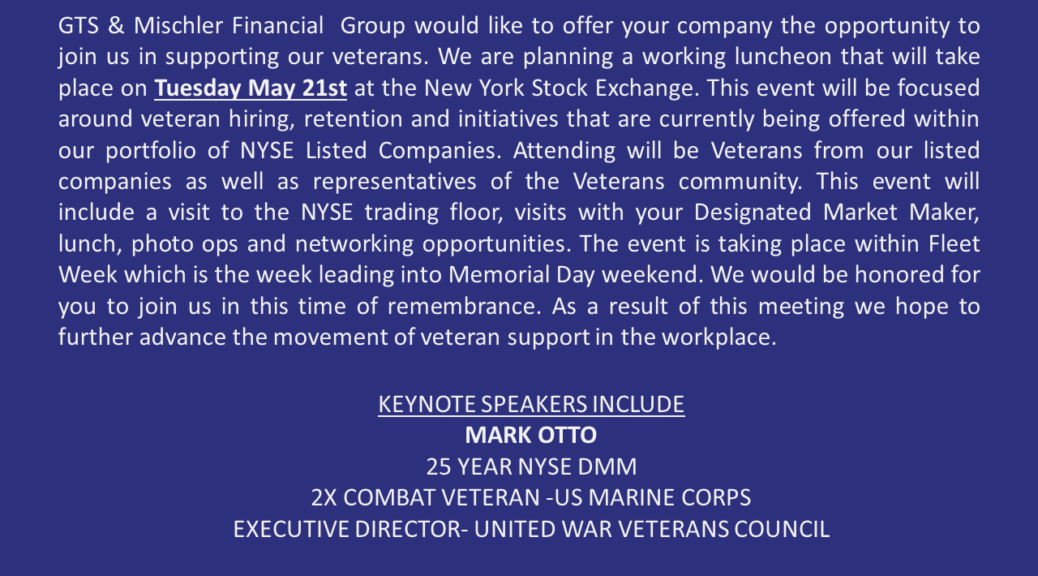

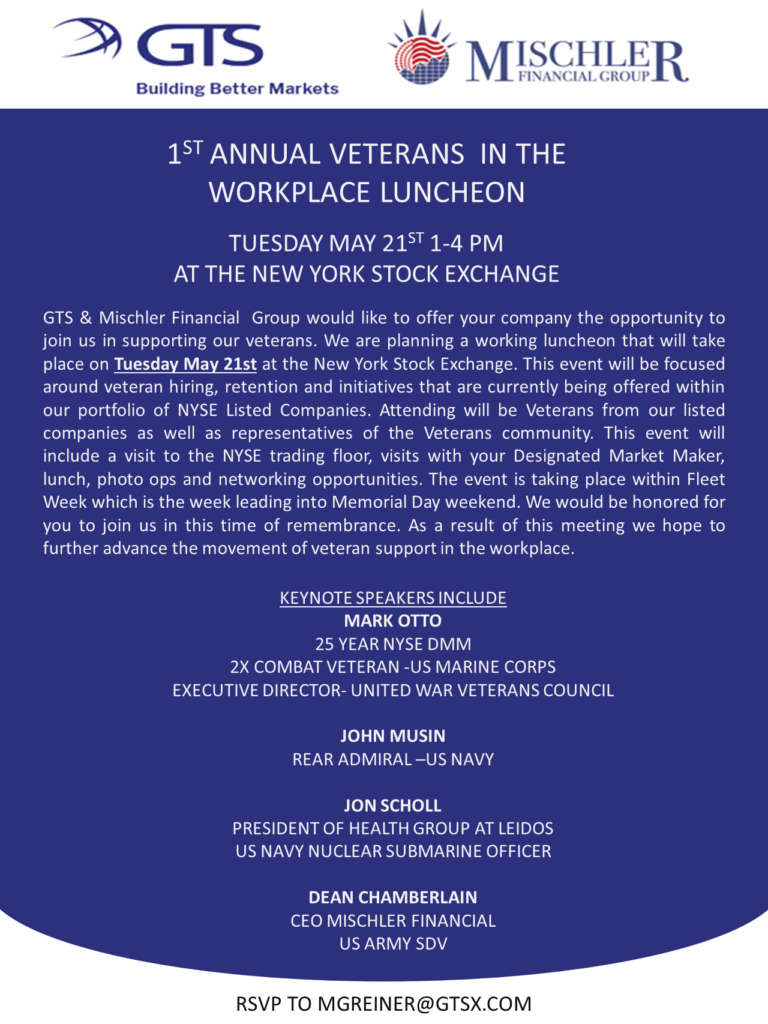

Working Luncheon will celebrate veterans in the workplace with attendees from notable publicly traded companies

May 16, 2019 10:00 AM Eastern Daylight Time

NEW YORK–(BUSINESS WIRE)–GTS, a leading electronic market maker across global financial

instruments and the largest designated market maker at the New York Stock

Exchange (“NYSE”), in partnership with veteran-owned broker dealer Mischler Financial Group, will hold the first annual ‘Veterans

in the Workplace’ luncheon at the NYSE on May 21, 2019.

The luncheon will kick

off the 31st annual Fleet Week New York, which will

take place from May 22-28. Attendees will include veteran C-level executives

and employees of publicly listed companies, high-ranking military officials,

and student veterans from local New York colleges.

The event is being

organized by Mark Otto, Global Markets Commentator for GTS and U.S. Marine

Corps combat veteran. Otto also serves as Executive Director of the United War

Veterans Council (“UWVC”), which is the organization that produces the New York

City Veterans Day Parade.

“I am thrilled to

organize the first-ever ‘Veterans in the Workplace’ luncheon at the NYSE to

kick off Fleet Week in New York,” Otto said. “This event will be a great

opportunity to honor both those who are actively serving as well as veterans who,

after serving our country, have rejoined the workforce to serve our capital

markets.”

The event will feature

three keynote speakers:

Dean

Chamberlain, CEO of Mischler

Financial, West Point graduate and former U.S. Army Officer;

Rear

Admiral John Mustin, Deputy Commander of

the U.S. Second Fleet and Naval Surface Force Atlantic;

Jon

Scholl, President of the

Health Group at Leidos, U.S. Naval Academy graduate and 5-year U.S. Navy

veteran; and

Diego

Rubio, U.S. Army Veteran

and Co-founder of Women Veterans on Wall Street (“wVOWS”)

“It is an honor to

deliver a keynote address for a unique program that includes fellow military

veterans in the workforce,” Chamberlain said. “As the CEO of the industry’s

oldest service-disabled veteran-owned business, it is always inspiring to work

alongside corporations that provide veterans with opportunities to leverage the

skills acquired in the course of their service and provide focused programs to

help them successfully transition to new careers.”

In addition to the

keynote speakers, the luncheon will provide attendees with a networking

opportunity, and will highlight topics including veteran-hiring retention and

the different initiatives companies are taking to help veterans.

Approximately forty

C-level executives and employees from publicly listed companies such as Wabash

National (NSYE: WNC), DHI Group (NYSE: DHX), Leidos (NYSE: LDOS) and Samsung

will be in attendance.

Fleet Week is a

weeklong celebration of the U.S. military’s sea services and gives the citizens

of New York the opportunity to meet and interact with members of the U.S. Navy,

U.S. Marine Corps and U.S. Coast Guard. This year, the U.S. Navy expects about

2,600 Sailors, Marines and Coast Guardsmen will be on hand.

About GTS

GTS is a global

electronic market maker, powered by combining market expertise with innovative,

proprietary technology. As a quantitative trading firm continually building for

the future, GTS leverages the latest in artificial intelligence systems and

sophisticated pricing models to bring consistency, efficiency, and transparency

to today’s financial markets. GTS accounts for 3-6% of daily cash equities

volume in the U.S. and trades over 10,000 different instruments globally. GTS

is the largest Designated Market Maker (DMM) at the New York Stock Exchange,

responsible for nearly $12.5 trillion of market capitalization.

For more information on GTS, please visit www.gtsx.com.

About Mischler

Financial Group

Established in 1994,

Mischler Financial Group (“Mischler”) is the financial industry’s oldest

diversity-certified investment bank and institutional brokerage owned and

operated by service-disabled veterans, the firm was the first FINRA member to

be designated as a Service-Disabled-Veteran-Business Enterprise (SDVBE).

Mischler is recognized for its role as a leading capital markets boutique

operating across the primary and secondary financial market ecosystem. The firm

serves Fortune corporate treasurers in the course of their issuing new debt and

equity offerings and administering their respective corporate share repurchase

aka 10b-18 programs. In many initiatives, Mischler is viewed as a pure

complement to the role played by issuers’ lead underwriters and also assists

state and local governments in selling tax-exempt and taxable municipal

securities. Investment management clients of the firm’s secondary market

execution platform include a broad spectrum of public plan sponsors and

investment fund managers. Mischler also provides cash management for government

entities and corporations, and asset management programs for liquid and

alternative investment strategies. Mischler maintains offices in 8 major cities

and is staffed by more than 50 securities industry veterans.

Visit https://www.mischlerfinancial.com for more information.

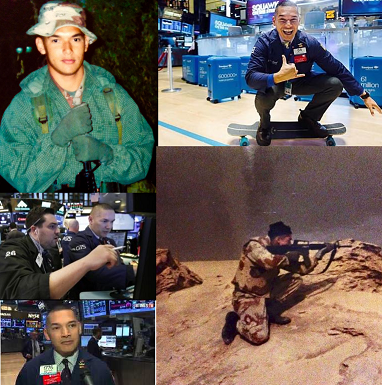

US Marine veteran of Operation Just Cause and Operation Desert Storm and veteran NYSE floor trader enlists with designated market-maker GTS with rank of Global Market Commentator

From the USMC to the NYSE, Mark Otto re-defines the phrase ‘veteran’ when considering his pedigree as a highly-decorated former US Marine and the 25 years of financial industry service he’s racked up since hanging up his gun belt. Former Marine Corporal Otto saw combat throughout his 4 years as an enlisted solider (first 1989 Panama Invasion “Operation Just Cause”and thereafter, Operation Desert Storm and then parachuted into the line of fire on the global financial industry’s most iconic battle field: the trading floor of the New York Stock Exchange. After three tours of duty serving under the commands of NYSE floor specialists Susquehanna Group, Knight Capital and J. Streicher, Otto will now be serving under a new command, he’s just signed on with the veteran-friendly NYSE Designated Market-Maker, GTS where Otto will have the rank Global Market Commentator. In November, GTS announced they had secured a minority stake in veteran-owned investment bank and institutional brokerage, Mischler Financial Group

Excerpt from the Jan 17 ,2019 press release is below:

Mark Otto-from the USMC to NYSE

NEW YORK–(BUSINESS WIRE)–GTS, a leading electronic market maker across global financial instruments, today announced the addition of U.S. Marine Corps combat veteran and experienced equities trader Mark Otto as the firm’s first Global Market Commentator.

As Global Market Commentator for GTS, Otto will combine his specialty of trading American depositary receipts (“ADR”), algorithmic trading, market making and volatility trading with his experience trading in times of historic geopolitical events and market turmoil such as the 2008 Financial Crisis, the Flash Crash, the Greek Debt Crisis, Eurozone Debt Crisis and Brexit to provide market commentary on current trends and their impact on the securities markets.

“I am thrilled to continue my career on the NYSE with GTS,” Mark Otto said, “So much of the pricing of stocks results from international developments and interconnected global economies. It’s an honor for me to share my commentary and views as part of the GTS platform. The firm is a pioneer in bringing innovation to the marketplace and it is an incredible opportunity for me to be teaming up with such an important player in the global capital markets ecosystem.”

US Marine Corps Veteran and NYSE floor veteran Mark Otto

Between 1988 and 1992, Otto served under the 2nd Surveillance Renaissance and Intelligence Group based out of Camp Lejeune, North Carolina. During his military service, Otto saw combat during the Panama Invasion and Operation Desert Storm, as well as leading surveillance teams observing and securing U.S. boarders in support of Federal Law Enforcement agencies. Otto received over a dozen military decorations and achievements, including the Combat Action Ribbon with Gold Star, Joint Meritorious Unit Commendation and Airborne Jump Wings.

GTS is the largest Designated Market Maker (“DMM”) at the New York Stock Exchange (“NYSE”) and has an extensive track record of responsibly using best-of-class technology to bring better price discovery, trade execution and transparency to the markets. At the NYSE, GTS is responsible for the trading in more than 900 public companies that have a total market capitalization of approximately $13 trillion dollars. Listed securities include blue chip companies ranging from ExxonMobil (NYSE: XOM) and Ford (NYSE: F) to international companies such as Alibaba (NYSE: BABA) to leading global technology companies like Oracle (NYSE: ORCL) and AT&T (NYSE: T).

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

Stock Price Implosion Leads Some to Challenge Current Market Structure; HFT Firms Are Under Attack, Again…

Heads Up to High-Frequency Firms: Time to Hire a PR Crisis Manager Again, Call Your Lobbyists, Book Your Plane Tickets to Washington DC.

Before “bidding on” to the anti-HFT and anti-ETF remarks circulated by the assortment of market pundits appearing on Bloomberg, Reuters or the financial media megaphone channel, CNBC, you should know that SecTres Mnunchin has already weighed in. So has the SEC’s favorite tech entrepreneur, Mark Cuban. So has icon stock investor Leon Cooperman, who has the ear of Mnuchin and others. There’s a whole ‘hang-em-high’ crowd assembling to lay blame on high-frequency trading for the latest market routs. According to CNBC, Trump favorite Mike Flynn was overheard shouting to Mnuchin and Trump: “Lock them up!”

NYSE DMM Citadel Securities started as a HFT prop trading firm

But, unless you’ve been investing in or trading in the equities markets for at least 20 years, you probably have no conception of a simple premise: markets go up and markets go down. Blame games are easy to play, equities investing is not always easy.

Traditional drivers to stock price movements include simple, time-tested fundamentals: the interest rate environment, the economic cycle, the value of the US dollar vs. other currencies, corporate revenue and profit, corporate debt levels, consumer debt levels, trends in residential real estate prices and other consumer optimism metrics. Yes, you can throw in the degree of confidence in the current government administration and a bunch of other geopolitical stuff (including tariff wars, Brexit event, and total uncertainty in many countries’ leadership–including the US) into the mix. We’ve all grown accustomed to the minute-to-minute chaos caused by the current president. His impact on stock prices is powered by his Twitter comments about China, the Federal Reserve Chairman, and blaming the latest government shutdown on democrats. Beyond that, institutional investors can only make investment decisions based on reality within context of company earnings reports and not easily-fudged economic data. Investors should NOT make decisions based on a reality TV show produced in Foggy Bottom.

But, we should agree on one thing: the combination of complacent investing, a belief that prices of company shares will go up year after year is a fool’s view. The topic of debate in this post is whether the evolution of high-frequency trading (aka HFT) weaponry has contributed (yet again) to the large (downward) percentage moves in stock prices during the recent weeks. The sell-off, which arguably began during the first week of October, has led to an approximate 20% decline in the leading stock indices from the record highs. Many individual share prices have suffered bigger mark-downs, most notably tech sector stocks. Before asserting that high-frequency trading algorithms are the culprit, one need to ponder whether those same HFT tools also contributed to the nearly 50% gains the stock market has enjoyed since the 2016 US presidential election (two years ago)?

Whatever black swans have been flying over head for the past 6 months, now that equity prices have suffered multiple-day declines of 1%-3% (and the interim 1%-2% “dead cat bounce”) we need to blame someone!! After all, our very own president has been unwavering in his leadership mantra: “When the shit hits the fan, blame someone else for the problem!”

Let’s say you want to blame HFT firms for the slide. Considering the fact that today, the 3 largest NYSE market-makers are better known

Specialist traders work at a Virtu Financial booth on the floor of the New York Stock Exchange April 16, 2015. Shares of electronic trading firm Virtu Financial Inc rose as much as 24.6 percent during their IPO, valuing the company at about $3.23 billion. REUTERS/Brendan McDermid – RTR4XMJS

for their legacy as high-frequency trading outfits, its easy to be cynical. These are ‘not your father’s NYSE specialist firm’, these are young quant jocks who made a ton of money as HFT prop trading shops starting back in the early 2000’s, and more recently, used some of that cash to purchase the legacy NYSE market-maker firms; the firms responsible for maintaining fair and orderly markets in NYSE listed companies. Now known as NYSE “DMMs”, they (actually their computers) also have the “first look” at orders to trade shares in which they are now the designated market-maker for. Instead of old-fashioned auction markets, these folks utilize algorithmic trading tools to match buyers and sellers and also trade for themselves. As a consequence, there is circumstantial evidence these firms are, to some extent, culpable for the rapid reflex moves in share prices.

Keep in mind, the flip-side is that these ‘HFT black boxes’ are also providing instantaneous liquidity, price transparency, and facilitate exiting or entering a investment position in less time than it takes to hit a ‘send’ button (until someone unplugs the machine after realizing they’ve risked the entire firm’s capital). Further, because everything happens in nano-seconds, one can argue that bear market cycles –periods that typically reflect recessionary pressures and in turn, signals that lead to a negative impact on the value of a company’s equity shares—are now much shorter in duration when compared to cycles going back 60-70 years.

To the first question, who can forget the May 2010 ‘Flash Crash’—an event that was certainly connected to HFT computers plugged into the walls surrounding the NYSE and NASDAQ computer server farms–and then became unplugged by humans when markets cratered due to a “fat finger” episode. We’ll tell you who cannot remember that event (other than having read about it years later): upwards of 1/3 of current ‘senior’ Wall Street quant jock HFT programmers who code the HFT machinery. Many of them were mining bitcoins in their MIT dorm rooms back in 2010. How many of the current generation of ‘systematic traders’ who now oversee billions of dollars were beyond high school in 2004? How many current trading desk wonks were around during the dot com bubble? How many folks who worked on trading desks in 1987 are even still alive, no less working in the business? Have you gotten the point, yet?

Because our pundits have accurately predicted this latest market down draft, allow us to further predict that we want to be “long on” private jet services to Washington (NYSE: BRK.A) and we’d love to invest in engagement contracts issued by PR Crisis Management gurus who represent these folks; they are presumably getting calls already by the best-known HFT honchos, starting yesterday.

Let’s be clear, the fundamental economic underpinnings that power equity prices have been sending mixed (warning) signals for months. OK, employment figures have been good, but Trump told us while campaigning for president that “US Employment figures are fake and fraudulent.” Yes, corporate earnings have met expectations, but nobody has delivered out-sized reports, and many companies have been sweating to provide realistic expectations, not wild-ass projections. According to recent polls, nearly 50% of Fortune CFOs are anticipating a recession will hit the US economy in 2019. 80% of CFOs believe a recession will be upon us before the end of 2020. Many multi-nationals based in the US are lamenting “Tariff Man” tweets. He says ‘US companies with US employees that make/sell products to US consumers will benefit, and the big companies have plenty of money to cushion the blows..” Really?!

So, fundamentals have been weakening during the past 2 quarters (unemployment figures aside). Even for those who subscribe to technical analysis and historic charts, the writing has been on the wall for months: “Caution Mr. Robinson, Caution!”

High-flying tech company shares started cracking in the 2nd quarter of 2018. They’ve been under an assortment of pressures that range from severe government and shareholder scrutiny to simple supply/demand obstacles impacting their business models (e.g. FB down nearly 40%, GOOG down 30% from its high, AAPL down 40%, AMZN down etc etc.) Bank stocks have been pummeled for the most part, even if GS’s latest beating is connected to yet another multi-billion dollar scandal. Big ticket corporate acquisitions made in the past 2 years have resulted in transition management problems. Corporate balance sheets have become increasingly overly-bloated with debt, thanks to folks on Wall Street who came up with a new pitch to corporate treasurers starting back in 2011: “We’ll float your bond offering (and get a big fee), you use the proceeds to repurchase outstanding shares, and you’ll make your EPS numbers look fantastic; everyone wins!!” Until the music stops, of course. Corporate share repurchases have been credited with keeping equity prices stable and moving higher for upwards of seven years; the brokers are making nice commission on executing those buybacks and all is good with the world, until its not.

Stock market chartists started raising red flags in October. Corporate debt issuance came to a crashing stop in the last 6-8 weeks. That was a big signal. Less than two dozen Fortune companies have actually been buying back debt in the past quarter in preparation for the next shoe to drop; the one with the word ‘recession’ stamped on the bottom of each shoe. The notion that corporations should unwind the ‘sell debt, buy shares’ trade –by issuing new shares and using the proceeds to balance the balance sheet and repurchase outstanding debt is an idea that no investment bank would even suggest in his sleep, no less in an office. It would be professional suicide for a corporate CFO to even suggest that idea makes sense. Geopolitical impact re Trump’s tariff war is hitting US companies and US workers, even if not the Trump Hotel enterprise. The corporate tax cut was a short shot of heroin that stimulated the stock market, but increased the Federal deficit by nearly $1trillion. (Let’s not forget that Trump campaigned on reducing debt, not increasing it–but so does every other candidate). Now people are coming off the sugar high and that’s how/why stock prices revert to the mean.

Tariff Wars, Brexit and the assortment of geopolitical catastrophes have all been thrown into the mixing bowl. Crude oil prices have been crushed–along with the share prices of companies that drill, process and sell oil-based products. Yes, we’ll repeat: employment figures have been great, but as Donald Trump said throughout his presidential campaign, “Nobody can believe government employment figures, they’re all fake news!”

When weighing the assortment of fundamental signals that have been brightly broadcast throughout the past 9-12 months—and certainly since October of this year, anyone who had not re-balanced or pared down exposure to equities has no business investing in stocks. Its easy to say “Ok, 20-20 hindsight is great..blah blah blah..” For those following @marketsmuse, there’s no 20-20 hindsight; our resident pundits (with trading market pedigrees that go back to the 1980’s) have been shouting “Caution Ahead!!” for at least 4 months. (see the pinned tweet). But, who wants to listen to experienced (if not cynical) professionals who have lived through multiple market cycles, especially when prices keep going up? Who wants to risk taking a profit and paying taxes on those gains when the asset value keeps going up, with or without fundamental justification? The answer: people who are (i) naïve (ii) overly-optimistic (iii) financially irresponsible (iv) not old enough to appreciate that what goes up, must go down.

Whatever black swans have been flying over head for the past 6 months, now that equity prices have suffered multiple-day declines of 1%-3% (and the interim 1%-2% “dead cat bounce”) we need to blame someone!! After all, our very own president has been unwavering in his leadership mantra: “When the shit hits the fan, blame someone else for the problem!”

Before the ink was dry on the famous Michael Lewis book “Flash Boys,” which profiled the May 2010 stock market crash, everyone knew who to blame. Before the first 1000 copies of that book left Barnes & Noble, government officials and regulators were busy sending out outlook meeting invites to the primary suspects-the heads of HFT proprietary trading firms that had come to dominate the trading of shares in US companies listed on public exchanges (and ‘dark venues), as well as stock index futures traded on electronic venues in Chicago.

Rules were introduced. Market structure lobbying groups were formed. Exchange executives pilot tested uptick rule changes. Fintech firms that provided ‘better solutions’ now represent more than just a cottage industry as evidenced by the fact, three of the leading HFT firms have through acquisition, become the three largest NYSE DMMs. For old folks, DMM is the contemporary phrase for ‘floor specialist’-the folks who are responsible for maintaining fair and orderly markets in the companies the NYSE assigns to market-makers on the floor of the NYSE. Pay-to-play and maker-taker rebate schemes advanced by brokers and exchange venues have flourished. Blah Blah Blah. Along the way, the US equities market, spurred by improving economic circumstances, and the last 10 years have been pretty much one long wet dream for traders and stock investors. The evolution of high-frequency trading morphed even more.

Irrespective of bull vs. bear views on individual stocks and stock indices and the 1500+ Exchange-Traded Funds that provide thematic investing styles, more than a carload of institutional investment managers still agree on one simple fact: share price movements in individual companies and ETFs are exacerbated by high-powered black boxes that spit out millions of orders per minute. Those orders are often based on what has transpired in the markets during the past few seconds. This algorithmic approach to trading causes educated investors to scratch their heads when observing the value of shares in public companies can gyrate so violently in the course of an hour or a day, despite the fact those companies haven’t made any earnings report nor announced any positive or negative news as to the health of their business or the industry they sit in.

How does a company’s enterprise value move 10% down one day, then 5% up the next? Are there so many investors with differing views who are expressing these views constantly via buying and selling millions of shares? No. Honest electronic trading industry experts will estimate that at least 80% of the time, transactions taking place at the NYSE or NASDAQ are between two ‘transformers’; computer bots that are set on auto-trade. These black box powered bots do not represent investors, they don’t smoke (unless the computer is overheated and not residing in a freezer), they don’t curse and they don’t sweat—they simply spit out–orders based on algorithms.

Put more simply, actual investors are not involved in upwards of 90% of the trades taking place. Bottom line: the exaggerated changes in publicly traded corporate enterprise values that take place from second to second are even more pronounced as prices move lower. That’s a real fact, not a Kelly Ann Conway or Sarah Huckabee-style “alternative fact.” More than a handful of objective market observers and participants have long argued that Wall Street has evolved into a Battle of the Transformers”; price moves and volatility are powered by computers, not by momentary sentiment changes on the part of real investors.

But, we live in a blame game world, as best evidenced by our so-called leaders (yes, we’re referring to the current occupant of the White House) who, when faced with obstacles or after making stupid decisions, automatically blame others for the disaster that occurred recently. And those blames are applauded by the blind mice and sheep who go along with the stupid decisions made for them.

Because our pundits have accurately predicted this latest market down draft, allow us to further predict that we want to be “long on” private jet services to Washington (NYSE: BRK.A) and we’d love to invest in engagement contracts issued by Wall Street-friendly PR Crisis Management guru. Those folks will be on speed dial for the best-known HFT honchos, starting yesterday. Caveat Emptor: PR crisis management should be advanced by smart folks, not those trained in the art of jibber jabber and deflection. If there is a fundamental flaw, acknowledge it and implement transparent steps that will appease the plaintiffs and provide real solutions to the ‘problem’ .

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

Trifecta Month for GTS; NYSE DMM, Quant-Trading Powerhouse and Fin-Tech Think-Tank Now Aligned With Investment Bank Specializing in Primary Debt & Equity Capital Markets

GTS, the NYSE’s Top DMM, and one of the global trading market’s leading multi-asset electronic market-makers, is on a strategic deal-making binge. On the heels of GTS co-founder and CEO Ari Rubenstein’s November 2 announcement that his firm acquired Cantor Fitzgerald’s 35-member ETF market-making and institutional broking crew, last Thursday while in London, Rubenstein announced that GTS is expanding its collaboration with BNP Paribas to now include live-streaming US equities pricing, on top of already delivering GTS’s UST price feed through BNP’s platform. Making November a hat-trick month for GTS, Rubenstein today announced that his firm is joining forces with boutique investment bank Mischler Financial Group (“Mischler”), a specialist in primary debt and equity capital markets and institutional brokerage providing secondary market execution for equities and fixed income.

Founded in 1994, Mischler Financial is also the industry’s oldest diversity firm owned and operated by service-disabled veterans; a designation that enables GTS to advance a Diversity & Inclusion (D&I) value-add to its armory of new solutions and client experience that GTS will bring to investment managers and issuers of debt and equity across the listed-company landscape.

Below is the opening extract of the press release.

New York, NY – November 19, 2018 – GTS, the New York Stock Exchange’s largest Designated Market-Maker (“DMM”) and a leading electronic trading firm, and Mischler Financial Group, Inc. (“Mischler”), the financial services industry’s oldest minority broker-dealer owned and operated by service-disabled veterans, today announced a strategic alliance that will establish a best-in-class offering for primary debt and equity market underwriting as well as secondary market best execution across the capital markets.

The partnership, which is anchored by a technology-powered offering for public companies and a broad universe of capital markets participants, will yield a low-cost, more efficient and more effective trade execution experience. Mischler will become a “forward operating base” for the growing GTS capital markets franchise, affording clients access to technology and sources of liquidity that are generally only available to the world’s most sophisticated investors.

Founded in 2006 as a proprietary, quantitative trading firm, GTS is now a recognized thought-leader in market structure and proudly oversees trading for more than one-third of NYSE-listed companies. The firm has an extensive track record developing and deploying proprietary, industry-best technology to bring better price discovery, trade execution and transparency to the markets.

“This is a high-tech, high-touch partnership designed to meet the needs of a new generation of issuers, asset managers, and trading and investment professionals seeking low-impact market liquidity and best-in-class execution,” said Ari Rubenstein, Co-Founder and Chief Executive Officer of GTS. “Clients are rightfully demanding innovation in the marketplace, and this alliance is uniquely designed to provide that and much more.”

Mischler, established in 1994, is an active underwriter across global equities, corporate and municipal debt, government securities and structured products. In the last three years alone, Mischler has played a role in almost 700 primary debt and equity market transactions. The firm also provides conflict-free share repurchase services for corporate treasurers as well as secondary market trade execution in equities and fixed income for a discrete universe of public plan sponsors and institutional investment managers.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

Breaking News: GTS Securities, the NYSE’s biggest specialist firm aka Designated Market Maker (“DMM”) and one of the electronic market-making world’s biggest players in the FX and rates markets is now aiming to become the ETF industry’s biggest market-maker the old-fashioned way, by buying into the space. After several months of speculation and rumors of a pending deal, GTS formally announced today they have acquired the entire team of ETF brokers and traders from Cantor Fitzgerald. According to the press release issued by GTS, the deal to acquire Cantor’s ETF team of approximately 35 ETF sales traders led by ETF industry veteran Reginald Browne is expected to close in February 2019. Terms of the transaction were not disclosed.

(l)Reginald “ETF Godfather” Browne (r) Ari Rubenstein, co-founder GTS Securities

GTS was established by former NY Merc floor traders Ari Rubenstein and David Lieberman, who looked to Amit Livnat, a top-of-class graduate from the world famous Israel Institute of Technology to serve as the firm’s resident tech wonk. Of the three, Rubenstein is the camera-facing thought-leader, who first cut his teeth in the trading business as a runner on the floor of the New York Mercantile Exchange and later became a floor trader on the New York Cotton Exchange. Aligning with fellow floor trader David Lieberman and Livnat, GTS was first positioned as a quantitative prop trading firm that leveraged in-house trading technology and home-grown algorithms to peel incremental profits by executing tens of thousands of transactions per day across US equities, rates and FX markets. GTS levered its high-frequency trading domain expertise and morphed into its current role as a global trading powerhouse once the firm took control of the NYSE’s biggest specialist firm operated by a unit of Barclays Bank.

“For the first time on a scale never seen before, the most sophisticated Wall Street technology is being deployed for mainstream investors, be they institutional or retail,” said Ari Rubenstein, CEO and co-founder of GTS. “Investors around the world can now leverage the very best in machine learning, artificial intelligence and execution technology to help them save money whenever they trade and invest. This is an unprecedented opportunity for investors that unites unrivaled innovation with pioneering client service – while enhancing the capital raising opportunities for listed companies.”Stacey Cunningham, president of the New York Stock Exchange said, “The NYSE and our partners embody the synthesis of technology and human judgment, leading to the best possible outcome for investors and issuers.”

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.

Tom Farley, the former top gun at the NYSE, has long advocated the benefits of raising capital via the construct of Special Purpose Acquisition Company aka “SPAC”, aka “Blank Check company.” Now he’s become the CEO poster boy for SPACs with the formal IPO and NYSE listing of Fintech SPAC Far Point Acquisition Corp., a financial technology-themed acquisition company, which is backed by activist investor and fintech aficiondo Dan Loeb.

Tom Farley, Far Point Acquisition Corp

42-yearold Farley, a Georgetown University alum and former ICE senior executive and the second youngest person to serve as NYSE President when taking on that role in 2012, will serve as CEO of the ‘fintech buyout’ company. Farley is arguably one of the industry’s most fintech-fluent folks, given his role in helping to transform NYSE into a financial industry trading technology centerpiece.

Farley’s long-held view towards the future is evidenced by the fact NYSE’s two most dominant designated market-makers aka “DMM” firms, GTS Securities and Virtu Financial are companies that are synonymous with the phrase fintech. Both firms started their journeys as prop trading firms specializing in ‘high-frequency-trading’ and their more recently attained NYSE ‘specialist’ roles are powered by next generation in-house algorithmic trading and artificial intelligence tool kits. GTS Founder Ari Rubenstein, whose NYSE DMM is responsible for maintaining fair and orderly markets in 1200+ companies and who also oversees one of the industry’s most robust, multi-asset liquidity-providing prop trading platforms, is also a founding member of industry trade group Modern Markets Initiative (MMI)

Back to SPACs- For those who may have missed the multiple memos coming out of the biggest investment banks, the blank check company construct provides a means to create a publicly-traded ‘shell company’, whose use of proceeds is intended to acquire a private company (or companies) and seamlessly “jump the shark” by rolling the private company into the publicly-listed company without bearing the burden of the time and cost that is synonymous with taking a company public via the traditional IPO process.

First introduced in the early 1970’s, blank check companies were soon derided by securities regulators after a string of capital raises by companies that had notoriously little corporate governance, enabled unsupervised CEOs to empty corporate coffers for personal gain, leaving investors with nothing. In the early 1990’s, the construct was re-invented by small-cap investment bank GKN Securities’ founders David Nussbaum, Roger Gladstone and Robert Gladstone, who have been credited with introducing the SPAC construct (along with securing a trademark for SPAC), which is chock full of checks and balances. The GKN leadership team’s early success in floating ‘blank check’ companies led to their creating a new firm, EarlyBirdCapital which has become the thought-leader in SPAC offerings, as the SPAC template has since been emulated by the financial industry’s leading investment banks and endorsed by major exchanges across the globe.

In the past 10 years alone, tens of dozens of capital raises via the SPAC construct have delivered billions of dollars of dry powder for designated acquisition companies that have since effected tens of billions of dollars worth of ‘quick IPOs’ for companies in nearly every industry sector, including the cannabis industry,

One fintech industry veteran and startup industry consultant who coincidentally helped GKN introduce their first SPACs to institutional investors back in 1993, and now serves on the advisory board of fintech merchant bank SenaHill Partners said, “Far Point Acquisition may not be the first Fintech SPAC, but its launch clearly reinforces a compelling approach to raising capital for the purpose of bringing established private companies into the publicly-traded ecosystem.”

Via video clip below, former NYSE top gun Tom Farley expresses his views on the SPAC construct and the fintech sector, and provides a glimpse at the prospective target acquisitions that Farley will be aiming for.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com.