MarketMuse update courtesy of Todd Shriber from ETF Trends.

The Global X FTSE Greece 20 ETF (NYSEArca: GREK) is off 3% to start 2015 and with anxiety running high that Greece is still a candidate for departure from the Eurozone, global equity market volatility and investors’ skittishness is on the rise.

With Greek elections slated for Jan. 25, global investors are understandably nervous about what the Eurozone will look like in the future. While Moody’s believes Greece’s Eurozone departure probability is not as high today as it was in 2012, there are still negative implications with such an event for fellow Eurozone nations.

Investors can mitigate Greek volatility with a familiar source: U.S.-focused low volatility ETFs, which outperformed traditional benchmarks in 2014. That group includes thePowerShares S&P 500 Low Volatility Portfolio (NYSEArca: SPLV).

“The relative performance of the S&P 500 Low Volatility Index during the Greek crisis in 2011 and 2012 offers insight into risk mitigation,” according to a recent note by PowerShares.

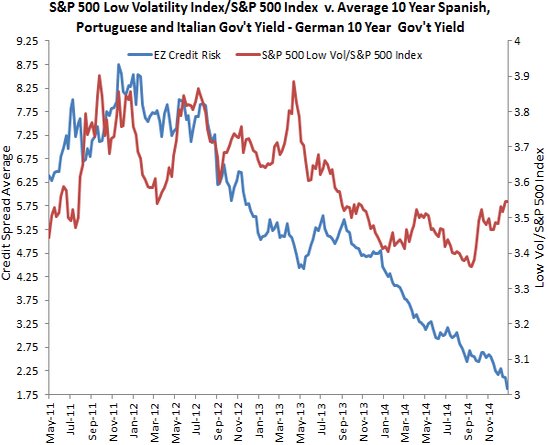

A favored measuring stick for gauging Eurozone volatility is 10-year government bond yields, but combining that with how SPLV’s underlying index performed against the S&P 500 during periods of elevated Eurozone stress proves instructive for investors.

In the chart below, “the red line shows the performance of the S&P 500 Low Volatility Index relative to the S&P 500 Index, based on weekly closing data. When we compare the red line with the blue line, we see that the S&P 500 Low Volatility Index outperformed the S&P 500 Index during each wave of credit stress in the Eurozone,” notes PowerShares.

For original article from ETF Trends, click here.