Stocks Benefit From Surge Pricing

A review of February equities market performance

The Drivers : AI + Economic Improvement + Corporate & Consumer Confidence

What’s Next?

Looking Back to Look Forward : Month End Equities Market Comment 2024 Episode 3

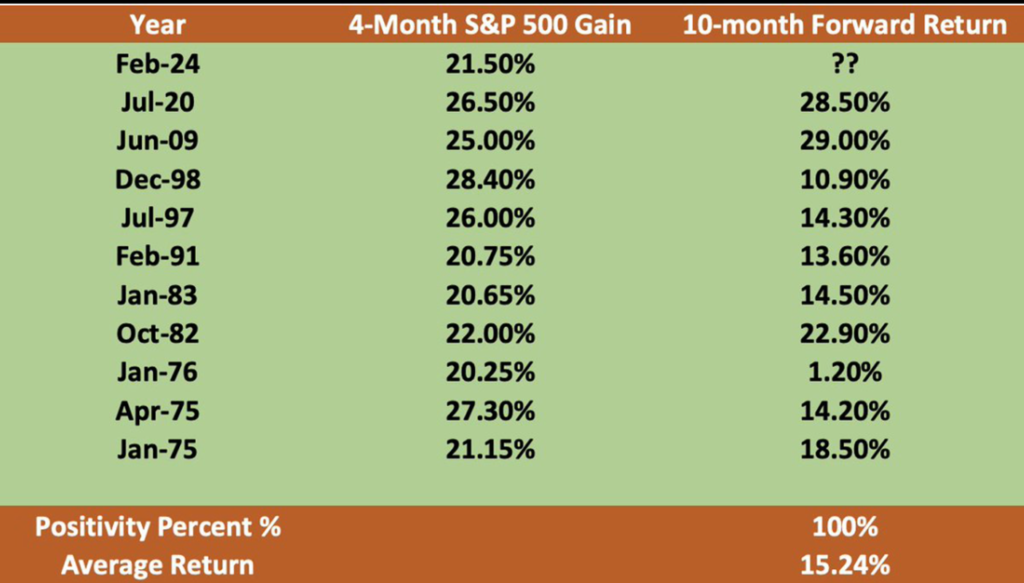

This being the 3rd edition of the year for our month-end equities market commentary, it’s worth noting that February, historically the second worst performing month of the year for stocks (Sept winning the top spot), Feb turned out just fine, and proved the technicians, chartists, and ‘seasonality pundits’ wrong, once again.

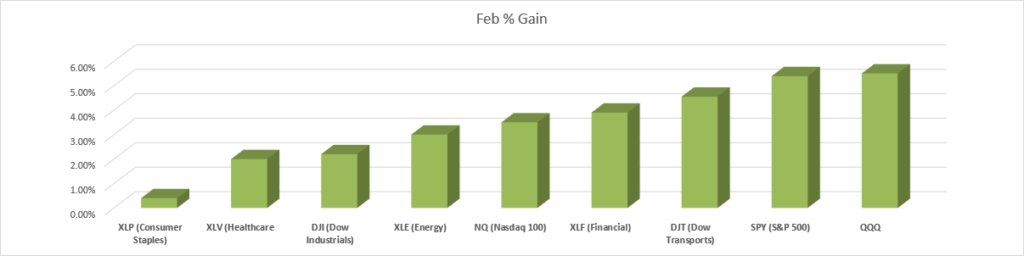

A look at the month-end stock price performance data finds nearly every sector with noticeable gains, despite the month’s uptick in interest rates across the yield curve. (More on that below).

A round of applause to the assortment of Fortune 500 CFOs, corporate treasurers, and investor relations professionals who have played important roles in delivering financial performance numbers that have inspired your investors with solid results.

Yes, a handful of best-known “AI darlings” (aka Artificial Intelligence) has led the most recent 4 consecutive months of price gains of 20% in the S&P 500 and Nasdaq 100 (QQQ). And yes, the PE Ratio for the S&P 500 has also expanded noticeably, which is often a worrisome sign for pension fund managers who are looking to allocate cash.

“It’s All About AI, Stupid!” (to paraphrase James Carvell) The AI revolution is still in the infancy stages and some less sanguine say that share prices in companies most rooted in providing AI and Generative AI picks and shovels “have gotten in front of themselves.” On the flip side, 92% of Fortune 500 CEOs polled by PwC say that “Gen AI is a top investment priority”, and 63% say that Gen AI tools are expected to deliver material improvements in productivity and efficiency, and ultimately, expansion in profitability. Last week, Travelers Corp (NYSE:TRV) Chairman & CEO Alan Schnitzer told the WSJ that a significant amount of the insurance giant’s $1.5bil technology investments in 2023 went to large language Gen AI models that “have already enabled us to process hundreds of thousands of broker submissions within a matter of minutes, as opposed to hours or days. Along the way, underwriting expense ratios have improved materially. The workflow process improvements are staggering, and the math in terms of ROI is pretty simple to calculate.” To wit, the insurance company’s stock price is up 14% YTD.

And, No, It’s Not a Bubble, The Markets Have Simply “Re-Priced”. Even mega-billionaire investor Ray Dalio, the founder, and former Chairman & CEO of Bridgewater Associates, the world’s largest hedge fund, and someone who is known for being skeptical in the face of skyrocketing asset prices, said as recently as March 1, “The Mag 7 sector is a bit frothy, yet the U.S. equities market is not really that bubbly (yet).” He details his views on LinkedIn.

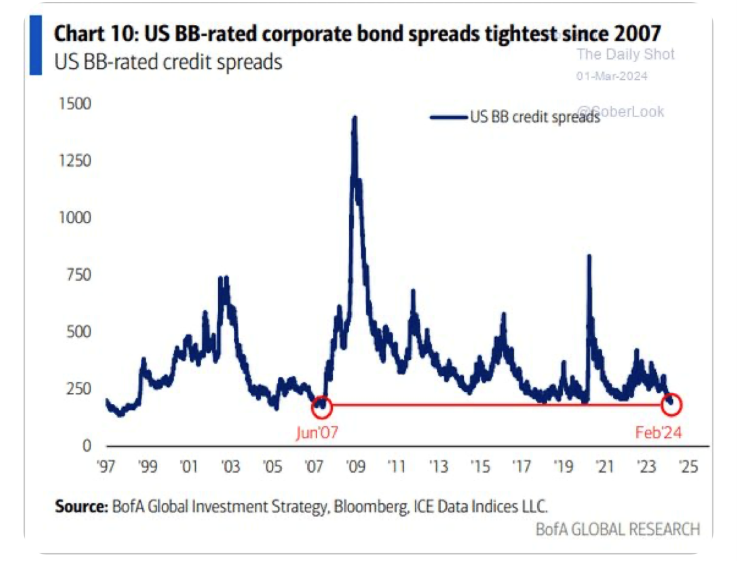

Wait, It’s (also) About the Economy! By many measures, whether it be GDP, employment, manufacturing, consumer sentiment and consumer spending, the US economy has proven very resilient. As noticed by rates traders, February’s increase in interest rates across the curve (40bps on the 2’s, 37bps on the 5’s, and 29bps on the 10’s), equity prices have been impervious to interest rates at this point.” Underscoring that point, the spread between IG and HY debt has narrowed to historic levels, and February saw the largest number of IG corporate debt issuance for any February in history. $155bil was floated, including several large transactions from Abbvie and 3M that were dedicated to funding M&A transactions, a part of the market that is re-percolating, irrespective of the uptick in borrowing costs.

Convertible Debt Issuance v.4.0 The Drexel Burnham Award For Great Placement Goes to SMCI. For those not old enough to know the name Drexel Burnham, in the 1980’s, that investment bank pioneered the transformation of modern debt financing and enabled many borrowers to bolster their balance sheets. Convertible bonds, which were first created to finance railroads in the mid 19th century, and also one of the arrows in the Drexel quiver, have since been a mainstay for a cross-section of companies during the past few years.

As most readers of this note are aware, “converts” enable lower-rated corporate issuers to borrow at rates significantly lower than IG issuers can by offering buyers an equity kicker with an exercise option that can be 25% to +50% or higher than the prevailing stock price. In February, Super Micro Computer (NASDAQ:$SMCI), whose fortunes are greatly tied to that of Nvidia, floated a 5 year, $1.5b senior unsecured note with a ZERO interest coupon, but enables investors to convert into shares at a 37.5% premium. Said another way, based on a stock price of $900ish at the time the deal was struck ten days ago (up from a price of $281 since Jan 2!), investors can convert their notes into stock for a price $1341 per share. This strategy can ostensibly work for a bevy of Issuers across multiple sectors, including those that are pivoting to AI empowerment.

That said, $SMCI price was added to the S&P 500 index after the close of regular day trading Friday, Mar 1, and the stock rocketed from $902 to an intra-day high of $1155 before noon Monday, Mar 4 (a 25% increase in a matter of hours, a near 50% increase in ten days, a 100% increase in three weeks, and a 175% increase since Jan 2).

Geopolitical Risks: Are there any Canaries in the Coal Mine? Russia, China, the Middle-East, North Korea, threats of US Government shut-down (on top of ballooning government debt), not to forget Cyber Attacks, or the most contentious Presidential election season in recent history, all present risks of one kind or another. Yet, the equities markets have continued to discount these tail risk topics. Likely because there hasn’t been a debilitating Black Swan since the global pandemic. “The clue is in the skew”; meaning that call option prices on major indices and large-cap stocks remain slanted to favor continued upside in equities prices as the ‘re-pricing’ regime remains intact.

What’s in store for the months ahead? For those administering share repurchase initiatives, which is expected to account for up to $1trillion of stock purchases in 2024, or those investors who have a traditional 60-40 (or perhaps 70-30) allocation to US equities, there is an assortment of historical data that suggests US equity indices will end the year appreciably higher than where they started 2024.