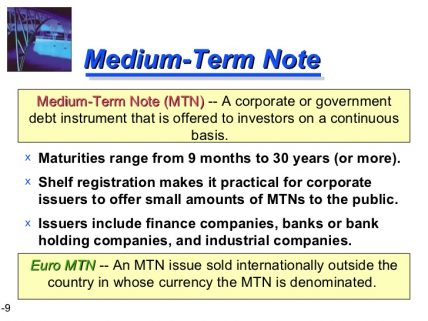

Fintech Fixed Income Trading & Fragmentation-What’s Next? A Venue for Private Placement Bonds & MTNs

Despite the seeming oversupply of electronic bond trading initiatives, the convergence of fintech and fixed income trading continues to spawn new electronic trading start-ups, bringing the total industry count to 128 venues. The latest player, dubbed “Origin Markets”, aims at filling a void in the $1.5 trillion Medium-Term Note space aka private placement bond market. The “still-in-beta mode” initiative is based in the UK and backed by a consortium of global banks led by BNP Paribas, Bank of America Merrill Lynch, Societe Generale and Credit Suisse.

Raja Palaniappan CEO Origin Markets

Origin’s founder and quarterback is Raja Palaniappan, a former Credit Suisse flow trader and MIT wonk who cut his teeth trading MTNs at various firms during the past 9 years and was most recently a VP responsible for making markets in investment grade and crossover corporate bonds and CDS at Credit Suisse.

A spokesperson for UK-based Origin said its platform “simplifies issuance in the medium-term note private placement market by acting as a central information source.” The business model allows dealers to receive targeted funding levels from issuers on a single platform and allows users to foster new relationships through cloud-based technology and bank-grade security.

“[Issuers] can optimise their funding using the built-in cross-currency pricer, comparing their funding levels to their own and their peers’ levels in the secondary markets,” Origin said.

Joakim Holmstrom, head of funding at Municipality Finance, explained the platform makes the medium term note process more efficient and provides access to a broader pool of dealers. Ben Powell, head of funding for IFC, added that Origin’s platform “simplifies what was once a manual process prone to inefficiency. It allows us to manage our dealer communication in one central place.”

The platform’s full launch is expected later this year and brings the total number of electronic fixed income platforms to 128, according to a recent compilation of platforms by front office trading consultant John Greenan.

Bob Mahdavi, the CTO for private placement bond documentation firm Prospectus.com stated “The MTN market is indisputably one of the largest sectors in terms of number of issues, yet it is populated by thousands of private issues that don’t typically lend themselves to being traded in an electronic venue.” Added Mahdavi, whose firm works with tens of dozens of Issuers, as well as attorneys and boutique investment banks throughout Europe and Asia in preparing debt offering documents, “You can build it, but will they come?”

According to fintech merchant bankers at SenaHill Partners “When considering the still nascent stage impact of electronic venues focused public company investment grade corporate bonds, including the likes of startup Electronifie among others, a platform that can prove truly effective and liquid for MTNs can prove to be a big challenge, albeit the backing of big banks does provide some wind in the sail.”

If you’ve got fintech fever, or just a hot tip, a bright story idea profiling global macro, fintech, ETFs, options, or fixed income markets, or if you’d like to get visibility for your firm through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, etc., please reach out to MarketsMuse Corporate Communication Conciege via this link

As noted in a 11 Jan story in TheTradeNews and citing the work of Greenan, between November 2016 and January this year alone, 14 new fixed income trading platforms joined the market.

“…The asset class is overcrowded with trading venues as regulation forces the structure of fixed income across instruments away from a centralised model – mostly due to bank balance sheet constraints – towards a decentralised model….Market participants have said the explosion of venues is causing fragmentation and a ‘liquidity drought’ in global bond markets.”

Large buy-side firms and asset managers have the opportunity to act as price makers rather than price takers, according to a quarterly report published by the International Capital Market Association (ICMA) this week.

The report said the bond market has seen a decrease in ratio turnover, despite an increase in market size and overall turnover against a backdrop of bond issuance, as issuers take advantage of low interest rates globally.

Joanna Cound, head of public policy EMEA at Blackrock and a member of the ICMA board, explained this has led to liquidity in fixed income markets suffering, something regulators have taken a greater interest in over the last year.

Wow. That’s a bucket full of precision when considering the constituents of XLC include among others, Facebook (NYSE:FB), Alphabet Inc (

Wow. That’s a bucket full of precision when considering the constituents of XLC include among others, Facebook (NYSE:FB), Alphabet Inc (