(MarketsMuse blog post image courtesy of Institutional Investor)–Thanks to MiFID II, Sell-Side Research Analysts are not only unwanted, they will become increasingly underemployed in terms of compensation, or simply unemployed. This increasing view is bleak for investment bank research wonks, but provides for a career re-purposing on the part of experienced research analysts. At least that’s one thesis, as advanced by Institutional Investor’s Amy Whyte. (link to article below).

Wall Street’s investment bank research analysts, the folks who have long been notorious for peddling buy recommendations on companies in which their respective firms serve as the lead or co-lead underwriter to the company whose shares and/or bonds they tout are now facing a new professional career dilemma and its directly related to MiFID II, the EU’s revamped financial industry regulatory framework. Part of the new regs that rolled out at the beginning of 2018 require investment banks to charge their clients separately for research provided, as opposed to bundling the cost of research within trade execution fees/commissions charged to clients. This is actually a very big deal, as it now puts the onus on investment banks to not only justify the “value” of their manufacturing buy recommendations, but opens Pandora’s Box insofar as institutional investor clients of those banks can now measure the value of that research in a granular fashion.

MiFID II’s negative impact on investment bank research analysts is one that is perhaps bigger than the reputational crisis they suffered consequent to the bursting of the internet bubble during the turn of this century. Back then, research analysts were castigated for peddling grotesquely overvalued dot com stocks–many of which imploded within less than 2 years of their banks underwriting the IPOs of the same companies. For those not familiar with history, a simple revisit to the wikipedia page of former Merrill Lynch Analyst Henry Blodget provides a case study in conflicted commentary peddled by analysts back in those days (keep reading below for the Blodget story). Point being-sell-side research analysts were (deservedly) thrown under the bus for being conflicted in their recommendations, leading to a short-lived surge in startup independent research firms. Now, investment bank research analysts are facing another career crisis thanks to unbundling research regulations introduced by MiFID II.

Unbundled pricing models will change research market forever (Bloomberg Intelligence Aug 2017) Banks are adjusting their pricing models for investment research in preparation for EU reforms that will prevent research from being paid for directly using dealing commissions. In an unbundled world, based on execution-only commission rates where payments for research are separated, competition in equity research, as well as fixed-income, currency and commodities research, is likely to rise. Managers may look beyond traditional sources, triggering fragmentation. They may also move research in-house.

But all is not as bad as it sounds for the research analyst community at large. Sell-side research analysts who have strong pedigrees are presumably well-positioned to take on similar roles at buy side firms, or as the II article suggests, these folks are nicely qualified to serve as Investor Relations professionals for corporations. For US-based analysts, the urgency to repurpose is not as severe as it might be for their EU counterparts, as the US SEC has provided a reprieve for the time being according to one expert.

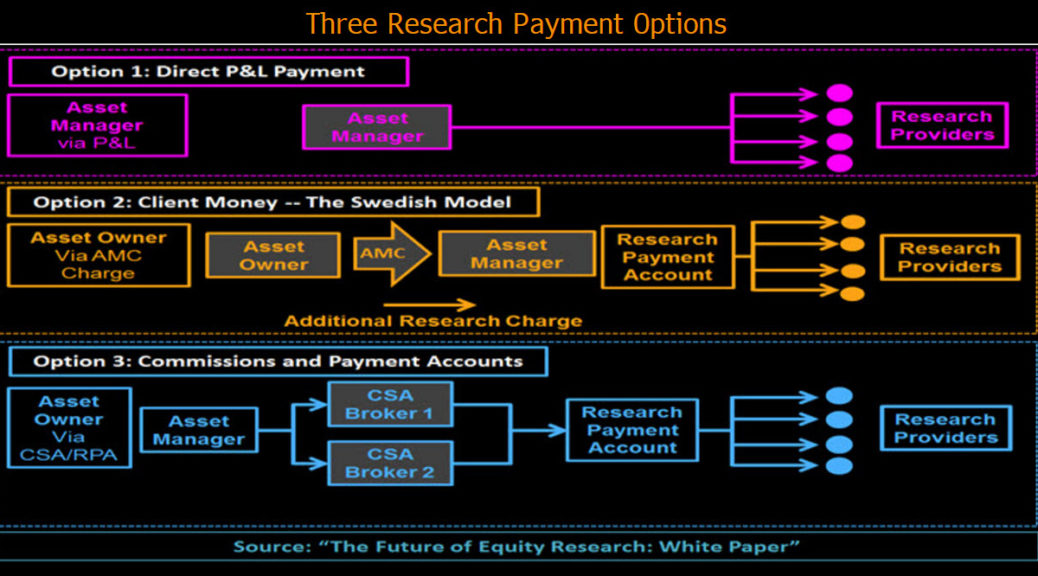

MiFID 2 regulations require investment research to be paid for in one of two ways: from a fund manager’s own account, which may be recoverable by raising fees, or via a ring-fenced client research-payment account. While regulators will permit research charges to be collected alongside transaction commissions, subject to strict conditions, there should be no link to transaction value or volume. The move to an unbundled research model will limit the long-held use of commissions and is being disruptive to the industry globally.

Henry Blodget

Flashback to Blodget….Putting into context, he was the 1990’s icon for being a dot com MarketsMuse. The likes of Henry Blodget made no bones promoting dot com stocks underwritten by his former employers Oppenheimer & Co and then Merrill Lynch. Blodget was ultimately barred for life from the securities industry for his egregious touting and to make sure the door didn’t slam his butt on the way out of Wall Street, he paid a $2mil fine and agreed to give back another $2mil that he earned while being the most prolific stock promoter of his generation. Good news-Blodget repurposed himself and is co-founder/CEO, Editor-in-Chief and publisher of financial industry rag Business Insider.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor or email: cmo@marketsmuse.com.

According to MarketsMuse market structure mavens, if you can say “dis-intermediate” five times in under 5 seconds, or if you can simply spell the word (without looking at this blog post), then “you’ll get the joke” i.e. exchange operator Bats Global Markets (acquired last year by CBOE for $3.2bil) is a disrupt-or. After sell-side firms were given direct access to a new block trading service for the European equity market launched by stock exchange operator Bats Europe in December, it was just revealed that starting next month, buy-side asset managers will gain direct access to the same block trading platform. The pending roll-out will enable buy-side traders to submit their own Indications of Interest (IOIs) so as to reduce information slippage.

Bats Europe licensed technology from Bids Trading, the largest block trading ATS by volume in the US to launch Bats LIS (Large in Scale) in December. Per reporting from Markets Media….

Dave Howson, chief operating officer at Bats Europe, told Markets Media that average trade size has grown to more than €1m over the past month since sell-side firms were given direct access to Bats LIS. He added: “We have eight to ten brokers regularly utilizing the platform with additional participants joining all the time.”

Buy-side firms have been able to access Bats LIS through a broker but the service is being rolled out so asset managers also have direct access.

Dave Howson, Bats

“Over the next month, buy side will have direct access to submit indications of interest into the Bats LIS platform,” said Howson. “One of the key benefits of the platform is that the buy side control their IOI up until it is matched before turning it over to a designated broker for execution, which means information leakage in minimized.”

Under MiFID II, the new European Union regulations which come into effect in January next year, block trades above a specified minimum size can trade under a large in scale waiver which allows market participants to negotiate trades without the need to make quotes public to meet the pre-trade transparency requirements. The ability to trade large blocks will become even more important as MiFID II also places volume caps on trading in a dark pool without a waiver.

Another MiFID II compliant service for block trading that has been introduced by Bats Europe is the Periodic Auctions book. Launched in October 2015, the Periodic Auctions book is a separate lit book that independently operates intra-day auctions throughout the day. Howson said: “A priority is to change the structure of our Periodic Auction order book to optimise the duration of the auction, which should result in increased order matching.”

If you’ve got fintech fever, or just a hot tip, a bright story idea profiling global macro, fintech, ETFs, options, or fixed income markets, or if you’d like to get visibility for your firm through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, etc., please reach out to MarketsMuse Corporate Communication Conciege via this link

He continued that another priority in Europe is to increase the volume of trading of exchange-traded funds, which should be boosted by the MiFID II requirements to report ETF trading. Howson added: “The new trade reporting obligation under MiFID II will increase transparency in ETFs so should we expect to see an increase trading of these products on trading venues.”

In June last year Bats launched a new indices business with the introduction of a UK-focused benchmark index series of 18 different indices. In December, Bats added eight indices for the French, German, Italian and Swiss markets bringing the total number of European indices managed by Bats to 26.

“We are currently focused on building European coverage with our indices,” added Howson. “Further down the road we’ll look to create products on the back of the indices, but right now we’re focused on expanding our reach.”

Bats Europe operates a trade reporting facility, BXTR, which will be registered under MiFID II. BXTR reported more than €4.8trillion in transactions last year.

EC Embraces ISIN reference code protocol for financial instrument identifiers as MiFID II nears full implementation

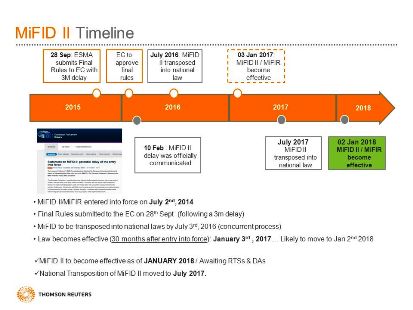

(Waters Technology |InsideReferenceData.com) 20 July 2016-The European Commission (EC) has adopted several technical standards of the Markets in Financial Instruments Directive (MiFID II), including RTS 23 (Regulatory Technical Standard), which deals with standards and formats for financial instrument reference data. The initial version of the standards mandated the International Securities Identification Number (ISIN) for reporting under MiFID II and the commission is in the process of finalizing level two texts of the regulation.

David Nowell

David Nowell, head of regulatory compliance and industry relations, UnaVista, London Stock Exchange (LSE) Group, welcomes the development, despite blistering complaints voiced by Richard Young, who leads the “open symbology’ team for Bloomberg LP, which has long been seeking to advance its own proprietary reference code protocol known as FIGI. Bloomberg LP is a privately-owned market data platform that charges upwards of USD $28,000 per user, per year to access the firm’s terminal farm.

“London Stock Exchange welcomes the European Commission’s proposals to adopt the ISIN as the instrument identifier under MiFID II. The use of the ISIN and its accompanying Classification of Financial Instruments (CFI) code allows regulators to have both an identifier and associated instrument classification data,” says Nowell.

(MarketsMedia)–European exchange-traded fund (ETF) issuers have welcomed a new service from Deutsche Börse which aims to make it easier to trade large ETF orders on the German exchange.

Deutsche Börse has launched Xetra Quote Request which allows investors to send quote requests for large orders to all registered market makers of a selected ETF, rather than having to negotiate ETF transactions bilaterally over-the-counter or through request-for-quote systems.

The market makers respond by updating their quotes in the Xetra order book, Deutsche Börse’s electronic trading platform. Investors can generally receive a response within 120 seconds of the submission of a quote request although less liquid funds may require more time than highly liquid products according to the exchange.

The process is designed to achieve a high degree of automation with straight-through processing, clearing and settlement, which reduces operational and counterparty risks, while ensuring compliance with best execution requirements for large orders.

Deutsche Börse said in a statement: “Investors therefore benefit from a potential price improvement over execution against a single market maker quote, and ensure best execution by simultaneously interacting with the full liquidity available in the order book.”

Jürgen Blumberg, head of European capital markets at Source, told Markets Media that the European ETF issuer very much liked the Deutsche Börse initiative. “In Europe approximately 70% of ETF volume is traded over-the-counter and liquidity is invisible. If there is more visibility then ETFs will be even more widely used,” he added.

Lansing agreed that the European market will benefit from more on-exchange trading.

“A number of ETP issuers (including us) have long recommended the creation of a consolidated tape (a comprehensive record of both on-exchange and OTC trades),” Lansing added. “Given that that is still in process, more trading on-exchange will go a long way to promoting greater liquidity, price discovery and transparency.”

MiFID II is due to introduce mandatory reporting for ETFs but the new regulations covering European financial markets have been delayed by one year to 2018.

For the full article from MarketsMedia, please click here

Disruptive Unbundlers, Securities Industry Untouchables, Fintech Aficionados and Innovative Altruists seek to level the investment research playing field, inspiring a bull market for independent research distribution channels, start-ups and disruptive schemes.

Investment research and expert ideas, whether within the context of equities analysis or global macro perspective, has long been the domain of sell-side investment banks, whose research insight is typically bundled as a ‘free product’ within the range of fee-based services provided, including trade execution. Those old enough to remember the ‘dot-com bubble’ days will recall that much of Wall Street’s so-called research was (and arguably still is) notorious for being heavily tilted towards “buy recommendations” in favor of the investment bank’s corporate issuer clients.

This clearly conflicted practice was perfected in the late ‘90s by the likes of poster-boy analyst Henry Blodget (since banned from the securities industry, and ironically, now Editor and CEO of financial media company Business Insider) and was lambasted by securities industry regulators when the “Internet bubble” burst. Those chasing-the-horse-after-the-barn-door-closed efforts since led to a regime of regulation and firewalls intended to distance in-house research analysts from their investment banker brethren so as to mitigate biased recommendations and conflicts of interest. Compliance officers across the industry found themselves facing a host of new rules, and that ‘compliance contagion’ served as the catalyst for a spurt in “independent research boutiques” offering “unbundled” and un-conflicted research sold as a stand-alone product with no ties to execution or trading commissions.

However compelling the notion, and despite the regulatory impetus to foster the growth of independent research boutiques, the business model for these firms has proven challenging during the past 10-15 years. Many boutique research firms floundered or failed for several crucial reasons, including but not limited to (i) the burdensome costs and means associated with creating a stand-alone brand, (ii) the challenge of delivering consistent and compelling content to institutional investment managers and sophisticated investors at a price point that could prove profitable and (iii) the non-trivial logistics required to deliver content in a compliant manner. In the interim, regulators stood by and observed, and digital delivery mechanisms for independent researchers only slowly evolved. Investment banks, never shy when it comes to creative workarounds, bolstered their research ranks and produced more content, even if mostly undifferentiated, but still promoted by the strength of the investment bank’s brand.

All of this is about to change again, causing some to conclude that regulatory market moves in cycles every decade or so, much like the stock market moves in cycles. The current bull market case for unbundled independent research is not a result of efforts by get-tough-on-Wall Street types such as New York Attorney General Eric Schneiderman or Massachusetts’ kindred spirits Elizabeth Warren and William Galvin, and the bull case is certainly not because of any efforts made by the SEC. To a certain extent, the positive outlook for those in the unbundling space is based on Moore’s Law and the advancement of Fintech-friendly applications, but it is more directly attributed to a new European Union law inspired by MiFID II, that if passed as expected, will require investment managers to pay specifically for any analyst research or related services they receive. With that new rule (which includes more than a few line items), many large money managers are starting to follow the proposed rules globally; investment banks in the U.S. (and obviously those in Europe) are devising new business models for one of their oldest and highest-profile functions: offering ideas to customers that banks can monetize through commission-based services.

More than some across the major continents believe that however much top investment bank brands are a decidedly powerful selling tool for research product, the power of the internet has enabled the distribution of independent research and enables a Chinese menu of pricing schemes via a continuously-growing universe of independent portals that invite content publishers to sell their products using an assortment of social media-powered distribution channels and revenue-sharing schemes.

Bloomberg LP has created its own independent research module accessible by 300,000+ subscribers in direct competition with Markit, the financial information services provider. Earlier this year, Interactive Brokers (NASDAQ:IBKR), the web-powered global online brokerage platform that provides direct market access to multiple exchanges and trading venues across the entire asset class spectrum quietly began enhancing its offering of third-party professional and institutional-grade research. IB’s 300,000+ accounts comprising professional traders and institutional clients may subscribe to research made available in the trading platform, Trader Workstation (TWS). At the same time, IB began promoting these third-party research providers via IB Traders’ Insight, a blog embedded within the firm’s Education module that covers the full range of investment styles from more than two dozen content providers.

While bolstering objective research content is a natural business extension for those having captive brokerage clients and for terminal-farm behemoths, perhaps even more interesting is that start-ups in the unbundling space are starting to percolate.

On the European side of the pond, UK-based SubstantiveResearch, created earlier this year by former EuroMoney Magazine publisher Mike Carrodus, is positioned to be an institutional research thought- leader that curates and filters both independent and sell side global macro research, with a sleeve that hosts regulatory events for investment manager content consumers and sell-side content providers. Start-ups in the US include among others, Airex Inc. , which dubs itself “the Amazon.com for financial digital content” and recently secured funding from fintech-focused merchant bank SenaHill Partners. TalkMarkets.com is another notable entrant to the space, and was created in late 2014 by Boaz Berkowitz, a former “Bloombergite” who was also the original brain behind Seeking Alpha. From the traditional financial media publishing world, industry stalwart Futures Magazine, recently re-branded as “Modern Trader” and the parent to hedge fund news outlet FinAlternatives is also embracing the research content unbundling movement as a means towards capturing more Alpha and better monetizing relationships with content providers. Each have their own business models, including the use of cloud-based technology and coupled with the muscle of creative online marketing, social media tactics and search-engine ranking techniques.

While the start-up space is often littered with short shelf-life stories, these new unbundled research distribution vehicles are being enabled by the fintech revolution and embraced by distributors of content, high-profile independent research providers, as well as by at least one major bank seeking to hedge its internal bets; earlier this year, Deutsche Bank inked a deal with upstart Airex, such that DB’s proprietary equity research is available on a delayed basis and can be purchased by any AIREX Market shopper. In the case of now 6-month old TalkMarkets, they are embracing an advertising-based business model, which is predicated on building an outsized audience of sophisticated retail investors for prospective advertisers. To date, they have enlisted more than 350 content providers and 10,000+ registered users. While there is no cost to access the platform, content providers are able to upsell subscription-based services and at the same time, earn ‘points’ that can be converted into the private company’s equity shares.

Neil Azous, Rareview Macro

According to former sell-side global macro strategist Neil Azous, the Founder/Managing Member of think tank Rareview Macro LLC, and the publisher of subscription-based “Sight Beyond Sight” which is now being distributed across several channels apart from the firm’s website (including via Interactive Brokers), “Truly superior, high-quality content, including actionable ideas remains relatively scarce, but the fact remains, content has become commoditized. The good news is that banks are not the sole source of carefully-conceived research and the better news is that conflict-free content publishers can now more easily distribute via a broad universe of narrow-casting, web-based channels.”

Added Azous, “For independent research providers and trade idea generators, it’s arguably a watershed moment. As new rules take shape, content publishers, including those who previously worked under investment bank banners, can now reach an exponentially larger universe of content buyers through these new distribution channels. It’s a numbers game; instead of working inside an investment bank and trying to ‘sell’ a traditionally high-priced product to a relatively narrow list of captive clients, the more progressive idea generators can re-tool their pricing and make their product available to exponentially more buyers, and in a way that conforms to and stays within goal posts of compliance-sensitive folks.”

However much it makes sense to foster the easy distribution of independent and un-conflicted research, Wall Street et. al. is not going to easily abrogate their role for providing ideas or forgo the trade execution commissions derived from those proprietary ideas. Banks are reported to be devising new pricing models for investment research in view of EU proposals that could prevent research from being paid for using dealing commissions. In an unbundled world, where payments are separated, competition for equity and credit research may increase as asset managers look beyond traditional sources, which may trigger fragmentation. They may also move research in-house. The U.K.’s FCA, which is driving the debate, has endorsed the EU proposals.

As noted within the most recent edition of Pensions & Investments Magazine, Barclays PLC, Citigroup Inc., Credit Suisse Group AG and Deutsche Bank AG are working with clients to come up with pricing for the analyst research customers receive, according to bank executives. Prices are expected to range from roughly $50,000 a year to receive standard research notes, up to millions of dollars for bespoke research and open-door access to analysts.

“We are working to change the mind-set so that fund managers understand that research should be treated as a scarce resource. There is a great opportunity to tap into experts in their fields at brokers, but we need to really think about the value of research and determine the right amount to pay for it,” said Nick Anderson, head of equities research at Henderson Global Investors.

The following [excerpted] analysis is by Bloomberg Intelligence analysts Sarah Jane Mahmud and Alison Williams and helps summarize the current outlook. It originally appeared on the Bloomberg Professional service. Continue reading →