Most sophisticated investors, whether Tier 1 institutional investment managers, ‘top minds’ across the sell-side, or the truly savvy, self-directed types should all agree that fixed income market signals, and investment grade credit spreads in particular are a prelude to what equities market can expect to happen.

Whether the ‘lag time’ is 3 months, 6 months or 9 months, history has proven that interest rate markets and investment credit spreads are a reliable indicator. Reading those ‘tea leaves’ is complex, and a task often relegated to “senior research analysts.” That said, MarketsMuse followers (primarily investment industry professionals who hail from both sides of the aisle) know that when it comes to truly superior research within the financial market ecosystem, finding diamonds in the rough is not easy, particularly when the landscape is a minefield of jibber jabber produced by ‘experts’ at top banks–folks whose interests are more often aligned with their own wallets as opposed to being aligned with their clients’ best interests.

Worse still, having access to understandable, plain-speak analysis from objective and un-conflicted (aka INDEPENDENT) research is a challenge, albeit the unbundling movement is helping to address that issue. Without further ado, the MarketsMuse Fixed Income team is happy to share an ‘evergreen’ piece from one such highly-trained and completely conflict-free expert. You’ve seen the work from Neil Azous of Rareview Macro LLC here before and the banner of his publication “Sight Beyond Sight” speaks volumes.

Roll the tape….

A segment from our daily global macro newsletter, Sight Beyond Sight, written at the end of July – What Investment Grade Credit is Really Telling Us – made the cover of the back-to-school issue of the IRP Journal, a recently launched magazine that is digitally distributed to institutional investors and features current research from independent research providers (aka IRP’s). As our readership expands deeper into Asia we are pleased to have been selected to be on the cover by this Hong Kong-based publisher.

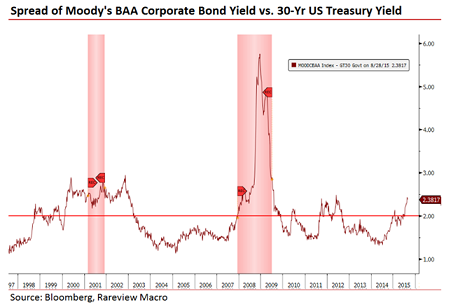

In the past few days, US investment grade (IG) credit spreads have reached new three year wides. Historically, the absolute level of these spreads is consistent with periods of economic and financial market stress. Additionally, the daily volatility of these spreads has increased dramatically in recent weeks.

Below is a chart of the Moody’s Baa Corporate Bond yield spread over the US 30-year Treasury yield.

What is the significance of this observation?

Investment grade corporate bonds are one of the least risky investments within the capital structure, and less sensitive to changes in default risk due to economic weakness. Moreover, the credit market is arguably, next to the slope of the yield curve, the greatest predictor of future economic stress.

The most widely cited explanation for the recent widening in spreads is that it is due to the amount of new investment grade credit issuance. Indeed, that is one factor as new issuance (+SSA) set a record pace yesterday after having surpassed $1 trillion, a level not reached last year until mid-September.

However, the recent widening of the spreads is not just down to the recent surge in corporate issuance. Issuance is simply not a large enough driving force to cause this level of “stress”. The reasons for this widening are two-fold.

Firstly, the aggregate level of issuance, to a degree, is beginning to finally catch up with the market after years of sensational appetite. Corporations, in aggregate, are raising their leverage levels by issuing the new debt and not using the proceeds to grow their revenues or cash flows to compensate. Put another way, the market is beginning to segregate between issuance related to refinancing a company’s “credit stack” as part of its normal annualized funding requirements and pure capital redeployment for the benefit investors.

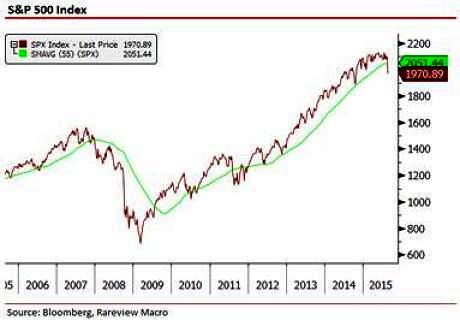

By the way, not only is the IG spread widening, signaling the distinction noted above, but the equity markets are now doing so as well. See the below chart of the ratio of the S&P 500 to the S&P 500 BUYUP index overlaid with the US Treasury 5-30yr yield curve. Stock buy-backs are simply underperforming in 2015 after multiple years of out-performance as the yield curve steepens in anticipation that interest rate hikes will slow the capital redeployment process down. As a reminder, it is much easier to slow a buy-back than reduce a dividend as the former has a time-band and discretion to implement and the latter generally is a board-level decision.

If the second shoe is actually falling as US (and all other) equities markets appear to indicate this morning, MarketsMuse ETF and Global Macro editors were stimulated by having Sight Beyond Sight with this morning’s coffee, courtesy of Rareview Macro’s Neil Azous. Of particular interest, Azous points to Mebane Faber’s The Ivy Portfolio for those who have defaulted to using exchange-traded funds and to the reference to Occam’s Razor, a principle that global macro enthusiasts will appreciate.

Without further ado, please find an extract from this morning’s edition of Sight Beyond Sight…

Corporate Buybacks Not Strong Enough to Save Stocks Today…Retest of the Lows Now Underway

Negative Statistical Analogs

No September First of the Month Inflows

China Quantitative Tightening (QT)

Trends Switch to Medium- from Short-Term

Correlation Breakdown

Neil Azous, Rareview Macro

The key takeaways to start September are invisible to the naked eye; a little sight beyond sight is required this morning in order to see them clearly.

Firstly, we are not sure who the source was, but the following S&P 500 analog was sent to us:

In the 11 times the S&P 500 fell by more than 5% in August it declined in 80% of the subsequent Septembers; the average decline in September in those years was 4%.Now, there are many statistics with similar odds of success being circulated out there, but in aggregate these one-liners miss the bigger picture, in our opinion.

The message is that the higher volatility witnessed during August has carried over into September. It took eight hours of the overnight session for S&P futures (ESU5) to confirm 65% of the above analog, as the index was -2.6% at one point.

Secondly, the first of the month inflows into risk assets that professionals are accustomed to relying on to support their long equity positions has gone missing this year. Inflows into equities are generally expected to follow the simultaneous release of PMI manufacturing data, especially when the data historically points to a stronger global growth profile. However, the data released this morning was uniformly weak, and serves as a reminder of the regional synchronicity – that is, Japan’s consumption-led recovery is faltering, the US has a second half of the year inventory overhang to work through, Europe’s inflation profile is reverting back to pre-“QECB” profile, and China remains an unknown.

Thirdly, given the overall weakness in risk assets the sell-off in the German Bund (RXU5) over the last 24-hours is confounding professionals. Occam’s Razor, a principle that states that among competing hypotheses that predict equally well, the one with the fewest assumptions should be selected, suggests that the Chinese central bank is once again selling dollars and foreign fixed income reserves to buy yuan. As a reminder, FX intervention means foreign reserves have to shrink. The mechanics are as follows: sell foreign sovereign bonds > receive US dollars (USD), euro (EUR), yen (JPY) > use USD/EUR/JPY proceeds to buy CNY = no impact to private economy.

The Chinese Yuan, both the onshore (USD/CNY) and offshore (USD/CNH) versions, is trading at its strongest level since the devaluation. The key difference today however is that the central bank is not defending yuan weakness. Instead, in the spirit of managing volatility, it appears it is proactively reminding speculators who their daddy is and doing a good job of crushing their souls at the same time.

One needs to have ‘been there and seen that’ for at least twenty years in order to have been “loaded for bear” in advance of this morning’s equities market rout. At least one of the folks who MarketsMuse has profiled during the past many months meets that profile; and those who have a true global macro perspective such as Rareview Macro’s Neil Azous have pointed to the credit spread widening during the past number of months as a prime harbinger of things to come. And so they have…

Neil Azous, Rareview Macro

Last night, Neil Azous published one of his finer commentaries in advance of this morning’s global equities market rout and incorporated a great phrase:

“Man looks in the abyss, there’s nothing staring back at him. At that moment, man finds his character. And that is what keeps him out of the abyss.” – Lou Mannheim, Wall Street, 1987

The highlights of last night’s edition of “Sight Beyond Sight” are below…

Big Picture View

S&P 500 View

Asset allocation Requires Swimming Against the Tide – Low-to-Negative Downside Capture

Long German versus Short US Equities (Currency Hedge)

US Fixed Income – Short 2016 Eurodollars

Long European & Japanese Equities (FX hedged), US Biotech and US 10-Yr Treasuries

Long US Energy Sector

Volatility – Sell Apple Inc.; Not the S&P 500 or VIX

Harvesting S&P 500 Index Option Skew

Long Agricultural Call Options

Long US Housing (Hedged)

Technical Mean Reversion – Short EUR/BRL

Long Euro Stoxx 50 Index Dividend Futures (symbol: DEDA Index)

To read the full edition of the Sight Beyond Sight special Sunday (Aug 23 2015) commentary, please click here*

*Subscription is required; a free, 10-day trial is available

Neil Azous is the founder and managing member of Rareview Macro, an advisory firm to some of the world’s most influential investors and the publisher of the daily newsletter Sight Beyond Sight.

Within the context of continuous guessing as to the outlook for a rate hike, and how to hedge fixed income portfolios accordingly, getting a strong fix on fixed income strategies has proven to be a challenge for a vast majority of professional investors during the past 24-26 months, many of whom have replaced high-priced wall hangings with dart boards. Many other managers prefer to simply hum “Lower for Longer” to themselves. For global macro-focused fund managers, MarketsMuse spotlights a refreshing update from Rareview Macro LLC, the global macro think tank and publisher of professional newsletter “Sight Beyond Sight.” Below please find opening excerpt from today’s edition

Neil Azous, Rareview Macro

We are pleased to present our new portfolio construction, including four new trade ideas and a tail risk hedge that make up our core fixed income strategy. As is customary, each one includes our standard trade matrix with a pre-defined game plan for managing gains and losses.

For those that regularly traffic in fixed income, we look forward to any feedback you may have and a spirited debate on our ideas. We are confident they are sufficiently robust to survive some criticism. For those not in fixed income, please feel free to share this internally with your colleagues who are.

TRADE 1 – Gradual/Variable pace of rate hikes

TRADE 2 – Leverage on Gradual/Variable pace of rate hikes

TRADE 3 – Targeted field bet on no rate hikes in 2015, recession book overlay

TRADE 4 – “Uncertainty” Risk Premium

TRADE 5 – Choke Yourself Tail Hedge

Highlights:

Thematic view, not tied to day-to-day movements in the long bond

Multiple sources of return attribution

High return on capital: Low option premium outlay, high leverage

High risk/reward: Lose 1.5% (realistic) to 3% (absolute) of the NAV to make 6% to 8%

Both quantitative and qualitative risks clearly expressed

Above is the teaser, those interested in drilling down into the above, today’s edition of Sight Beyond Sight is available by clicking this link.

MarketsMuse Global Macro and Fixed Income desks converge to share extract from 23 July edition of Rareview Macro commentary via its newsletter “Sight Beyond Sight”. For those not following the corporate bond market, most experts will tell you the equities markets follow the bond market–which in turn is a historical indicator when it comes to economic expansion, contraction, and recession. Below is courtesy of Rareview’s founder/managing member Neil Azous .

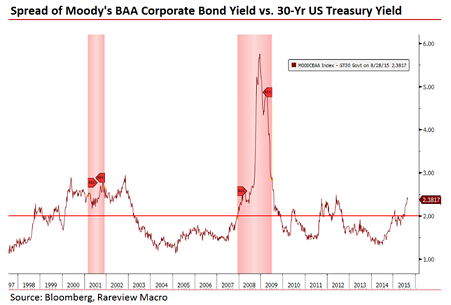

In the past few days, US investment grade (IG) credit spreads have reached new three year wides. Historically, the absolute level of these spreads is consistent with periods of economic and financial market stress. Additionally, the daily volatility of these spreads has increased dramatically in recent weeks.

Below is a chart of the Moody’s Baa Corporate Bond yield spread over the US 30-year Treasury yield.

What is the significance of this observation?

Investment grade corporate bonds are one of the least risky investments within the capital structure, and less sensitive to changes in default risk due to economic weakness. Moreover, the credit market is arguably, next to the slope of the yield curve, the greatest predictor of future economic stress.

The most widely cited explanation for the recent widening in spreads is that it is due to the amount of new investment grade credit issuance. Indeed, that is one factor as new issuance (+SSA) set a record pace yesterday after having surpassed $1 trillion, a level not reached last year until mid-September.

However, the recent widening of the spreads is not just down to the recent surge in corporate issuance. Issuance is simply not a large enough driving force to cause this level of “stress”. The reasons for this widening are two-fold.

Firstly, the aggregate level of issuance, to a degree, is beginning to finally catch up with the market after years of sensational appetite. Corporations, in aggregate, are raising their leverage levels by issuing the new debt and not using the proceeds to grow their revenues or cash flows to compensate. Put another way, the market is beginning to segregate between issuance related to refinancing a company’s “credit stack” as part of its normal annualized funding requirements and pure capital redeployment for the benefit investors.

By the way, as we have pointed out in these pages for a while now, not only is the IG spread widening, signaling the distinction noted above, but the equity markets are now doing so as well. Again, see the below chart of the ratio of the S&P 500 to the S&P 500 BUYUP index overlaid with the US Treasury 5-30yr yield curve. Stock buy-backs are simply underperforming in 2015 after multiple years of outperformance as the yield curve steepens in anticipation that interest rate hikes will slow the capital redeployment process down. As a reminder, it is much easier to slow a buy-back than reduce a dividend as the former has a time-band and discretion to implement and the latter generally is a board-level decision.

Secondly, we are aware that discussions around the lack of liquidity in the credit markets are a near daily occurrence these days. The only observation of note is that there is now a new term associated with the market construct – that is, “liquidity cost basis”. In simple terms, due to the lack of market depth and the continued sensational appetite to issue bonds, there is now a higher premium being applied in the market to finding liquidity if you want to own a bond. All we are saying is that the investor concerns over liquidity are not only being priced into the market but those worries have been crystalized with a fancy Wall Street name.

The end result is that investors are demanding a higher premium for the new issues they are taking down, largely due to deteriorating fundamentals in the actual credit.

Now, the second most widely cited explanation for the spread widening is that it is due to the energy sector. If you decompose the spreads it is easier to argue that a notable portion of the weakness is due to the deterioration in the energy sector, whose credit spreads are highly correlated with the lower price of crude oil. However, energy makes up a much smaller portion of the investment grade market (~12%) than it does for the high yield (i.e. ~18%+), which indicates that the breadth of weakness stretches across many other sectors of the investment grade market and is not due to one single risk factor, such as crude oil.

Lastly, we would note that the absolute levels of these spreads referenced on the chart above are also consistent with weakness after the US quantitative easing program was completed and in anticipation of an interest rate hike. We are not sure how much of the spread widening is a result of this less easy monetary policy but the fact is that both QE and the zero interest rate policy forced investors to perpetually search for yield and investment grade credit was a major source of that appetite. To what degree that happened is difficult to handicap but some of those inflows have to reverse given how asymmetric the outcome would be if the Federal Reserve actually embarked on a rate hiking cycle consistent with past cycles, as opposed to a gradual pace of hikes.

Taking a step back, if you look at both the US yield curve and the credit markets, what you find is that both are saying roughly the same thing – that is, there is currently a recession risk embedded in the market, and that there is the potential for the end of this credit and/or economic cycle to be on the horizon.

Take what we have just sketched out any way you want. We are not making a bearish call on risk assets or attempting to sell blood. All we are doing is saying that credit markets, the yield curve and corporate share repurchase trends are signaling some concern sometime over the next 6-9 months. Given that we have not had a recession in 6-7 years, and historically we have had one every four years on average in the modern era, it is not at all unreasonable to start to watch these signals a lot more closely from now on for something more acute.

Above segment from investment newsletter Sight Beyond Sight is re-published with permission from global macro think tank Rareview Macro LLC. Subscription to the daily commentary and trade strategy profiles is available via the firm’s website

Disruptive Unbundlers, Securities Industry Untouchables, Fintech Aficionados and Innovative Altruists seek to level the investment research playing field, inspiring a bull market for independent research distribution channels, start-ups and disruptive schemes.

Investment research and expert ideas, whether within the context of equities analysis or global macro perspective, has long been the domain of sell-side investment banks, whose research insight is typically bundled as a ‘free product’ within the range of fee-based services provided, including trade execution. Those old enough to remember the ‘dot-com bubble’ days will recall that much of Wall Street’s so-called research was (and arguably still is) notorious for being heavily tilted towards “buy recommendations” in favor of the investment bank’s corporate issuer clients.

This clearly conflicted practice was perfected in the late ‘90s by the likes of poster-boy analyst Henry Blodget (since banned from the securities industry, and ironically, now Editor and CEO of financial media company Business Insider) and was lambasted by securities industry regulators when the “Internet bubble” burst. Those chasing-the-horse-after-the-barn-door-closed efforts since led to a regime of regulation and firewalls intended to distance in-house research analysts from their investment banker brethren so as to mitigate biased recommendations and conflicts of interest. Compliance officers across the industry found themselves facing a host of new rules, and that ‘compliance contagion’ served as the catalyst for a spurt in “independent research boutiques” offering “unbundled” and un-conflicted research sold as a stand-alone product with no ties to execution or trading commissions.

However compelling the notion, and despite the regulatory impetus to foster the growth of independent research boutiques, the business model for these firms has proven challenging during the past 10-15 years. Many boutique research firms floundered or failed for several crucial reasons, including but not limited to (i) the burdensome costs and means associated with creating a stand-alone brand, (ii) the challenge of delivering consistent and compelling content to institutional investment managers and sophisticated investors at a price point that could prove profitable and (iii) the non-trivial logistics required to deliver content in a compliant manner. In the interim, regulators stood by and observed, and digital delivery mechanisms for independent researchers only slowly evolved. Investment banks, never shy when it comes to creative workarounds, bolstered their research ranks and produced more content, even if mostly undifferentiated, but still promoted by the strength of the investment bank’s brand.

All of this is about to change again, causing some to conclude that regulatory market moves in cycles every decade or so, much like the stock market moves in cycles. The current bull market case for unbundled independent research is not a result of efforts by get-tough-on-Wall Street types such as New York Attorney General Eric Schneiderman or Massachusetts’ kindred spirits Elizabeth Warren and William Galvin, and the bull case is certainly not because of any efforts made by the SEC. To a certain extent, the positive outlook for those in the unbundling space is based on Moore’s Law and the advancement of Fintech-friendly applications, but it is more directly attributed to a new European Union law inspired by MiFID II, that if passed as expected, will require investment managers to pay specifically for any analyst research or related services they receive. With that new rule (which includes more than a few line items), many large money managers are starting to follow the proposed rules globally; investment banks in the U.S. (and obviously those in Europe) are devising new business models for one of their oldest and highest-profile functions: offering ideas to customers that banks can monetize through commission-based services.

More than some across the major continents believe that however much top investment bank brands are a decidedly powerful selling tool for research product, the power of the internet has enabled the distribution of independent research and enables a Chinese menu of pricing schemes via a continuously-growing universe of independent portals that invite content publishers to sell their products using an assortment of social media-powered distribution channels and revenue-sharing schemes.

Bloomberg LP has created its own independent research module accessible by 300,000+ subscribers in direct competition with Markit, the financial information services provider. Earlier this year, Interactive Brokers (NASDAQ:IBKR), the web-powered global online brokerage platform that provides direct market access to multiple exchanges and trading venues across the entire asset class spectrum quietly began enhancing its offering of third-party professional and institutional-grade research. IB’s 300,000+ accounts comprising professional traders and institutional clients may subscribe to research made available in the trading platform, Trader Workstation (TWS). At the same time, IB began promoting these third-party research providers via IB Traders’ Insight, a blog embedded within the firm’s Education module that covers the full range of investment styles from more than two dozen content providers.

While bolstering objective research content is a natural business extension for those having captive brokerage clients and for terminal-farm behemoths, perhaps even more interesting is that start-ups in the unbundling space are starting to percolate.

On the European side of the pond, UK-based SubstantiveResearch, created earlier this year by former EuroMoney Magazine publisher Mike Carrodus, is positioned to be an institutional research thought- leader that curates and filters both independent and sell side global macro research, with a sleeve that hosts regulatory events for investment manager content consumers and sell-side content providers. Start-ups in the US include among others, Airex Inc. , which dubs itself “the Amazon.com for financial digital content” and recently secured funding from fintech-focused merchant bank SenaHill Partners. TalkMarkets.com is another notable entrant to the space, and was created in late 2014 by Boaz Berkowitz, a former “Bloombergite” who was also the original brain behind Seeking Alpha. From the traditional financial media publishing world, industry stalwart Futures Magazine, recently re-branded as “Modern Trader” and the parent to hedge fund news outlet FinAlternatives is also embracing the research content unbundling movement as a means towards capturing more Alpha and better monetizing relationships with content providers. Each have their own business models, including the use of cloud-based technology and coupled with the muscle of creative online marketing, social media tactics and search-engine ranking techniques.

While the start-up space is often littered with short shelf-life stories, these new unbundled research distribution vehicles are being enabled by the fintech revolution and embraced by distributors of content, high-profile independent research providers, as well as by at least one major bank seeking to hedge its internal bets; earlier this year, Deutsche Bank inked a deal with upstart Airex, such that DB’s proprietary equity research is available on a delayed basis and can be purchased by any AIREX Market shopper. In the case of now 6-month old TalkMarkets, they are embracing an advertising-based business model, which is predicated on building an outsized audience of sophisticated retail investors for prospective advertisers. To date, they have enlisted more than 350 content providers and 10,000+ registered users. While there is no cost to access the platform, content providers are able to upsell subscription-based services and at the same time, earn ‘points’ that can be converted into the private company’s equity shares.

Neil Azous, Rareview Macro

According to former sell-side global macro strategist Neil Azous, the Founder/Managing Member of think tank Rareview Macro LLC, and the publisher of subscription-based “Sight Beyond Sight” which is now being distributed across several channels apart from the firm’s website (including via Interactive Brokers), “Truly superior, high-quality content, including actionable ideas remains relatively scarce, but the fact remains, content has become commoditized. The good news is that banks are not the sole source of carefully-conceived research and the better news is that conflict-free content publishers can now more easily distribute via a broad universe of narrow-casting, web-based channels.”

Added Azous, “For independent research providers and trade idea generators, it’s arguably a watershed moment. As new rules take shape, content publishers, including those who previously worked under investment bank banners, can now reach an exponentially larger universe of content buyers through these new distribution channels. It’s a numbers game; instead of working inside an investment bank and trying to ‘sell’ a traditionally high-priced product to a relatively narrow list of captive clients, the more progressive idea generators can re-tool their pricing and make their product available to exponentially more buyers, and in a way that conforms to and stays within goal posts of compliance-sensitive folks.”

However much it makes sense to foster the easy distribution of independent and un-conflicted research, Wall Street et. al. is not going to easily abrogate their role for providing ideas or forgo the trade execution commissions derived from those proprietary ideas. Banks are reported to be devising new pricing models for investment research in view of EU proposals that could prevent research from being paid for using dealing commissions. In an unbundled world, where payments are separated, competition for equity and credit research may increase as asset managers look beyond traditional sources, which may trigger fragmentation. They may also move research in-house. The U.K.’s FCA, which is driving the debate, has endorsed the EU proposals.

As noted within the most recent edition of Pensions & Investments Magazine, Barclays PLC, Citigroup Inc., Credit Suisse Group AG and Deutsche Bank AG are working with clients to come up with pricing for the analyst research customers receive, according to bank executives. Prices are expected to range from roughly $50,000 a year to receive standard research notes, up to millions of dollars for bespoke research and open-door access to analysts.

“We are working to change the mind-set so that fund managers understand that research should be treated as a scarce resource. There is a great opportunity to tap into experts in their fields at brokers, but we need to really think about the value of research and determine the right amount to pay for it,” said Nick Anderson, head of equities research at Henderson Global Investors.

The following [excerpted] analysis is by Bloomberg Intelligence analysts Sarah Jane Mahmud and Alison Williams and helps summarize the current outlook. It originally appeared on the Bloomberg Professional service. Continue reading →

Now that InteractiveBrokers is turning up the heat and joining the “unbundling movement” by offering independent research via its world-class trading platform, MarketsMuse editors spotlighted the following comments courtesy of global macro sage Neil Azous, Founder/Managing Member of Rareview Macro LLC from today’s IB feed..If you’re a hedge fund-type, you will either smile, smirk or throw a rock at your computer..

Neil Azous, Rareview Macro

A few of our hedge fund buddies have asked us to bring back “the old-school Neil” and tell you what I think will happen in the next 48-hours. We aim to please, at least sometimes, so therefore today’s note has a lot of “hedge fund speak” and is very short-term in nature. Here we go.

If you ban selling, threaten to arrest short sellers and suspend over half the market, then at some point Chinese equities will inevitably close positive. Add in some good old fashioned government buying of what actually remains open and it is no great surprise that equity markets closed positive in China.

Of the 2,754 shares traded in Shanghai, 1,700 were suspended but the ones that were opened had virtually a 100% up-day. All 194 of the 484 shares that are still open for trade on the ChiNext Board – the poster child for speculation – rose limit up 10%. The three main index futures – CSI 300 and CES China 120 – closed limit up 10% and FTSE China A50 futures closed up +17%. The 5.8% gain in the Shanghai Composite was the largest since 2009.

While the invisible hand of China’s government has set a positive bid-tone for the rest of global risk assets today, it also increased the probability of further PnL duress for long/short hedge funds here in the old US of A.

Sadly, the desire by the long/short hedge fund strategy to reduce overall gross exposure over the last week has been very low.

The fact is that the majority believe that the earnings bar going into this reporting season is so low that you can crawl over it on your knees, and that the dispersion of opportunities remains high due to M&A activity or event-driven catalysts. The last thing this investor base wants to do is lose core positions on account of Greece or China. In Greece, the opportunity cost has been high over the years, and in China’s case, since none of them have really any meaningful direct exposure, the mindset is that the spillover effect to US equities is marginal at best.

As a result, long/short hedge funds remain long on single stocks, and to at least show some appearance to their investors that they are being prudent given the top-down concerns globally they have OVER-purchased a lot of market-related protection, or have used blunt instruments to get really short of the market outright. Put another way, their gross exposure is roughly the same as where it was last month, before the very recent global margin call kicked in, but there is large contingency now running TOO NET SHORT.

To continue to dazzle you with words like “code-red”, it does not take a genius in this business to look at all the usual short-term hedge fund indicators and recognize that many of them are at extremes – that is, put/call option ratios are at 18-month highs, prime brokerage position reports show the net short position at multiple standard deviations above the average over the past year, etc.

So what does the fact that long/short hedge funds are extremely long single stocks and over-hedged actually mean? Continue reading →

MarketsMuse Global Macro update is courtesy of extract from a.m. edition of “Sight Beyond Sight”, the newsletter published by global macro think tank Rareview Macro LLC and authored by Neil Azous.

Neil Azous, Rareview Macro

In last Thursday’s edition of Sight Beyond Sight we argued that we couldn’t work out how anyone was able to make an argument about the short-term direction of fixed income, and especially calling the end of the sell-off, with a straight face. Put another way, there were a lot of pikers out there with no accountability or transparency voicing their opinions that day. Given that any attempt at analyzing fundamentals relative to positioning at historically climactic moments is generally a very poor exercise, we refused to go on the record that day and said we would regroup over the weekend. Given the resumption of the sell-off, that patience has served us well.

At this point, just repeating that CTA/Managed futures, a strategy that makes up ~10% of hedge fund AUM but deploys the most leverage, have lost on average ~5% over the last few weeks is a waste of time. Since CTA’s apply priced-based trend-following algorithms to the trading of futures contracts what matters is that many thresholds used to trigger a stop-loss have been breached and then some.

The takeaway at this point is that CTA’s/Managed futures strategies are way passed working through large offsides positions and many of them have now flipped their strategies to go the other way. Along those lines the positions that have flipped are more acute so far in Europe than the US.

That is very important to recognize because that position building is still in the early stages and as/if the new trends extend those positions will grow and grow given this is the most levered strategy within hedge fund products.

The big out-trade at this point is that asset managers still hold structural long US dollar and Treasury curve flattening positions and have yet to adjust them in the same way as the CTA’s. Why? Because their threshold for pain is a lot greater and they are not reactive to priced-based trend-following algorithms.

What does this mean? It means that the risk from here is that as CTA/Managed futures strategies ramp up new positions that will begin to force the hand of asset managers who have yet to be really reactive.

The new leverage being applied to the counter-trend on the hedge fund side plus the liquidation of structural position on the asset manager side is the point we think we are at now in terms of overall market positioning.

MarketsMuse Global Macro update profiles perceived opportunities from the perch of Denmark’s Saxo Group Mads KoefoedIt and his view that interest rate increases probably won’t happen during the second quarter, but the market will very likely be dominated by speculation on the likely timing of a US Fed interest rate hike. Focus on the Fed, FOMC, ECB and Euro recovery—and European high-yield corporate bonds.

MarketsMuse.com profile of ETFs intended to provide global-macro-focused investors with a hedge against a continuing strong dollar and currency swings is courtesy of below extract from Mar 20 WSJ column by reporter Carolyn Cui.

Exchange-traded funds that protect against currency swings are attracting U.S. investors concerned that the strong dollar will erode their gains.

Currency-hedged ETFs have more than doubled their assets this year to $50.3 billion, largely thanks to strong inflows of $21.6 billion, according to data tracker ETF.com. Firms that offer the funds—including WisdomTree Investments and Deutsche Bank—use derivatives to offset the effects of currency swings, which they say could cause unintended volatility for investors and even hurt their returns in periods of dollar strength. Continue reading →

MarketsMuse.com update profiling iShares MSCI Sweden ETF ($EWD) and a global macro view is courtesy of extract from March 18th coverage by ETFtrends.com’s Todd Shriber

Shares of the iShares MSCI Sweden ETF (NYSEArca: EWD) were modestly higher Wednesday after the Riksbank, the world’s oldest central bank, surprisingly took Sweden’s repo rate deeper into negative territory with a cut of 15 basis points to -0.25% from -0.1%

Some of Sweden’s larger companies are struggling due to weak demand from Europe, the country’s largest export market, as the krona currency appreciated against the euro. However, lower central bank rates has helped stimulate household spending.

The Swedish central bank recently cut its benchmark rate below zero for the first time and started buying bonds to combat deflationary pressures. However, if the krona continues to strengthen, the Riksbank could be forced to implement more aggressive measures. [Loose Monetary Policy Could Lift Sweden ETF]

In its efforts to stimulate inflation, Riksbank may not be done employing accommodative monetary policy.

“For us, we will pay close attention to the door they opened to launching a scheme to channel monetary support directly to corporations via lending. While no details were provided for the second meeting, we have for some time believed that a funding-for-lending program (FLS), a measure already used by the Bank of England, or a public-private investment program (PPIP), a liquidity tool used by the US Federal Reserve, are transmission mechanisms that have much greater and immediate impacts on the real economy than quantitative easing,” said Rareview Macro founder Neil Azous in a note out Wednesday. Continue reading →

MarketsMuse update courtesy of reporting by Reuters’ Gertrude Chavez-Dreyfuss and Ashley Lau

NEWYORK (Reuters) – U.S. investors spooked by wild swings in the foreign exchange market are piling into exchange-traded funds that strip out the local currency on their international equity portfolios, making them one of the most sought-after financial products in 2015.

With the dollar having rallied more than 19 percent since the beginning of 2014, investors are seeing gains in overseas stock markets eaten up by losses against the greenback.

“People are voting with their feet,” said Luciano Siracusano, chief investment strategist for WisdomTree Investments in New York. “They’re putting billions of dollars into these funds, and what they’re saying is, ‘We don’t want to be 100 percent unhedged.’”

Some say there aren’t enough of these products for investors looking for international exposure. These ETFs have about $31.5 billion in assets, up nearly five-fold from 2011. But assets in international equity ETFs exceed $275 billion, according to WisdomTree.

“There are 40 countries with stock markets deep enough to have a currency-hedged product,” said David Kotok, chairman and chief investment officer of Cumberland Advisors in Sarasota, Florida, which oversees $2 billion, and whose firm’s equity investments are solely through ETFs. Continue reading →