Facebook’s Mark Zuckerberg (who needs no further introduction) and his wife Priscilla are celebrating the birth of their first child ( a girl named Max) by announcing that he and his wife will move 99% of their shares in Facebook (NYSE:FB) to a charitable trust. For those without a calculator, that’s $45bil of net worth that will go to a trust.

Wow. OK…a big announcement that makes CNBC wonks slather with commentary..but there’s lots of small print in the plan…this is a long-term allocation to the newly-created trust. It will be funded in incremental stages, etc etc.

MarketsMuse followers who noticed our June 29 2015 post “What’s Next? ETFs for Crowdfunding?” and our curator’s somewhat parody-centric, but now prescient view that someone in the ETF world would soon come up with a crowdfund industry exchange-traded product can now share this post with others–as that prediction has come to fruition.

Per brief blurb from Traders Magazine–Yes, Matilda–the ahead-of-the-curve folks at Wisdom Tree have thrown the gauntlet down…

A Crowdsourced Index Fund

In what could be the ultimate filing of the cyberage, private label ETF firm Exchange Traded Concepts has filed for a fund based on an index provided by Centerboard Ventures Corp. The ETF will track an index created by users of the firm’s mobile app, the CrowdInvest Internet Platform.

The CrowdInvest Wisdom ETF’s underlying benchmark can include any U.S.-listed stock with an average daily trading volume of at least $15 million over the preceding 20-day period. Every month, the users of the app can vote on long, short or flat positions for eligible stocks. The top 35 companies with the most long votes after their short votes are subtracted and selected to be the index components for the following month, according to the prospectus. Index weightings are based on the number of votes the components received.

However, only four components can be replaced each month, and if there are not enough votes to determine weightings, all of the components are weighted equally.

This would be the first ETF to track a crowdsourced index. Presumably, investors in the fund would have to have a certain amount of trust in the judgment of the app’s users. The prospectus lists “Platform User Bias” as one of the ETF’s risks, and warns that the app users voting on the index’s components are not necessarily professional investors and could be subject to “cognitive and emotional biases.”

Vident Investment Advisory will serve as the fund’s subadvisor. The filing did not include a listing exchange, a ticker or an expense ratio.

There continues to be a call for clarity with regard to the topic of corporate bond ETF liquidity and where/how corporate bond ETFs add or detract within the context of investors ability to get ‘best execution’ when secondary market trade in underlying corporate bonds is increasingly ‘illiquid.’

This not only a big agenda item for the SEC to wrap their arms around, it is a challenge for “market experts” to frame in a manner that resonates with even the most knowledgeable bond market players.

MarketsMuse curators noticed that ETF market guru Dave Nadig penned a piece for ETF.com last night “How Illiquid are Bond ETFs, Really?” that helps to distill the discussion elements in a manner that even regulators can understand.. Without further ado, below is the opening extract..

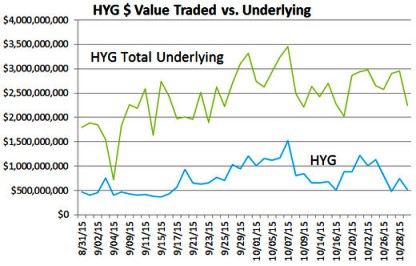

“Transcendent liquidity” is a somewhat silly-sounding phrase coined by the equally silly Matt Hougan, CEO of ETF.com, to discuss the odd situation in fixed-income ETFs—specifically, fixed-income ETFs tracking narrow corners of the market like high-yield bonds.

But it’s increasingly the focus of regulators and skeptical investors like Carl Icahn. Simply put: Flagship funds like the iShares iBoxx High Yield Corporate Bond ETF (HYG | B-68) trade like water, while their underlying holdings don’t. Is this a real problem, or a unicorn?

Defining Liquidity

The problem with even analyzing this question starts with definitions. When most people talk about ETF liquidity, they’re actually conflating two different things: tradability and fairness.

Tradability is actually a pretty simple concept: How well will the market let me get in or out of an ETF? And for narrow fixed-income ETFs (I’m limiting myself to corporates, in this analysis), most investors should be paying attention to the fairly obvious metrics, e.g., things like median daily dollar volume and time-weighted average spreads. By these metrics, a fund like HYG looks like the easiest thing to trade ever:

On a value basis, the average spread for HYG on a bad day of the past year is under 2 basis points. It’s consistently a penny wide on a handle around $80, with nearly $1 billion changing hands on most days. That puts it among the most liquid securities in the world. And that easy liquidity is precisely what has the SEC—and some investors—concerned.

Fairness

But that’s tradability, not fairness. Fairness is a unique concept to ETF trading. We don’t talk about whether the execution you got in Apple was “fair.” You might get a poor execution, or you might sell on a dip, but there’s no question that your properly settled trade in Apple is “fair.”

In an ETF, however, there is an inherent “fair” price—the net asset value of the ETF at the time you trade it—intraday NAV or iNAV. If the ETF only holds Apple and Microsoft, that fair price is easy to calculate, and is in fact disseminated every 15 seconds by the exchange.

But when the underlying securities are illiquid for some reason (hard to value, time-zone disconnects or just obscure), assessing the “fair” price becomes difficult, if not impossible.

If the securities in the ETF are all listed in Tokyo, then your execution at noon in New York will necessarily not be exactly the NAV of the ETF, because none of those holdings is currently trading.

Premiums & Discounts

In the case of something like corporate bonds, the issue isn’t one of time zone, it’s one of market structure. Corporate bonds are an over-the-counter, dealer-based market. That means the iNAV of a fund like HYG is based not on the last trade for each bond it holds (which could literally be days old), but on a pricing services estimate of how much each bond is worth. That leads to the appearance of premiums or discounts that swing to +/- 1%.

A pile on approach is impacting hedge fund emulator ETF products (e.g. $GURU, $ALFA), and leading to crowd control issues, according to a recent Bloomberg article re-distributed via TradersMagazine story with title:

Hedge Fund-Replicating ETFs Hurt by Crowded Trade Selloff

MarketsMuse curators carry the story here..

(Bloomberg) — Exchange-traded funds designed to mimic the strategies of hedge funds are mimicking their way into some serious losses of late.

Since the start of August, the Global X Guru Index ETF, (NYSE:GURU) which is tied to hedge funds’ top holdings using 13F filings, has slipped 10 percent, a casualty of popular trades that fell during this summer’s selloff and have so far failed to get back up. The Standard & Poor’s 500 Index has declined just 1.2 percent over the same period and recovered all of its 11 percent August correction.

“When something like this is opened up to retail investors, they tend to get the worst out of the deal,” said Bill Schultz, who oversees $1.2 billion as chief investment officer at McQueen, Ball & Associates Inc. in Bethlehem, Pennsylvania. “It’s not something that we find particularly attractive for our clients.”

The AlphaClone Alternative Alpha ETF, (NYSEarca:ALFA)which tracks the performance of U.S. equities to which hedge funds and institutional investors have disclosed “significant” exposure, has lost 19 percent since the start of August.

While lining up with the biggest speculators can make sense when markets rise, it has the potential to increase the pain on the way back down as everyone bails from losing bets at the same time. Trepidation has been in no short supply among money managers, with funds run by Stan Druckenmiller, Louis Bacon and David Tepper among those that disclosed declines in U.S.-listed equity holdings in the third quarter.

Quick selloffs are even more pronounced for stocks with “crowded” hedge fund positioning, according to Stan Altshuller, chief research officer at Novus Partners Inc. Novus measures crowdedness not only by the percentage ownership by hedge funds, but also by how many different firms are invested at the same time and how easy it would be for them to liquidate, he said.

Using this approach, a basket of the 20 most crowded stocks has trailed the S&P 500 by 21 percent from the start of June through Nov. 4, Novus data show. Companies such as Community Health Systems Inc., which decreased as much as 59 percent over the period, and Ally Financial Inc. are to blame for the underperformance.

“Nobody seems to grasp the severity of crowding as a risk,” Altshuller said by phone. “When the opportunity to exit is narrow, and there are a lot of funds in the stock, that creates the most dangerous type of situation. These stocks get absolutely crushed in times like these.”

Aligning one’s holdings with those of hedge funds hasn’t always been a losing proposition. A Goldman Sachs Group Inc. gauge that identifies the most popular bets across firms had annual returns exceeding the S&P 500 in each year from 2012 through 2014. That’s changed in 2015, with the Hedge Fund Very Important Positions Index trailing the benchmark index by 5 percentage points year-to-date, Goldman Sachs data show.

Institutional Investor Magazine has recently announced the world’s top 35 FinTech Bankers, and…

As astutely noted by Institutional Investor Magazine’s Senior Editor Jeffrey Kutler, “The origin of the term “fintech” is difficult to pinpoint; only very recently has it become an accepted label for one of the hottest segments of the technology market. The availability of high-performance computing and low-cost distribution channels is attracting a steady stream of entrepreneurs with ideas for improving, if not revolutionizing, financial products and processes — and investors are in hot pursuit.”

With that lead in, MarketsMuse curators are happy to excerpt II’s latest ranking report, this one profiling the top fintech bankers and financiers. We extend a special salute and shout out to merchant bank SenaHill Partners, led by securities industry veterans Neil DeSena and Justin Brownhill—whose boutique merchang banking firm is ranked within the top 20 of 35 firms profiled by Institutional Investor’s global survey.

Institutional Investor’s first Fintech Finance 35 ranking turns a spotlight on the financiers who are abetting this flowering of innovation. They include deal makers at various stages of the investment cycle and facilitators of the incubating, mentoring and capital-raising ecosystems that accelerate promising financial start-ups’ paths to commercialization.

According to one global tally, by consulting firm Accenture, fintech investment tripled in 2014, to $12.2 billion, its growth rate dwarfing the 63 percent for venture capital overall. Research firm CB Insights estimates that fintech’s share of total venture capital activity quadrupled between 2008 and 2014, to 12 percent.

That’s the big picture. Here we present perspectives on the boom through the lenses of some of its leading players. (To account for firms’ partnership structures, a total of 41 individuals are recognized.) Opinions and investment theses vary, as does the approach of a traditional venture fund manager compared with that of a corporate strategic investor. But all share a conviction that fintech is here to stay and an enthusiasm for the work, which neither begins nor ends when checks are issued. Venture capitalists typically meet with hundreds of prospects over the course of a year before making a relatively small handful of bets, and through board seats or other types of advisory relationships they provide ongoing guidance, often drawing from extensive industry experience.

The Fintech Finance 35 ranking was compiled by Institutional Investor editors and staff, with nominations and input from industry participants and experts. The evaluation criteria included individual achievements and leadership at the respective firms, influence in the community at large, and the size, reputation and impact of the respective funds and institutions in the financial technology industry — particularly in the current wave of fintech financing.

The Fintech Finance 35 was compiled under the direction of Senior Contributing Editor Jeffrey Kutler. Individual profiles were written by Kutler; Asia Bureau Chief Allen T. Cheng; Senior Writers Frances Denmark, Julie Segal and Aaron Timms; Research Staff Writer Jess Delaney; Senior Contributing Writer Katie Gilbert; Associate Editor Kaitlin Ugolik; and Editor Michael Peltz.

MarketsMuse Global Macro curators credited with metaphoric title “Dollars and Donuts”–a phrase many of those who trade on institutional desks should appreciate…Snippet below is courtesy of a.m. edition of institutional research unbundler SubstantiveResearch.com

Neil Azous from Rareview Macro writes that for all attention being devoted to the equity market at the moment, the biggest sensitivity in markets currently is the long USD trade, which is where a majority of the market risk now sits. Indeed, with 45 days left in the year, this trade could be the make or break for many investors in 2015, Azous adds. This is reflected in CFTC positioning and yesterday’s BAML fund manager survey, which shows a widespread sensitivity to a USD selloff. Azous outlines three hurdles that US dollar longs should be aware for the remainder of the week. Not surprisingly they involve either central bank meetings or disclosure of policy committee meeting minutes from the BoJ, Fed and ECB.

To read the entire commentary form Rareview Macro, click on the link below (subscription required, Free Trial available)

MarketsMuse curators have been navigating commentary across the media throughout the weekend in search for the various financial industry pundits and opinionators who might add some context to the terrorism that shook Paris on Friday night. No surprise, we noticed the below opening from hot-off-the-press a.m. commentary from global macro advisory Rareview Macro via their institutional newsletter “Sight Beyond Sight”..

Neil Azous, Rareview Macro

Israeli equities are showing the largest positive risk-adjusted return across regions and assets. Crude Oil is -3% off the overnight highs and now trading flat-to-negative. So what is behind that? One argument is that these asset markets are positively responding to the deal made over the weekend on how to end Syria’s civil war and the adopted timeline that will let opposition groups help draft a constitution and elect a new government by 2017.

A lot of professionals want to believe that the US equity market is also technically oversold. Combine that with some of the global solidarity sketched out above in response to the weekend events in France and the view is that there will be more stability rather than higher volatility today in risk assets.

If you believe that, we have land for sale in Fallujah, Iraq and it’s at half price today.

For the full analysis expressed by Rareview Macro’s Sight Beyond Sight,please click here

Marathon Asset Management CEO Bruce Richards Leads Crowdfund Campaign for “Veterans Education Challenge”

Hedge Fund Honcho Will Match $1mm Raised via Crowdfunding Platform CrowdRise

(RaiseMoney.com) For those Wall Street sharks and finance industry wonks who haven’t yet received the memo about crowdfunding, you might want to dial in to hedge fund industry icon Bruce Richards, Co-Founder and CEO of Marathon Asset Management, the $12.5 billion investment firm that specializes in global credit markets. Richards, whose pedigree includes 15 years in senior trading desk roles for top Wall Street banks before migrating to the world of hedge fund management in 1998, is not only at the helm of one of the investment industry’s most successful and most philanthropic fund managers, he’s just promised to personally match the first $1million raised on crowdfund site Crowdrise for “Veterans Education Challenge”; a campaign dedicated exclusively to funding college scholarships for US military veterans.

Bruce Richards, Marathon Asset Mgt

The fund raising campaign, announced this past week in conjunction with the celebration of Veterans Day 2015, seeks to raise at least $1mil within the next 12 months, according to the campaign information at crowdfund platform Crowdrise, one of the industry’s leading charitable donation portals co-founded in 2010 by film industry icon and social activist Edward Norton. The goal for the Veterans Education Challenge is to provide scholarship funding for any veterans at 4-year accredited starting the coming school year. This $1 million matching contribution will remain in place until November 11, 2016, next year’s Veterans Day.

In a special note sent to recipients of Richards’ email distribution list, one that typically provides Marathon clients with the firm’s widely-sought insight to global credit markets, Richards provided a starkly compelling investment thesis as to the importance of supporting advanced education for US military members and the need to insure their successful transition into private sector roles in ways the US Government often falls short in providing. In addition to pointing investment firm clients and friends to the Veterans Education Challenge Crowdrise page, Richards encouraged his followers to help advance awareness of the campaign’s FaceBook page and to enlist their following the Twitter account for VetEdChallenge via @VetEdChallenge.

One such recipient of Richards’ outreach included Dean Chamberlain, the Chief Executive of Mischler Financial Group, the securities industry’s oldest investment bank owned and operated by Service-Disabled Veterans and a firm widely-known for underwriting philanthropic causes that benefit military veterans and their families. Stated Chamberlain, “I’ve known Bruce for nearly twenty five years and I commend his philanthropic leadership. I wholeheartedly endorse and have already made my contribution to the VetEdChallenge crowdfund campaign and I will encourage others to follow suit.”

Richards, along with his wife Avis, an award-winning documentary film producer and director and the founder of Birds Nest Foundation, are considered to be one of New York’s top society couples. They are widely-credited by hedge fund peers for their philanthropic thought-leadership. Marathon Asset Management, whose two other leaders include co-founder Louis Hanover and Andrew Rabinowitz, Marathon’s COO is repeatedly lauded for the firm’s culture of supporting critical philanthropic missions that benefit health and welfare social causes.

MarketsMuse followers have been reminded more than a few times that conventional wisdom requires investors to keep their eyes on corporate bond spreads so as to have a clear lens when considering the outlook for equity prices on a medium-to-longer time frame. The relationship between high-yield debt,most-often measured by HYG (the high-yield bond exchanged-traded fund) and VIX–the latter of which is an often misunderstood metric, is a telling indicator for stock investors. And, those who are experts at reading the tea leaves are pointing to red flags on the horizon..

Courtesy of CNBC, Neil Azous of Rareview Macro and Andrew Burkly of Oppenheimer, two of the industry’s most sensible pundits discuss the cause and ramifications of the recent junk bond sell-off, pointing to high yield bond ETF $HYG as a meter benchmark to in the video below..

Unless you are Rip Van Winkle, you don’t need to be a MarketsMuse to know that the primary value proposition put forth by the ETF industry has always been: “Lower Fees Vs. Mutual Funds!” Yes, the secondary ‘advantage’ is “liquidity,” given that investors can move in and out of exchange-traded-funds throughout the trading day, whereas mutual funds are priced on an end-of day basis.

Well, Issuers of exchange-traded funds are now eating their own lunches, as competing Issuers are now pursuing a “race-to-zero” path when it comes to administration fees—adding a further crimp to the mutual fund industry’s marketing complex—which is being rocked by allegations from PIMCO’s former top honcho Bill Gross who has alleged in a recent lawsuit that PIMCO’s administrative fees are equal to the management fees the firm charges (but, that’s another story!)

Courtesy of today’s column by WSJ’s Daisy Maxey ETF Fees: “The Arms Race to Nothing”, the story at hand is worth two in the bush…here’s an excerpt:

Daisy Maxey, WSJ

BlackRock Inc. exchange-traded fund can now claim the title of the lowest-cost stock exchange-traded fund—but it probably won’t have that distinction to itself for long.

BlackRock, the largest global provider of ETFs, on Tuesday cut fees on seven of its iShares Core ETFs. That included trimming the annual expenses of the $2.7 billion iShares Core S&P Total U.S. Stock Market ETF to 0.03% of assets from 0.07%, bumping a pair of Charles Schwab Corp. ETFs from the lowest-cost spot.

Within hours, Schwab vowed to match the cut on its $4.9 billion Schwab U.S. Large-Cap ETF, which currently has expenses of 0.04%.

“Our intention has always been to be the price leader in the ETF space, and we’re going to maintain that,” said a spokesman for Schwab, who didn’t give an exact time frame for the company’s planned move.

Low fees have been one of the big attractions of ETFs and providers have competed fiercely to whittle down their charges by additional hundredths of a percentage point. The latest cuts by BlackRock are being viewed as a challenge to Vanguard Group, the No. 2 in ETF assets, as well as a sign of the success of BlackRock’s iShares Core ETF lineup, launched three years ago.

The giants of the ETF business are BlackRock, with $818 billion in U.S. ETF assets under management; Vanguard, at $479 billion; and State Street Global Advisors, the asset-management business of State Street Corp. , at $418 billion, according to Thomson Reuters Lipper. Schwab is a distant No. 7, with $38 billion in U.S. ETF assets, according to Thomson Reuters Lipper.

BlackRock’s iShares Core ETFs, which now number 20, are marketed as simple and low-cost portfolio building blocks.

The lineup has grown to $160 billion in assets as of Sept. 30, according to BlackRock.

Former Lehman Bros capo Richard Fuld likes acronyms, and somewhat out of character for the Big Dick many on Wall Street remember him to be, he also apparently likes the idea of inserting himself into a consortium that has created yet another new exchange platform–that eschews the notion of maker-taker for being ‘bad policy’ and leading to the subtitle of this story: “NSX Takes On IEX; No Rebates Allowed”

So, MarketsMuse curators ask our readers to pardon the misleading lead-in title; the latest entrant to the world of equities exchanges isn’t really new, in fact its legacy extends back 130 years. Yep, MarketsMuse curators from the fintech department came across this ‘Back to The Future’ story courtesy of coverage from WSJ’s Bradley Hope, our favorite “Clark Kent of Market Regulation and Trading Technology.”

One of the country’s oldest stock exchanges is planning a comeback next month.

The National Stock Exchange, originally founded as the Cincinnati Stock Exchange in 1885, has submitted a final rule filing with the Securities and Exchange Commission and could restart trading as early as December.

The revival of the 130-year-old exchange as NSX will bring the number of U.S. stock exchanges to 12 at a time when many critics of the market structure say there are too many trading venues. IEX Group Inc., an upstart that has positioned itself as a haven against predatory trading, also has applied to become an exchange, but that isn’t expected to be approved before 2016.

The new owners of NSX say they will introduce some novel features, starting with abolishing the prevalent “maker-taker” pricing system where firms that post orders on an exchange get a rebate of 20 to 30 cents per 100 shares traded and those that take the order are charged about the same amount.

NSX will only charge firms if they take a resting order and the cost will be just three cents per 100 shares, a cost of as much as 90% less than on other markets.

“We’ve heard a lot about issues with the market structure and agree with some of the criticisms,” said Mark Sulavka, chairman and CEO of National Stock Exchange Inc. “But we want to actually make changes, not just talk about them.”

Dick Fuld, Former Lehman Bros Chair/CEO

Mr. Sulavka is being advised by a range of exchange veterans and bankers including Dick Fuld–that’s right, the same guy who was CEO of Lehman Brothers Holdings Inc., who helped arrange the buyout of NSX by a new consortium.

Other advisors include Bill Karsh, the former CEO of Direct Edge and Kevin O’Hara, a former co-general counsel of the New York Stock Exchange. Louis Pastina, who oversaw NYSE’s trading floor until 2014, is chairman of NSX’s regulatory oversight committee.

Even if it “traded ahead”, those who missed it can find the full story from WSJ by clicking here

9 November (BrokerDealer.com)–Broker-Dealer Mischler Financial Group (“Mischler”) , the securities industry’s oldest minority investment bank and institutional brokerage owned and operated by Service-Disabled Veterans announced that in connection with the firm’s annual recognition of Veteran’s Day, Mischler has pledged a portion of the firm’s entire November 2015 profits to The Bob Woodruff Foundation (“BWF”), the national non-profit established by the award-winning ABC News journalist Bob Woodruff and his wife, Lee Woodruff. Mischler contributes more than 10% of the firm’s profits to disabled veteran initiatives throughout each year.

Mischler Financial’s pledge to Bob Woodruff Foundation coincides with the firm’s ongoing sponsorship of Veterans on Wall Street (VOWS), the financial industry’s leading advocacy dedicated to mentoring and career development of military veterans who transition to the financial services industry.

Dean Chamberlain, CEO Mischler Financial Group

In a statement by Mischler Financial Chief Executive Dean Chamberlain, a former US Army Captain and a U.S. Military Academy at West Point graduate, “Our continued commitment to Bob Woodruff Foundation, as well as our role at VOWS, is based on our legacy of re-directing firm profits to support what we believe are the most crucial, service-disabled veteran programs. Our giving back strategy targets four discrete objectives; direct financial support that can be truly impactful, career building and mentorship, advancing veteran-centric legislative initiatives, and working with major corporations to help guide their respective internal veteran mentoring and community outreach programs.”

Added Chamberlain, “The fact that our institutional trading desk clients make it a point to support our philanthropic mission serves as inspiration for all of our team members and underscores a shared alignment with causes that are critical to our nation’s veteran community; for that we are greatly appreciative.”

On the heels of an Oct 6 story at MarketsMuse about UK-based “Crowd2Fund.com”, now there’s another fintech entrant seeking to introduce secondary market trading of crowdfund deals. In a news release this week, Australia’s Equitise is joining with Syndex to create a new Alternative Trading System (ATS) to facilitate secondary market for crowdfunded securities.

In separate equity crowdfund industry news courtesy of industry portal RaiseMoney.com the US Securities & Exchange Commission passed new rules for equity crowdfunding deals, which is expected to create a title wave of new opportunities for the brokerdealer industry.

Oct. 27 (BusinessDesk) – Equitise, the only trans-Tasman equity crowd funder, will launch a secondary market allowing investors to trade in real time in Australia and New Zealand in shares of crowd-funded ventures, which have typically been more illiquid investments.

The Auckland and Sydney-based firm, in partnership with Syndex, will build an online exchange where investors can buy and sell shares in Equitise crowd funded companies after the initial offer has closed, using the online exchange during trading periods.

“We want the companies we crowd fund to have a safe, secure and transparent way of trading securities,” Equitise co-founder and New Zealand manager Will Mahon-Heap said in a statement. “It combines Equitise’s expertise in running successful crowd funding campaigns with Syndex’s online exchange to provide companies with all the tools and resources they need to govern and manage shareholder interests.

“It will also provide our companies with access to new investment communities to stimulate trade in secondary markets and help generate more interest in crowd funding opportunities.”

Auckland-based Syndex has applied to the Financial Markets Authority to become a licensed financial products market, even though the Financial Markets Conduct Act does not currently require it to do so. Under the FMA’s equity crowd funding licensing regime, a platform such as Equitise wanting to give shareholders more liquidity in their investment would first need to get sign-off from the regulator to build a secondary market, where investors could trade equity up to an annual cap of 100 trades. Using Syndex means Equitise does not need to go through that process.

Companies are able to raise a maximum of $2 million from the ‘crowd’ in exchange for offering equity through crowd funding platforms.

Mike Jenkins, MD of Syndex

Mike Jenkins, MD of Syndex, called the partnership a fantastic endorsement of Syndex’s ability to provide a common, go-to place for investors that have an interest in investing and trading in proportionally-owned assets. “We’re excited to be working with Equitise to launch in the private company equity market here in New Zealand and across the ditch in Australia.”

“We’re creating a trusted investment environment that promotes confidence and enables investors to tap into the substantial global equity crowdfunding market. That will not only create value for individuals and companies, but also stimulate growth and create wealth for the wider New Zealand economy.”

The financial markets regulator has said the legislation isn’t prescriptive when it comes to what any ancillary market for equity crowd funded companies might look like.

“Our overall concern is to ensure that the services run, the original offer and the secondary market, in a fair and transparent way. But in terms of how a secondary market might be run, we’re agnostic in how a crowd funder might do that,” Garth Stanish, director of markets oversight at the FMA, told BusinessDesk in September. “We haven’t been prescriptive around what we look for. We will expect to engage with each of the crowd funders as they come to us and there’s a range of options in how a crowd funding service could choose to structure a secondary market.”

Since the first licences were awarded in July last year, New Zealand now has seven equity crowd funding platforms and 37 offers have either been run or are underway, of which 24 successfully raised a total $13.3 million.

Competition to provide investors the ability to trade in their crowd funded equity is heating up.

Unlisted, the alternative share trading platform which also runs equity crowd funding platform CrowdCube, plans to offer crowd funded companies cheaper fees to list on its market. Snowball Effect, which is New Zealand’s largest platform to date in terms of capital raising, also has a secondary market offer waiting, which would see it facilitate trading periods for companies on their own websites, rather than through a multi-issuer market.

In August, Commerce Minister Paul Goldsmith granted an exemption from licensing requirements for Unlisted, which means the market can continue as an unlicensed platform, but its website must make its unlicensed status clear and investors will need to sign a declaration acknowledging the risks involved.

In a July 20 brief to the minister, obtained under the Official Information Act, the Ministry of Business, Innovation and Employment says an exemption will set a precedent for future applications “potentially including crowd funding platforms seeking to extend their licences to provide secondary markets”. In an Aug. 7 note to the minister, the FMA said while there was opposition to Unlisted’s exemption from some industry operators, whose names were redacted, others were in favour “albeit they did not consider that Unlisted would fill the secondary market gap for crowd funded companies.”

The Equitise-Syndex secondary market offer is different from Unlisted, with Syndex offering a peer-to-peer trading model, whereas Unlisted operates via brokers. The Syndex platform also has built its exchange using the cloud, a spokesman for Equitise said.

The NYSE, a division of Intercontinental Exchange (ICE) has encountered a slippery slope in the exchange’s effort to secure a bigger role in the ETF marketplace through a scheme that would expedite the creation of so-called actively-traded ETFs, which some MarketsMuse followers have dubbed ‘exchange-traded funds on testosterone.’

WSJ-The New York Stock Exchange this month withdrew a proposal to the Securities and Exchange Commission that would have expedited the regulatory approval of some exchange-traded funds, a setback for the fast-expanding ETF industry.

What the Intercontinental Exchange Inc. unit sought is known as a generic listing standard, which would have cut months off the process to list actively managed ETFs. Listing currently requires a fund-by-fund evaluation by the SEC that can take several months. The SEC reported the withdrawal on Oct. 19.

Generic listing standards for many index-based products, which seek to mimic the performance of a particular index, have slashed the time and cost of getting an exchange-traded fund to market, helping fuel a record number of new issuers this year.

The setback for efforts to secure similar standards for actively managed products highlights the limits facing the industry after years of rapid and broad growth.

The SEC declined to comment on the withdrawal. A person familiar with the process said there were concerns at the SEC about the open-ended use of derivatives that could occur if the rule were approved. A narrower proposal could limit the types of new funds or tools they use should the SEC eventually approve the listing standards.

For its part, NYSE still sees value in a faster approval process for these funds, an exchange spokeswoman said.

A person familiar with the matter said NYSE would tweak and refile the proposal.

“I think it’s the SEC being extra cautious,” said Todd Rosenbluth, head of ETF research at S&P Capital IQ. “I think they want to fully understand the risks that investors take on with these products.”

Exchange-traded funds hold baskets of stocks, bonds or other assets and trade on an exchange like a stock. Most are passive, with holdings dictated by the rules and weightings of the index they are designed to track. Actively managed products, in which a fund manager can change the holdings, account for only about 130 of the 1,787 exchange-traded products in the U.S., according to ETFGI, a London-based consulting firm. They have about $21.6 billion in assets, a fraction of the some $1.98 trillion in all exchange-traded products in the U.S.

But actively managed funds represent a frontier for ETFs, and exchanges are eager to speed up the process of listing them, particularly as the competition for listings heats up.

Sayonara City As Japan Getting Crash Course in Leveraged Returns With Nikkei ETF

MarketsMuse ETF update courtesy of Bloomberg LP Oct 15–Nomura Asset Management Co. said it would suspend on Friday the creation of new shares in a large leveraged exchange-traded fund, as well as two others, citing liquidity concerns.

The move applies to the Next Funds Nikkei 225 Leveraged Index Exchange Traded Fund (BBRG Ticker: 1570 JP Equity <GO>), which has about ¥734 billion ($6.2 billion) in assets. The fund’s shares are up about 8.7% this month. Nomura said shares will continue to trade.

“The temporary suspension has been determined, considering the current situations of fund management including the liquidity of the underlying Nikkei 225 futures and the total assets under management of three ETFs,” Nomura posted on its website. The firm will continue to receive redemptions, it said.

A Nomura representative wasn’t available to comment.

The decision highlights an increasingly warned-about side effect of exchange-traded products’ growing popularity: a mismatch between the liquidity of some funds and their holdings.

The Nomura decision also highlights concerns about leveraged products, which provide investors with outsize exposure to certain asset classes, employing tactics such as borrowed money and derivatives. The $6.2 billion fund provides investors with two times the exposure to the Nikkei 225.

The products have been popular in the U.S., but the size of Nomura’s Next Funds Nikkei 225 Leveraged Index ETF is larger than any such leveraged exchange-traded product in the U.S., said Dave Nadig, director of ETFs at financial-data provider FactSet. There are close to 1,800 exchange-traded products listed in the U.S., and about 230 of them are leveraged, he said.

Regarding how leveraged funds operate, Mr. Nadig said: “The math makes people’s heads hurt.”

It’s not the first time an exchange-traded product has run into obstacles because of its own popularity. Credit Suisse Group AG had to suspend the creation of new stock in the VelocityShares Daily 2x VIX Short-Term ETN in February 2012, after demand for the security hit a limit set when the product was created in 2010. Barclays Plc also halted issuance in its iPath Dow Jones-UBS Natural Gas Total Return Sub-Index ETN in August 2009.

Guest Contributor and fixed income markets muse Ron Quigley, Managing Director of Fixed Income Syndicate for diversity firm Mischler Financial Group offers a Glass of Insight to the likely timing of the ABBIB acquisition of SABLN (AnheuserBusch proposed takeover of brewer SAB Miller). Below commentary is an extract from 15 October edition of Quigley’s Corner, the nom de guerre of daily debt market commentary distributed to Fortune 100 corporate treasurers, leading investment management firms, and the top fixed income deal bookrunners on Wall Street.

Timing of ABIBB for SABLN Deal

Ron Quigley, Mgn.Dir. Mischler Financial Group

There’s been a lot of conjecturing as to the timing of the Anheuser-Busch InBev NV (A2/A) for SAB Miller plc (A3/A-) deal. That should be expected. After all, since SAB Miller accepted ABIBB’s s $106b takeover price on Tuesday, the buyer announced it will issue a corporate record $55b in debt to finance the takeover. I have subsequently been asked by many what my thoughts on timing are so why not share them with you as well?

There is a six week window before Thanksgiving after which things begin to slow down although I think this year, the first two weeks in December will be more robust than in prior years. Rates will be lower-for-much-longer and as we approach year end issuer’s will jump in to secure great financing before the busy start to 2016. Now, regulatory hurdles could certainly slow down the $55b in ABIBB issuance until next year. Recall that Carlsberg faced one year of regulatory harangues before it completed its takeover. However, assuming $1.25 trillion in total 2016 U.S. Corporate issuance, or more, the transaction represents 4.4% of that volume! Heck, we all find it hard to earn 4.4% interest on our own money!……Just to put 4.4% into the proper perspective. In addition, can the current marketplace absorb $55b in issuance? Today for example, many market participants were shocked at the relative absence of any IG primary calendar. Today’s session only hosted three issuers at a time when just yesterday we came off of the first back-to-back double digit billion dollar days for IG Corporate new issuance in five weeks dating back to September 8th thru the 10th! As one market professional quipped to me this morning, “hey it’s free money for them (ABIBB) so they can do this anytime!” No one can answer to the speed of regulatory hurdles but we all know when it comes to regulatory anything it means much more time. In this case the takeover has to meet muster with global regulators. For that reason alone we’ll see the deal print sometime next year.

The overall markets are also still very fidgety in here, although IG Corporate new issuance seemed to be moving in the right direction judging from the past two days and today’s session was especially impressive, albeit there were only three issues. There are concerns with IPOs not getting off the ground. For that, I point directly to yesterday’s pulled IPO for Albertsons Cos. In addition, First Data Corp’s lower than desired IPO priced at $16 vs. the $18 to $20 per share it sought and Neiman Marcus’s decision to wait on its IPO. First Data’s $2.6b IPO was the largest of 2015 and nearly twice that of runner-up Tallgrass Energy’s $1.4b IPO last May. Lest we forget that yesterday Wal-Mart shocked the investment community by forecasting a drop in 2016 earnings. Shares were pummeled down 10% and Q3 corporate earnings, for the most part, have missed with downward revised forward forecasts.

Dell Inc. (Ba3/BB+) also announced an up to $67b cash and stock deal to acquire EMC Corp. (A1/A). Dell is heard to be planning a total of $45bn in debt to consummate the deal. Net, net, not only ABIBB but Dell also stands to make billions from these deals so even “if” regulatory approval is unbelievably, almost unreasonably expeditious and the green light is given, both will leave big NICs on the table to get their deals done. As for the banks and the respective fees they stand to garner before year end, should timing be sooner rather than later on both transactions, well………..it’s a no brainer for them folks. The combined ABIBB for SABLN and Dell for EMC deals represent 8% of an entire year’s worth of IG Corporate issuance! Digest that for a moment….Did you hear that?.CHA-CHING! How badly would investment banks love to have those profits on their 2015 books?

MarketsMuse Strike Price curators are always looking for smart perspectives on how to bring more asset managers and institutional investors to better understand and embrace the use of options in a responsible manner. According to Todd Hawthorne, lead portfolio manager of Boston Partners, volatility [which some immediately and sometimes, misguidedly associate with the CBOE VIX Index], has created a new asset class for institutional and retail investors, and like all other asset classes, there are opportunities to harvest returns. In this case, the tools to implement volatility strategies are found via the use of options contracts.

Todd Hawthorne, Boston Partners

In a recent submission to Pensions & Investments, Hawthorne writes, “These volatility strategies, when viewed as their own discrete asset class, are designed with the goal of delivering returns that are in line with historical assumptions for equities while maintaining a far narrower range of performance (i.e., a substantially higher Sharpe ratio) and downside protection that can limit losses. Moreover, in a market in which yield has become difficult to find, the construct of equity buy/writes, coupled with bottom-up fundamental analysis, can create a synthetic yield instrument that delivers uncorrelated returns and manages to capitalize on volatility rather than being subjected to it.”

Adds Hawthorne, “Traditionally, when retail investors discuss “low volatility” strategies, they are referring to an approach that combines diversification with systematic and regular rebalancing. These more traditional approaches — be it Shannon’s Demon, the Kelly Criterion, or other variations — are more about circumventing volatility than actually capitalizing on it with true downside protection and improved return profiles…

However, other strategies that combine both equities and equity call options — or buy/write securities — can more effectively “harvest” returns out of swings in sentiment, while providing more predictable, and often better, performance even as volatility ramps up. The concept of creating synthetic yield isn’t necessarily new, as portfolio managers will often invest in buy/writes on a basket of stocks tied to an index as a way to generate returns that are in line with the market over time, but at slightly reduced volatility and with the added benefit of options income..”

While 99% of market pundits have been busy for the past months laying odds and making bets as to precisely when and how much the Fed will raise interest rates, a small universe of Fed Watchers have picked up on a surprising nuance that few seasoned market experts have even calculated into their outlooks. Its not about Janet Yellen’s body language, its more about the water in San Francisco and what the real Fed thought-leaders are signalling. Tony Bennett might have to update his iconic song..we’ll let the marketplace decide that one!

MarketsMuse Global Macro curators offer a hint into what those having Sight Beyond Sight are now modeling into their own calculations. As proffered via a special CNBC appearance by Neil Azous, the founder of global macro think tank Rareview Macro, LLC, the “lower for longer” theme could prove to be an even lower interest rate regime and lead to prospects for yet another QE, all driven by the clouds on the horizon that some believe are spelling out “global recession..” Listen carefully to the following thesis….and in tribute to Tony Bennett, scroll down and sit back to the second video clip on this post