Below is excerpt only from today’s edition of macro-strategy commentary courtesy of Rareview Macro LLC publication “Sight Beyond Sight”

Neil Azous, Rareview Macro LLC

Firstly, the Stock Exchange of Thailand SET Index (symbol: SET) is showing the largest negative and the Dollar-Rupiah (USD/IDR) is showing the largest positive risk-adjusted returns across regions and assets.

Of note, Thai stocks fell almost 10% at one point last night and the Indonesian Rupiah weakened by 2% to its lowest level relative to the US Dollar in 16 years. The head of the Thai bourse said no measures were needed to shore up stocks and investors shouldn’t panic and the Indonesia central bank reiterated their view that they will always be in market to stabilize the IDR currency.

Why do we start by highlighting Thai and Indonesian risk assets?

Because South East Asia is the clearest example we have seen of foreign investors pulling out of emerging markets and a prime example of what happens to stocks and currencies when there is a lack of liquidity. more

Below excerpt from Dec 10 edition of global macro strategy newsletter “Sight Beyond Sight” includes insight for those tracking events in Asia and China-related ETFs. When scrolling to the bottom of this post, MarketsMuse readers will appreciate why we regularly cite the Sight Beyond Sight newsletter—the conclusion of this post displays the out-performance of SBS publisher Rareview Macro LLC’s model portfolio.

“…Using the ETF’s as a proxy for the spot currencies, the pressure point in the Currency Shares Japanese Yen Trust (symbol: FXY) is closer to 83.15 (vs. last price 81.85) and the Euro Currency Trust (symbol: FXE) is closer to ~122.50 (vs. last price 122.00).

There are three major points we would like to make after the overnight price action in China.

The first is liquidity related and what actually drives that stock market. The second is inflation related and looks at what, at least partially, drives the rest of the world. The third is a rebuttal to the “bomb throwers” who continue to suggest that China has entered a phase of deliberately debasing its currency.

At no point during the recent stock market rally has any dogmatic bear on China been willing to concede that the stock market (i.e. liquidity) and the profit cycle (i.e. deflation) during cyclical episodes, such as the one we are witnessing right now, can have a meaningful divergence.

But they should note that the last time the SHCOMP outperformed the H share index due to an A share rally was back in 2006 and came at the start of rally of more than 200% for both indices and from a PE level that was more than two times the current levels. (Hat Tip: Aviate)

Additionally, with Macau struggling, real estate still contracting on aggregate, and Gold a weak trading tool, the stock market is the “vogue thing to do” at the moment. Fashion is important in China, just like anywhere else. more

Below excerpt from a.m. edition of Sight Beyond Sight, is courtesy of global macro think tank, Rareview Macro LLC

Neil Azous, Rareview Macro LLC

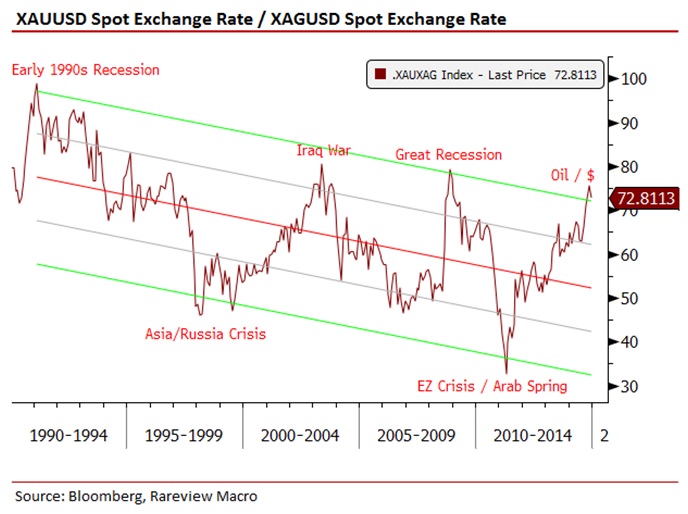

New Strategy – Short Gold vs. Long Silver

This morning we sold 3000 GLD 12/20/14 P112 at .63 to close.

We rotated our short Gold bias using put options into a short Gold versus long Silver spread using futures.

The updates were sent in real-time via Twitter.

Below are two illustrations: A “monthly” chart of long Gold versus Silver and a matrix containing our trade construction details.

Note that this is not a short-term “tactical” trade but rather an intermediate term “strategic” trade. As such, it will be managed with greater latitude in terms of risk.

Similar to the 200-day Moving Average (200-DMAVG), we find long-term Linear Regression Channels can be a strong technical indicator.

For those not familiar with Linear Regression Lines, it is a line that best fits all the data points of interest and consists of three parts: more

Below extract courtesy of a.m. edition of “Sight Beyond Sight”, the global macro trading commentary published by Stamford, CT-based macro strategy think tank Rareview Macro LLC.

“…For most of the second half of the year we have seen a surging dollar, and a falling euro. Nothing seems to be coming that will disrupt that.

Now a lot of US investors have asked why the WisdomTree Europe Hedged Equity ETF (symbol: HEDJ) performance has been sub-optimal. Specifically, why isn’t this “strong dollar/weak euro” play not playing out much like last year’s Japan trade (strong dollar/ weak yen) as we saw with WisdomTree Japan Hedged Equity (DXJ)?

As a reminder, DXJ is a portfolio of Japanese stocks with a currency hedge overlay (i.e. 100% of assets is hedged). So HEDJ is the European version of DXJ. The underperformance therefore is simply stock-related.

For example, HEDJ is a basket of European stocks (i.e. 100% of assets is FX hedged). The underlying basket is a Wisdometree dividend weighted basket. It does not quite have the same weightings as the iShares MSCI EMU ETF (symbol: EZU) which is market cap weighted & large cap equivalent or the iShares Europe ETF (IEV) or any other standard index, but it does have a very high correlation.

If you compare HEDJ vs. EZU (i.e. use Bloomberg COMP function, HEDJ in line one and EZU in line 2 and then change the currency next to EZU to EUR instead of USD) you will see performance come back in line with HEDJ as it displays the effect of the FX hedge.

So HEDJ is working exactly the way it should given how it is constructed and using HEDJ to get long European stocks and a weaker EUR is correct instrument for that view.

So the question becomes, how do you gain using HEDJ? more

Nov 17 2014 by Neil Azous Managing Member of Rareview Macro LLC

Most of us hand over dollar bills every day without ever really looking at them very closely. They are too familiar. But if you pause to look closely at the one dollar bill, you will see, right below the one-eyed pyramid, the Latin phrase “Novus Ordo Seclorum”.

The literal English translation of that is “a new order of the ages.” Taken from a book by the Roman poet Virgil, it first appeared on the Seal of the United States, and made its way onto the currency in 1835, where it has stayed ever since. Virgil was not a man to use words carelessly, so when he wrote it, he must have intended to emphasize “new” and, therefore, put it first in the sentence and in front of “ordo.”

A few readers might find that a slightly esoteric digression into Roman and monetary history, of little relevance to the markets today. In fact, they would be wrong. We started with that overlooked phrase because, over the second half of 2014, the professional investment community has come to believe that the US Dollar has indeed established a “new order” and the trend is now here for “the ages”. Continue reading →

A MarketsMuse special update, courtesy of compiling various columns from Bloomberg, ETF.com, Fortune and a special treat: this piece was sponsored by Mr. Chow’s! (see below)

After much fanfare, the “Shanghai-Hong Kong Stock Connect” is officially connected and ostensibly, this will be the link between brokers, dealers, ETF Issuers and global investors seeking access to a menu of mainland China stocks and bonds, whose market value is more than $4.2tril (if anyone knows another acronym for ‘Trillion”, please email us or simply comment below!). Even if trade volumes during the first 2 days appeared soggy (which some attribute to aversion to MSG, not China stocks or ETFs), this is a story that, according to many experts, is a watershed moment.

Noted Neil Azous, principal of global macro strategy think tank, Rareview Macro LLC, “This is a transformational event. Though the first day ‘scorecard’ indicates that retail/local investor support in Shanghai has proven successful out of the gate, institutional interest is still nascent, as evidenced by the big drop in Hang Seng share prices yesterday.” Added Azous, “Because the liberalization of markets is 1 of 4 key anchors to China’s long-term game plan, it is easy to expect that the opening of China markets to foreign investors might be incremental, but also integral to the evolution of the global financial marketplace.”

Below please find a collection of excerpts and ETF mentions that MarketsMuse has ‘cherry-picked’ from news outlets: Continue reading →

MarketsMuse coverage courtesy of out takes from a.m. edition of commentary produced by global macro trading guru Neil Azous, principal of macro-strategy think tank Rareview Macro LLC.. Editors Note: Aside from the prescience of “Sight Beyond Sight” outlooks throughout the past year (including select/specific and since successful trade ideas i.e. FX, Commodities (e.g. gold) and equities, Rareview’s process is uniquely aligned with the fundamental thesis embraced by the very smartest investors re macroeconomic investing: “mitigate exposure to risk, capture alpha in a conservative way, and never stay married to a position, particularly when the herd of wannabees comes to the party just when it seems like the main course has been consumed and coffee and desert are just starting to be served.

Risk in Very Near-Term is a Euro Short Covering Rally…Closed Core Long US Dollar Positions

A Lot of Importance Being Assigned to this Weeks US Inflation Data

Federal Reserve Following Bank of England a Clear Talking Point

Model Portfolio Update – November 14, 2014 COB: +0.27% WTD, +0.70% MTD,+17.57 % YTD

A Euro exchange rate short covering rally is the greatest risk going into the end of the week. The speed and degree of that is yet to be determined but our expectation is the Euro-Dollar (EUR/USD) will trade above 1.27 and if the US CPI on Thursday disappoints many investors will find themselves in a very difficult position.

After getting long on the US Dollar before the consensus on July 3rd we have reduced 100% our long exposure this morning. The following updates were sent in real-time via Twitter:

Sold 1180 DXZ4 at 87.61.

Sold 100% of USD/CHF at .9590.

The combination of our outperformance, lack of inspiration and our confusion over where the market will go next are the main reasons for that decision.

Below is excerpt from opening lines of today’s edition of “Sight Beyond Sight”, the macro-strategy commentary courtesy of Stamford, CT-based think tank Rareview Macro LLC. Our thanks to firm principal Neil Azous for the following observations.

Neil Azous, Rareview Macro LLC

Model Portfolio Update: Significantly Reduced Equity Net Long Exposure

Our inspiration level today is almost as low as the price of gold – that is, close to touching a low for the year.

We are struggling to find a meaningful macro catalyst or new top-down theme. None of the specific ideas we have analyzed recently are an “A Trade” and we will not deploy them ourselves, or ask you to either. The risk-reward in the short-term in many consensus themes are up 1 and down 2, not the profile of up 3 and down 1 that in the past we have always looked for.

In fact, we are finding that the psychology that has driven us all year is dissipating and for the first time we are more concerned about giving back performance in the model portfolio than generating further profits.

In the absence of a new opportunity, and following a period of healthy outperformance, a dilemma has arisen for us – markets/positions by nature mean revert. Now everyone has their own metric they watch for, and their own threshold for the mean reversion in their portfolio to start with. But let us just say that ours has been breached and it has served us well in the past to pay attention to that.

Now that may not be the case for many of you, and if we were in your position there is little question we would be pursuing the same ideas/themes in order to catch up with our benchmark. For today, we have little to offer you. However, like the Homebuilder seasonality and beta observation made yesterday (reminder BZH reported this morning and is in small cap basket we presented), we will continue to highlight ideas as and when they arise.

So in that spirit, we significantly reduced our net long equity exposure. Continue reading →

Below commentary is courtesy of extract from a.m. edition of today’s Rareview Macro’s “Sight Beyond Sight”

A Simple View: US Dollar, Gold, SPX, UST’s

Neil Azous, Rareview Macro LLC

The objectives we have laid out continue to materialize across the themes we are focused on.

The Q&A session with President Mario Draghi following today’s European Central Bank (ECB) meeting has concluded. We will leave it to the people with PHDs to debate the intricacies of what he had to say. But if price is the voting machine that always tells you the truth, then the weakness in the Euro exchange rate highlights that the press conference was simply dovish. Expect these same PHD’s to keep chasing as they lower their price targets again.

As evidenced in our most recent editions of Sight Beyond Sight, there was little doubt that Draghi would not strike a dovish tone. With his emphasis on a unanimous vote for further action if necessary and formally adding in the notion that the ECB’s balance sheet will return to 2012 levels (i.e. ~1 trillion higher), Draghi did a good job of walking back the negative tone that the media have tried to portray over the last 48-hours, especially the speculation about an internal battle/dissent/revolt building up against Draghi.

For us, it was never about whether the professionals sold the Euro after the event. They were going to do that anyway as the trading dynamics continue to point towards the Euro buckling under its own weight regardless of what Draghi says. Instead, we were more focused on a short covering event not materializing ahead of tomorrow’s US employment data and that has been largely removed for today.

So those bearish have to contend with the following factors: Continue reading →

Below excerpt is closing conclusion courtesy of Oct 28 edition of Rareview Macro LLC publication “Sight Beyond Sight”

Neil Azous, Rareview Macro LLC

The Federal Reserve (FED) will make its policy announcement tomorrow. The Bank of Japan (BoJ) will make its statement at the end of this week. The European Central Bank (ECB) meets next week. All three of them will be dovish at the end of the day.

Additionally, Jean Claude Juncker begins his presidency of the European Commission next week and that should embolden the call for fiscal help, which is required even more now that both Italy and France have changed their budget plans (see details below in Top Overnight Observations). There is no question that professionals we speak to are warming up to the idea of a larger fiscal announcement and this is tempering their bearish view on Europe to a degree.

Finally, with a positive US employment report, expectations of a Republican win in the US Mid-term Elections, and the positive seasonality associated with the start of a new month, it can be easily argued that the theme for the next two-weeks is global policy support.

The worst part of it is that everyone who was forced to reduce risk in October, and then missed the move back up, knows this is the market’s support structure regardless of the fact that QE finally ended yesterday.

This is not us being overly constructive on US equities or risk assets. After six weeks of one-way negative news flow and the sentiment shifting to extreme levels, there are now three weeks of events that should be supportive for risk. This is just the start of week number two in that period.

And that, combined with the lagging performance in the professional community, is enough to walk sentiment back even further, especially when countries like China and Sweden move out of nowhere to support the market on the upside.

MarketsMuse Editor: For the reader who requires further context re: above, the preface to above-noted thesis is… Continue reading →

Below extract from this a.m. edition of “Sight Beyond Sight”, the global-macro strategy insight courtesy of Stamford, CT-based, macro strategy “think tank” Rareview Macro LLC

Blood on the Streets Provides Counter-Trend Trading Opportunities

• Our 30,000 Foot Takeaways

• Model Portfolio Update: Closed EUROSTOXX and Dow Jones Index Short

• Model Portfolio Update: Opened Long S&P Structure

• Model Portfolio Update: Opened Eurodollar Interest Rate Steepener

• What Makes the Bounce Durable?

• Trading the Bounce

• US Equities Risk Profile for Next 48-Hours

• Watch List: Sugar, BRL/JPY and Nickel

Blood on the Streets Provides Counter-Trend Trading Opportunities

Baron Rothschild, an 18th century British nobleman and member of the Rothschild banking family, is credited with saying that “The time to buy is when there’s blood in the streets.” Since he ended up as one of the wealthiest men in the world at that time, he probably knew what he was talking about.

The objectives we laid out for risk assets have largely materialized. We would humbly point out that we were able to navigate these waters in the model portfolio fairly successfully, losing less than ~35 basis points on the week so far. With our large outperformance it is our intention to take advantage of the blood on the streets, as Rothschild would have done.

We wish we could say the same for others but our conversations are plagued with horror stories. Now, if we rub salt in someone’s wound or pinch the nerve of an investor that is just too bad. If that is you, then don’t read this edition. This is not us being cavalier. If we are wrong on some views or ideas we will keep an open mind and change our opinion, and will then simply reduce risk and move on. Continue reading →

MarketsMuse Editor Note: At risk of pounding the table too frequently by pointing to global macro strategy think tank “Rareview Macro” and their high-frequency of prescient postulating…the below excerpt from this a.m.’s edition of Rareview’s Sight Beyond Sight illustrates why this analyst is become the analyst ..For those confused by our use of ‘high frequency’, please note that we’ve filed a trademark for a new label “HFP” aka high-frequency prescience; and not to be confused with HFT aka high-frequency trading!. Premium merchandise including t-shirts, ball caps, and other items will be on sale soon!

“…The “True Pain Trade” Now Underway…Only Defence is Outright Risk Reduction”

Neil Azous, Rareview Macro LLC

Yesterday, our main argument was that US equity investors needed to be mindful of chasing higher prices as that was a “bull trap”. We specifically said:

“The key point here is that the S&P 500 finally closed below the 200-day moving average after almost two years and the bounce off the break of that record streak can be large enough to make professionals believe that the weakness is now over.

Make no mistake that is the formula for how we get to 1800 in the S&P 500 next. You suck investors back in only for them to have to liquidate all over again. This time, however, the losses are too great and the even lower prices force them to sell the positions they held onto all the way down in the first place and were not willing to relinquish that time around.

The sentiment is no longer about whether this is a correction or not. It is now about whether it is a 10% or 15% correction.”

At some point our microphone may be louder than it is at the moment, but for now this warning was dismissed by the bulk of investors. At the time of writing the S&P futures (symbols: ESZ4) are down -1.8% from yesterday’s highs. That is the very definition of new longs being trapped at higher prices.

Before dismissing this view we would remind you that the majority of professionals in this business are sheep, and to remain part of the asset gathering business they have to always put themselves in a position to capture ~60% of any market move. And, as sheep would, that is what they tried to do yesterday.

Now most participants who use a Bloomberg terminal just walk into the office and look at the World Equity Index (WEI) screen. This is a lazy exercise as it only provides updates for the major developed markets. The point is that a smart investor should also look at the markets not included on the WEI screen (i.e. Greece) and the Emerging Market Equity Indices (EMEQ) and World Bond Markets (WB) pages.

Below extract is courtesy of Oct 13 edition of ETFtrends.com and senior editor Todd Shriber

The United States Oil Fund (NYSEArca: USO) is off 6.4% in the past month as West Texas Intermediate, the U.S. benchmark oil contract, ominously descents to $80 per barrel.

Oil’s slide has wrought havoc for futures-based ETFs, such as USO, as well as scores of equity-bae funds with energy sector exposure. After a 9.5% third-quarter loss, was once the top-performing sector in the S&P 500 earlier this year has now turned into one of the worst groups. [Dour View on Energy ETFs]

Of the 25 worst-performing exchange traded funds over the past month, 12 are equity-based energy funds. However, weakness in the energy sector could be problematic for some an asset class some investors may not be overlooking as a victim of energy’s slide: High-yield bonds and the corresponding ETFs.

Booming production at the Eagle Ford Shale and other shale formations has helped make Texas the envy of large state economies. That same theme has also been viewed as one of the more favorable long-term catalysts for ETFs ranging from the SPDR S&P Oil & Gas Exploration & Production ETF (NYSEArca: XOP) to the Market Vectors Unconventional Oil & Gas ETF (NYSEArca: FRAK), but oil’s decline is threatening producers ability to profitably tap North American shale plays. [Fracking ETFs Foiled by Slumping Oil Prices]

“Texas is the anchor to shale production, employment growth, positive real estate trends, and overall positive moral. With Crude Oil at or below the cost of production for many project, the State with the highest economic multiple needs to contract,” said Rareview Macro founder Neil Azous in a research note.

But there’s more, including the threat falling oil prices pose to the high-yield bond market. Continue reading →

Below commentary is courtesy of Oct 8 a.m. notes from macro-strategy think tank Rareview Macro LLC’s “Sight Beyond Sight” and is provided as a courtesy to MarketsMuse readers who embrace smart insight. For those with interest in or exposure to the assortment of globally-focused ETFs across asset classes, we think you’ll welcome this content…If subscribing to newsletters from leading experts is not your ‘bag’ (regardless of how fairly-priced Rareview’s is), you should want to follow Rareview Macro’s twitter feed

Growth Scare Expanding Now…Large Cap Equity Indices Most at Risk

• Russia Enters the Vice-Grip

• EU Growth Profile: Cross-Asset Correlation to Reconnect & Lead EURO STOXX 50 Index Lower

• US Growth Profile: Pillars of Housing, Autos & Texas to Lead S&P 500 Index Lower

• China: H and A Share Markets Continue to Diverge…A Share Market is Correct

• Model Portfolio Update: Taking Profit or Restructuring Brazil (EWZ) Equity Position

Overnight

Right now everyone has a favorite metric that points to further disinflation. But, at the end of the day, the real world only really cares about one – Crude Oil.

Brent Crude Oil has made another new low and WTI Crude Oil has taken out the January low.

We are highlighting this first today for a number of reasons. Continue reading →

MarketsMuse Editorial Note: Below is extract from Oct 1 edition of macro-strategy commentary courtesy of Rareview Macro LLC’s daily publication “Sight Beyond Sight”..We often profile this content from macro strategy expert and author Neil Azous, simply because since we first started following SBS commentary, it has become one of those most highly-regarded independent research pieces subscribed to by more than a few of the “sharpest knives in the drawer.”

Neil Azous, Rareview Macro LLC

“….One simple way to measure the market impact of the growing pro-democracy protests in Hong Kong is to look at future assumptions for corporate dividend streams.

Specifically, we are watching the HSCEI Dividend Point Index Futures (symbol: DHCZ5) that trade on the Hong Kong Futures Exchange.

Because most of the “terminal outcome” is already in the price of the futures contract, based on the modeling of expected dividend payouts, the front-month futures contract should generally show the most acute reaction to a fast-developing live event. Put another way, the “gap risk” is much higher at the front versus the back of the futures curve.

Now, to be fair, this product is generally used by regional investors with $50-300 million in AUM as the futures are not liquid enough for the larger players. However, the fact that smaller is at times synonymous for “weaker hands” highlights that the local and small player is not yet really concerned by the protests. And what that tells us is that the possible contagion from these protests is actually lower than most people think, at least for today. Continue reading →

MarketsMuse Editor Note: We tip our hat to the folks at Rareview Macro LLC, whose ‘sightings’ we have been allowed to cite courtesy of extracts from that global macro strategy think tank’s daily newsletter Sight Beyond Sight… Why? When eyeballing the 18 Sept edition, our staff noticed that Rareview’s model portfolio has, on a YTD basis, produced a 9.7% return vs. a 4.1% average return YTD for hedge fund managers according to HFR’s 8 September report, considered a leading source of hedge fund industry analytics.

For those following only the best strategists and analysts, below are extracts from yesterday’s Sight Beyond Sight:

Neil Azous, Rareview Macro LLC

“……So while the strategy will be to remain long the US Dollar vs. the G5-G10, it will also be to take profits on emerging market and commodity currencies, including short-term and option gamma related positioning. The carry trade will return to being protected because the slope of the curve in the US Dollar move will be measured for the time being. It is important to note that many emerging market risk assets have already been though a 5-10% correction leading up to the FOMC meeting and many commodity benchmarks have broken down to new lows, including the ones with the riskiest and highest beta profile (see below Top Overnight Observations)….”

Below is excerpt courtesy of 07.29 edition of Rareview Macro’s“Sight Beyond Sight”

Small vs. Large Caps

Below are two charts of the ratio of the S&P 500 (symbol: SPY) to the Russell 2000 (symbol: IWM).

The first chart shows the performance of the ratio (i.e. long SPY vs. short IWM) on the top each time the relative strength index (i.e. 14-day RSI) reaches ~70. This ratio is currently overbought.

Neil Azous, Rareview Macro LLC

Going back to 2009 there have been ~10 points in time where the RSI reached ~70 (i.e. overbought) using the standard 14-day period. The average gain in the ratio is ~7.7% vs. the current gain at 6.6% off the July 2014 low.

The second chart shows the Fibonacci retracement levels following the GFC. The 61.8% FIB level is 1.2%. That happens to coincide with the average gain (i.e. ~7.7%) of the last 10 times that coincided with a ~70 RSI.

Courtesy of Rareview Macro’s Sight Beyond Sight 07.29

We have placed an order to buy $20 million of IWM and sell short $20mm of SPY at this 61.8% retracement level. Out stop is the 76.4% retracement level which is ~2.7% above the 61.8% retracement level. That would equate to a loss of ~$540k or ~50 basis points of the NAV. As a reminder, we refer to 50 basis points as one unit of risk.

Below excerpt from July 25 edition of “Sight Beyond Sight” is courtesy of Rareview Macro LLC

Neil Azous, Rareview Macro LLC

Overnight Commentary Strongly Centered on US Dollar, China, and NASDAQ

US Dollar

China – Operation Fox Hunt

NASDAQ

US Dollar

In the July 16th edition of Sight Beyond Sight we doubled the long US Dollar index exposure in the model portfolio and highlighted a number of catalysts for further US Dollar strength. As a reminder, the current position is long 500 U.S. Dollar Index Futures (Symbol: DXU4) for an average price of 80.4425 (original 80.28 on July 3rd + addition 80.605 on July 16th). We also hold a position of long Dollar/Swiss (USD/CHF) which helps better balance the European exposure in the basket. Collectively, if prices hold the long US Dollar position will generate about ~50 basis points of positive PnL this week.

We do not take victory laps in this newsletter as there are plenty of misses as well. We highlight this to emphasize that a long Dollar position can provide strategies that are lagging in performance with an opportunity to claw back. Additionally, this is an asset class that can absorb large inflows and no one is long in any material way currently.

Here are three most current US Dollar talking points – Structural, Technical and Data.

The consensus amongst paid forecasters with respect to the European structural backdrop continues to build. Morgan Stanley yesterday joined Nomura’s #1 ranked foreign exchange strategy team in holding this view. MS said “There were three main EUR-supportive flows that drove EUR/USD beyond what interest-rate differentials would suggest over the past two years: (1) foreign buying of peripheral bonds, (2) foreign buying of equities, and (3) official sector reserve diversification into EUR. We think all three flows are slowing and will continue to do so over coming months, leading EUR to trade more in line with macro fundamentals.” Continue reading →