Jane Street Capital, the quant-centric proprietary trading firm best known for its dominant role in the ETF marketplace–including its role as a liquidity provider for stocks and options as well as exchange-traded funds to buy-side accounts– has a new arrow in its quiver; making markets in corporate bonds. The firm disclosed that it is lifted its anonymous veil and is now a ‘disclosed dealer’ on electronic bond trading platform MarketAxess (NASDAQ: MKTX).

Shall we guess whether the 6-pack banks and their first cousins–the industry’s legacy source of liquidity to buy-side managers navigating the corporate bond market landscape are (i) happy to have a new competitor, (ii) happy not to have to make markets and tie up balance sheets with inventory of hard-to-move corporate bonds or (iii) f–king pissed that tech-focused prop trading firms are now invading a secondary market product area that banks have viewed as their exclusive territory since time began?

Shall we guess whether the 6-pack banks and their first cousins–the industry’s legacy source of liquidity to buy-side managers navigating the corporate bond market landscape are (i) happy to have a new competitor, (ii) happy not to have to make markets and tie up balance sheets with inventory of hard-to-move corporate bonds or (iii) f–king pissed that tech-focused prop trading firms are now invading a secondary market product area that banks have viewed as their exclusive territory since time began?

As noted by WSJ reporter, Matt Wirz, investment banks and brokerages are the main go-betweens for money managers looking to buy and sell corporate bonds, about $25 billion of which trade daily in the U.S. Now, Jane Street Capital LLC, has begun offering the same service to investment firms on electronic trading platform MarketAxess and has recruited about 60 clients, people familiar with the matter said.

The move puts Jane Street in direct competition with traditional dealers like Goldman Sachs Group Inc. and JPMorgan Chase & Co. It also shows how bond markets are being transformed by electronic and algorithmic trading, innovations that swept stock and currency markets more than a decade ago.

Jane Street’s headquarters are a five-minute walk from Wall Street, but in some ways the firm is more akin to a Silicon Valley startup than an investment bank. “They have a different approach—there’s not a lot of sales and a lot of technology,” says Mike Nappi, a bond trader for mutual-fund manager Eaton Vance Corp. who has bought and sold bonds through Jane Street. “That’s different from a traditional bank where they have a lot of sales and the technology is more like Microsoft Excel.”

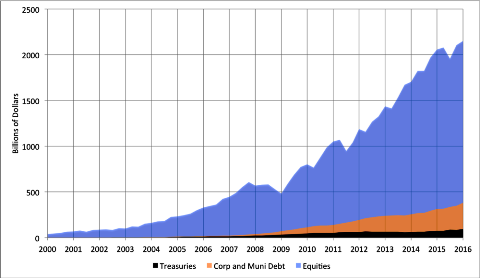

By joining those ranks, Jane Street aims to get recognition from asset managers for the balance sheet it uses to buy and sell with them, ultimately boosting the amount they trade with the firm, said Matt Berger, the firm’s head of fixed income and commodities trading. Jane Street trades about $550 million worth of corporate bonds in the U.S. every day, he said. This amounts to about 2% of the overall market, five times more than the firm traded two years ago.

That expansion would have been impossible without the recent spread of electronic bond trading.

Technology-driven trading firms like Jane Street and Virtu Financial LLC emerged after stock exchanges electronified in the 1990s, connecting buyers and sellers through computers and reducing trading times to fractions of a second. The firms’ computer scientists built programs to cull market data and identify profitable trades that humans missed. Now, quantitative trading firms dominate the stock market.

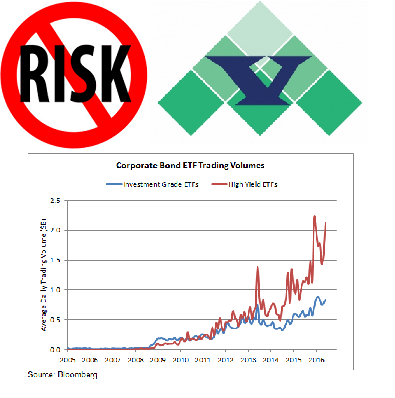

Electronic trading has been slower to catch on in debt markets because bonds typically trade over-the-counter rather than on centralized exchanges. That has begun to change over the past five years as banks and money managers turn to electronic trading and data analysis to trim costs and to connect to more trading partners. Electronic trading platforms like MarketAxess have given Jane Street and other quantitative investors venues to apply the technology they used in other markets.

MarketAxess accounted for about 18% of all U.S. investment-grade bond trading last year, up from 12% in 2014, according to data from the company.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

Jane Street, founded by four partners including Michael Jenkins and Robert Granieri, now has about 50 bond salespeople and traders. Recruiting materials tout chess facilities, office gyms, math puzzle contests.

The firm trades less debt overall than most banks, which still employ hundreds of human sales and trading staff. But when it comes to its inventory of corporate bonds, “we are on par with the banks,” Mr. Berger said.

Jane Street hold bonds on its balance sheet for days or weeks to facilitate so-called portfolio trades of bundles of bonds often tied to ETFs. The portfolio deals normally range from $50 million to $750 million but can go as high as $2 billion, a person familiar with its trades said.

Read the full WSJ story here